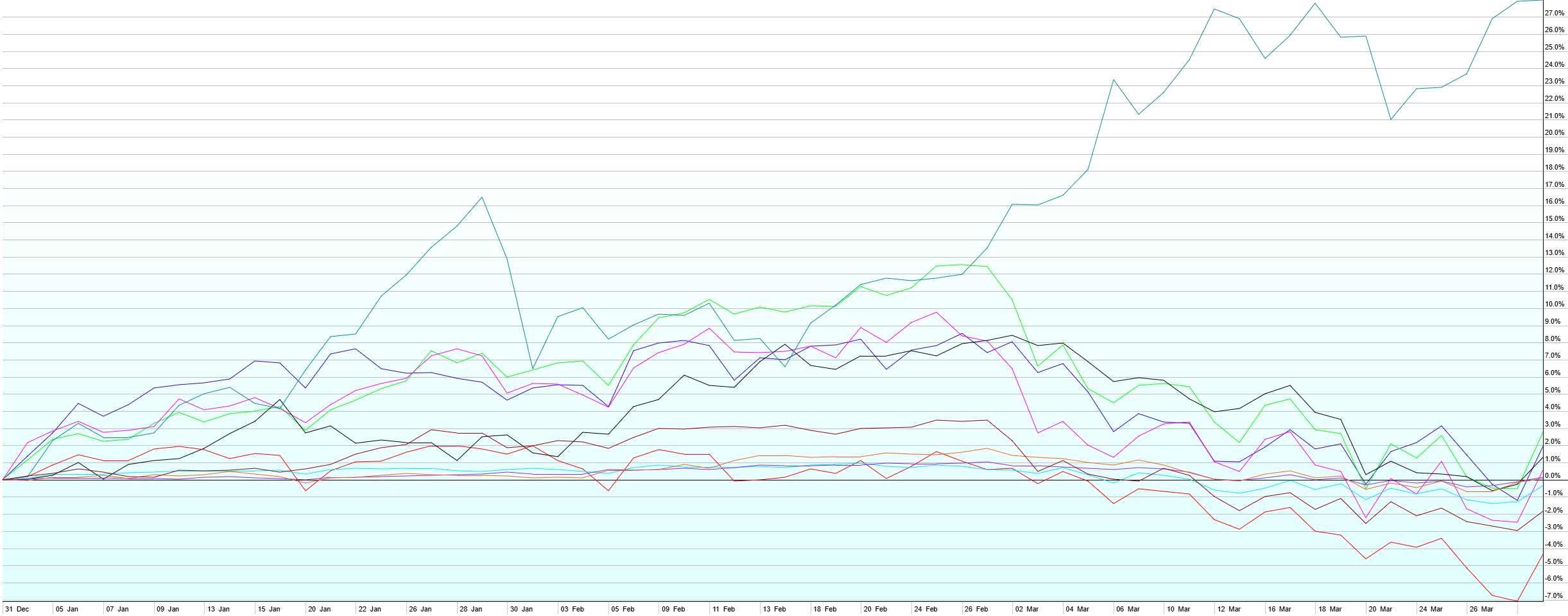

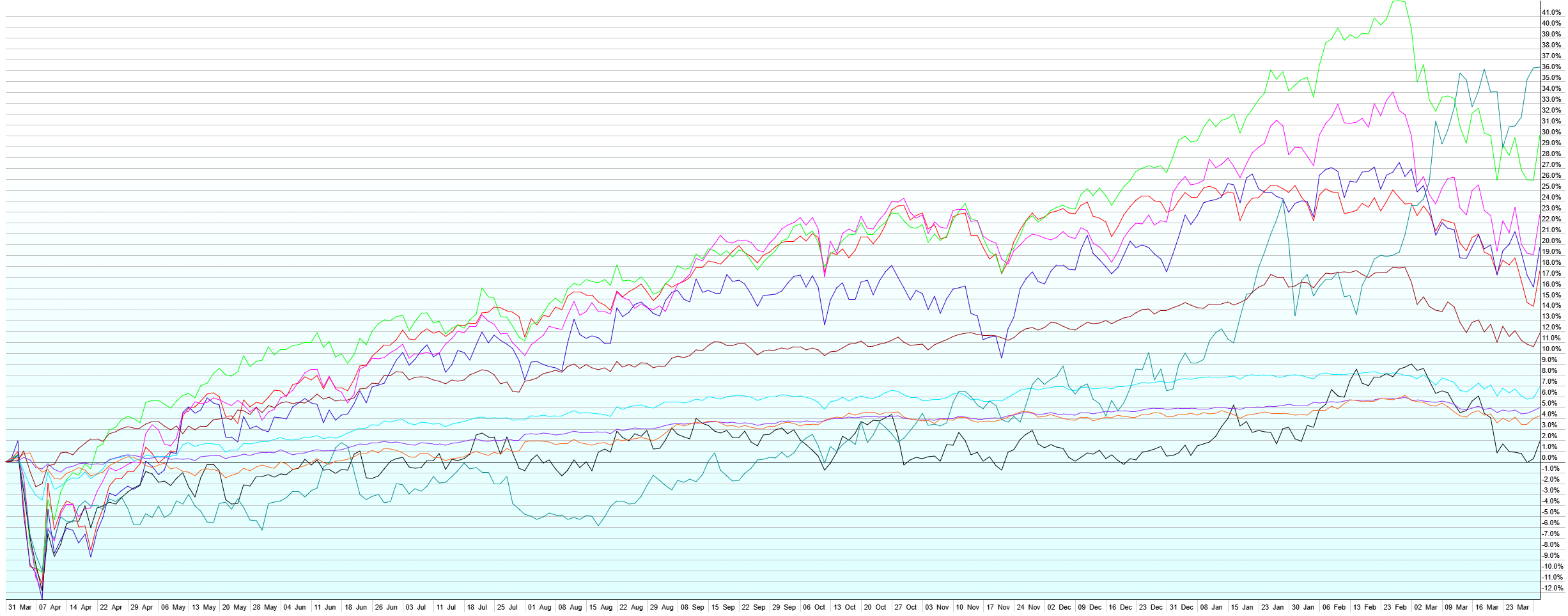

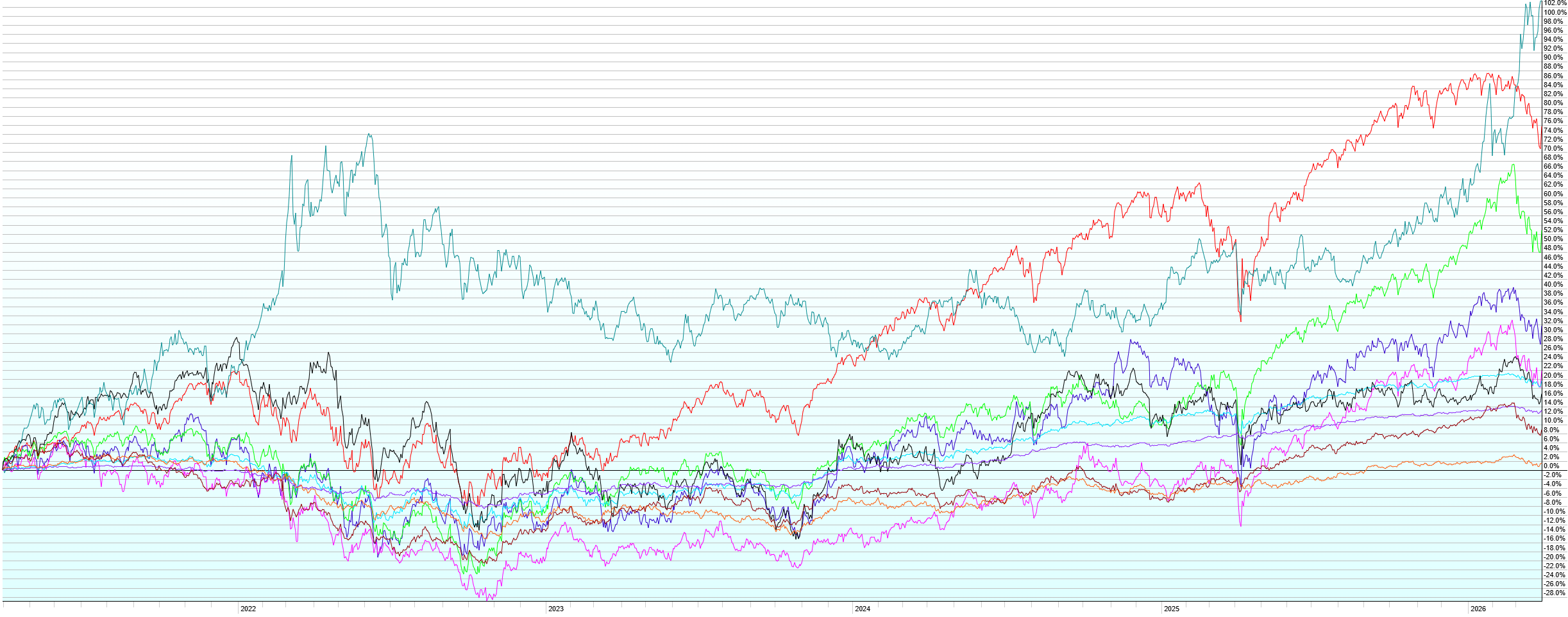

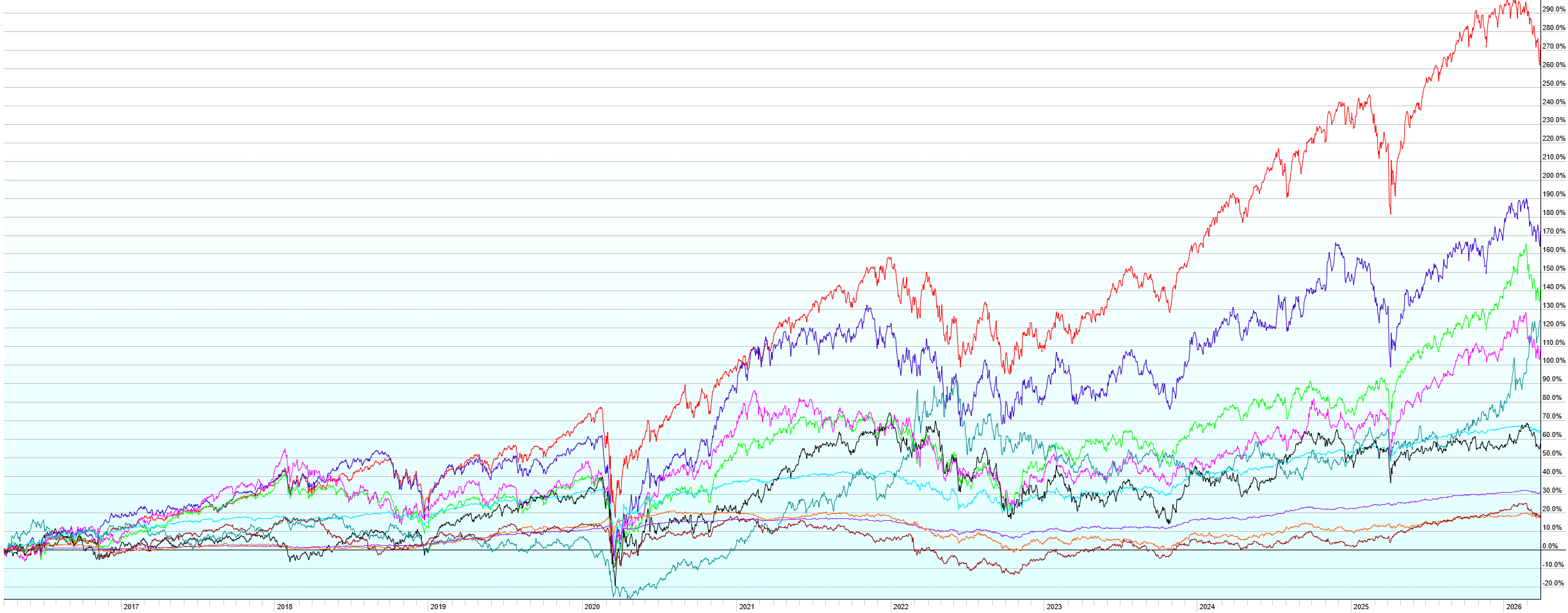

This post contains the usual returns by asset class for this past quarter (by representative ETF), last 12 months, last five years, and last ten years. While there is still no predictive power in this data, I’ll continue to post this quarterly for those of you that are interested.

Last Quarter (1/1/2026 – 3/31/2026)Last 12 Months (4/1/2025 – 3/31/2026)Last 5 Years (4/1/2021 – 3/31/2026)Last 10 Years (4/1/2016 – 3/312026)

A few notes:

Higher energy prices resulting from the “military action” in Iran ground the stock rally to a halt in Q1. While there hasn’t been too much damage overall, at least not yet, stocks around the world are off their highs on the order 5-15%. Diversification paid off once again in Q1 with Commodities leading the way, up 28%. International Developed Stocks finished Q1 up 2.8%, mostly due to their stellar performance in Jan and Feb (they were up 12% at one point). US Small Caps (+1.9%) fared significantly better than Large Caps (-4.4%), which were the worst performer of the quarter. In the middle of the pack were US REITs (+1.4%), Emerging Market Stocks (+0.5%), US Aggregate Bonds (+0.1%), US Short-Term Corporate Bonds (+0.1%), US High-Yield Bonds (-0.4%), and Emerging Market Bonds (-1.9%). The market pulled back the odds more Fed cuts in 2026 substantially, going from 1-3 more cuts expected this year at the start of Q1 to 0-1 more cuts at the end of Q1. This is the result of higher energy prices, which could put pressure on broader inflation and cause the Fed to be more restrictive with policy. Much of the damage already done in the Middle East will have a lasting effect on energy prices, even if tensions ease immediately. It remains to be seen whether those higher energy prices restrict the global economy enough to decrease demand (recession) or if the economy continues to chug along with higher prices and even higher expectations of higher prices passing through to goods and services (inflation). The Fed, along with it’s incoming new chairman, is in a tough spot trying to price rates for a very uncertain future.

Note also the other charts as we’re now approaching the one-year anniversary of the “Liberation Day” selloff around the world. Despite tariffs, war in the Middle East, war in Ukraine, spiking energy prices, Trump, Biden, a global pandemic, US debt downgrades, natural disasters, and a host of other imperfect world issues most of us can’t even remember over the last decade, all major market segments are up over the last one, five, and ten years. There’s a lesson in there somewhere.

Reverting back to Q&A conversation format for this one…

Q: Uh oh… market update time. I guess that means the stock market is in trouble?

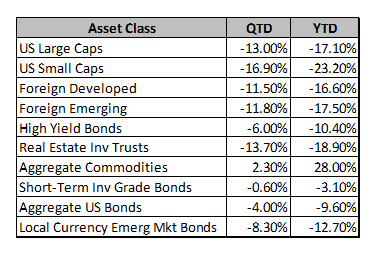

A: I wouldn’t say it’s in trouble because that gives the sense that something bad is about to happen. We don’t know what’s going to happen in the future. It sounds like semantics, but it’s an important distinction. What we do know is that stocks have performed terribly to start 2022, especially over the last 6 weeks. The Russell 2000 (small caps) and the Nasdaq are down ~30% from their highs and the S&P 500 is down 18.5%. Here’s a quick look at how the major asset classes that we track have performed quarter-to-date and year-to-date (by representative ETF):

High-growth tech has really taken it on the chin with more than 50% of the Nasdaq down more than 50% from its all-time high now. Stocks in ARK’s Innovation ETF (ARKK), perhaps the “growthiest” of growth stocks, are off even more, with the fund itself down 70%. Some other high-profile names that were booming a year or two ago make even that look not that bad (Shopify -81%, Zillow -82%, Zoom -85%, Coinbase -85%, Robinhood -88%, Peloton -93%). The market has woken up and remembered once again that price matters, and you can’t just put all your money in well-known, high-growth names at any price.

Q: That sounds awful. I know that individual stocks carry much bigger risks than the indexes, and that you don’t generally recommend individual stocks, and that PWA clients don’t own any of those names (or ARKK), so I’m not too worried about those. But, how does the decline in the S&P 500 compare to other historical declines?

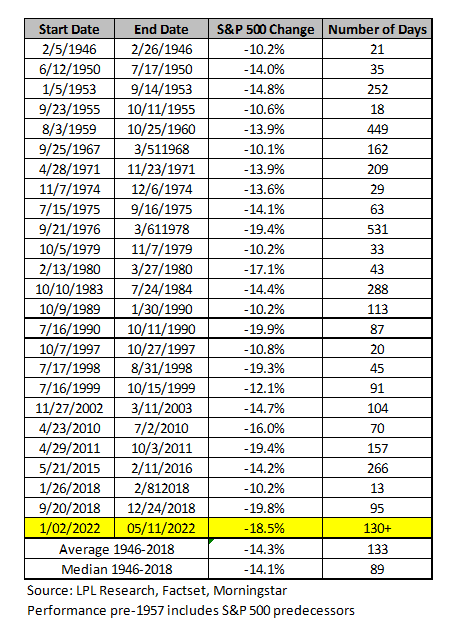

A: It’s just slightly worse than the average case. Looking at the all the times since WWII that the S&P has dropped by more than 10% from its previous high, on average, it has fallen 14.3% and it has taken 133 days from top to bottom. We’re currently down 18.5% and its been 130 days since the high. So really, this is pretty routine behavior for the S&P.

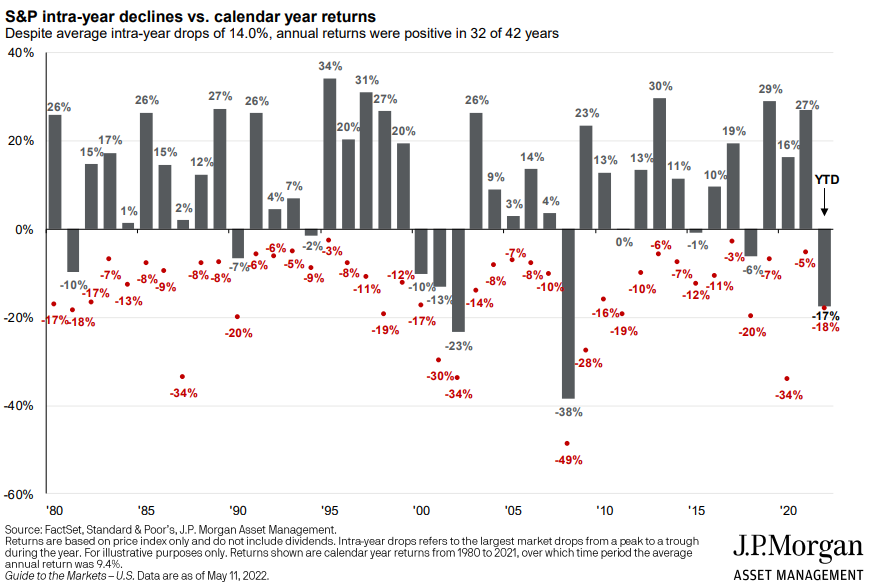

Another way of looking at this, courtesy of JP Morgan, is shown below:

You can see there are quite a few years where stocks are down significantly at some point during the year, but actually finish the year much better off. In fact, in the 23 years since 1980 that the market has been down more than 10% during the year, it finished up in 14 of them.

Q: You’ve often reminded me that there’s a nearly 100% chance that stocks are going to fall 50% from their highs, in aggregate, during my lifetime. Is this going to be one of those times?

A: While I’m very certain it’s going to happen eventually, there’s no way to know when it’s going to happen. That’s why we don’t try to time the market, moving money in an out of stocks pretending we have a crystal ball. Instead, we plan for it in client financial plans and incorporate it as a likely outcome in risk tolerance discussions. That lets us construct portfolios that can achieve client goals regardless of when (not if) the stock market temporarily declines.

Q: From the index returns table, it looks like even bonds are having a tough time. Aren’t they supposed to be the conservative, more stable part of a portfolio?

A: Bond returns can be negative from time to time. But they’re much less negative than their stock counterparts. Additionally, our client portfolios lean toward short-term bonds and incorporate inflation-protected bonds, both of which are down less than long-term or even aggregate bond funds. The long-term US treasury bond fund is down 20% so far this year. Short-term bonds are down 3.5-5.5% and short-term TIPS (treasury inflation protected securities) are actually up 0.3%. When interest rates rise, existing bond prices fall because they’re paying older/lower fixed interest rates, and are less appealing to investors. The shorter the term of the bond (or bonds in a bond fund), the less they’ll fall when interest rates rise because the bonds mature fairly quickly, investors get their principal back, and they can reinvest in new, higher interest rate bonds. With rates as low as they have been, we’ve tilted client portfolios toward short-term bonds, feeling like there’s an asymmetric chance of rising rates over falling rates. Short-term bonds are now paying nearly 3%, vs. the ~1% they were paying a year ago. The good news in rising rates is that while they temporarily depress bond prices, the interest they pay increases (quickly if the bonds are short-term), and eventually you are made whole and then some. Incorporating TIPS into portfolios also helps in times like these because TIPS pay a fixed interest rate + an inflation adjustment. When rates rise due to higher inflation, the higher inflation adjustment increases the interest payment and helps to offset the impact of the higher rate on fixed interest bonds prices. So, while this has been an ugly period for bonds, it’s within the bounds of what we expect for this type of environment and is going to lead to higher interest payments over the next couple of years a result.

Q: Understood. So what’s causing all this financial market stress?

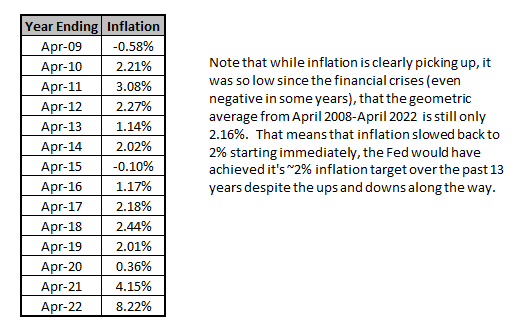

A: It’s hard to know with certainty, but I’d say a combination of fear of rising inflation and fear of slowing economic growth around the world. Inflation had been running stubbornly below the Fed’s 2% target for quite some time and has recently accelerated substantially (see table below). As world demand for goods and services came back online after covid, supply was unable to keep up. Supply chain issues led to goods shortages and rapid growth in open job positions led to employee shortages. This combined with seemingly endless money printing to support the post-financial crisis / post-covid economy and large fiscal stimulus resulted in too much money in the system chasing shortages of goods and services. People had savings and didn’t want to go back to work in a restaurant. Everyone wanted to travel at the same time. There was suddenly worldwide demand for energy at a pace that made negative oil prices of two years ago seem like a lifetime ago. It started with energy, then travel / tourism, then hospitality / dining, and now is impacting just about everything. The war in Ukraine caused another jump in energy and food prices and put more pressure on inflation. China’s latest bout with covid has also further increased supply shortages on various goods imported around the world.

As a result, the Federal Reserve and other central banks are pulling back on the liquidity they’re providing via Quantitative Easing (money printing to buy government debt and finance spending more than we’re collecting in tax revenue) and starting to raise interest rates. This month, the Fed raised interest rates by 50 basis points, taking overnight rates up to 0.75-1.00%, following a 25 basis point hike in March. They’ve signaled much more on the way.

Q: How much more?

A: Fed Funds Futures markets tell us (see derived probabilities below) that the market is currently forecasting nearly 3% rates by the of 2022 with potential of higher than that into 2023.

Q: Wow. That’s a pretty big change from what the economy is used to right?

A: Exactly. And it’s happening very fast. In anticipation of the higher overnight rates, longer-term rates have been climbing. Mortgage rates which were in the mid-3% range last year are suddenly over 5.5%. This puts pressure on housing and other activities that depend on financing. Q1 GDP came in negative (i.e. the US economy shrank in the first three months of 2022) and so the Fed is planning on substantial more tightening into a rapidly slowing economy.

Q: This is starting to sound really bad. Where’s the good news? There’s always good news isn’t there?

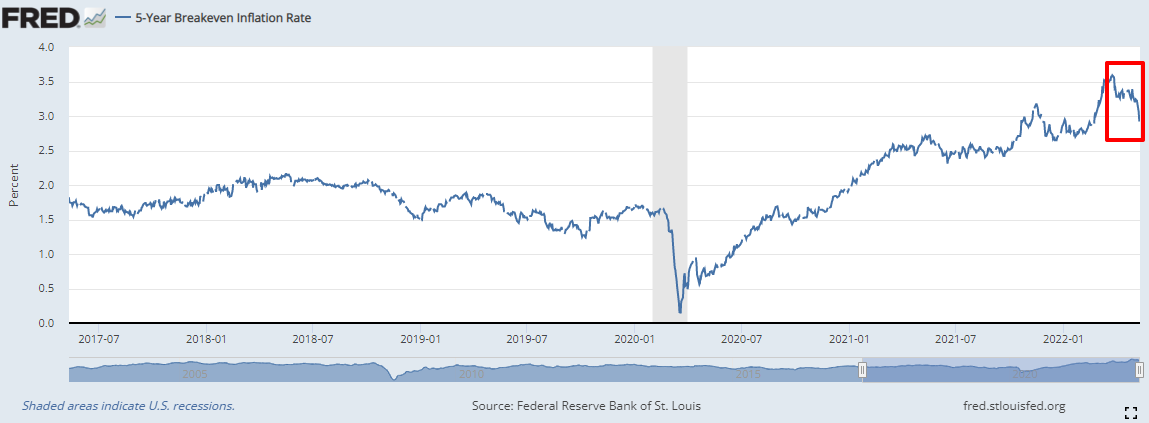

A: There is good news. Rising rates and a slowing economy should bring inflation back down. Eventually, higher prices tend to also bring more supply online (more people come into the workforce if they’ll get paid more, more oil drilling projects if the price of oil is ~$100/barrel, more crops planted if wheat/corn/etc. prices are high). The faster supply increases and demand decreases, the more dovish the Fed can be. While prices will likely remain high, it’s their year-over-year change that matters to the Fed. They don’t want a wage-price spiral to begin and take prices endlessly higher in a self-reinforcing cycle. Now, the market has already priced in massive interest rate increases. Either the economy withstands those increases and continues chugging along (means better than expected growth), or the economy puts on the brakes (means no need to take rates much higher than that, if at all). Either scenario would help stocks find a bottom and start to recover. The real danger is that the Fed raises rates too quickly in its attempt to break inflation and really hurts the economy or they don’t raise rates quickly enough and inflation accelerates from here, causing rates to ultimately have to go even higher in the future. The higher that terminal rate, where the Fed stops hiking, looks to be, the harder it temporarily is on stock and bond values. There are some signs that inflation may start to slow soon though. Using TIPS vs. non-inflation protected treasuries, we can look at what the market is pricing for future inflation. Below is a chart of the 5-year breakeven between the two, a measure of future inflation expectations. The red box shows that inflation expectations have started to decline in recent days.

Q: Ok, here’s the million dollar question… when is this all going to get better.

A: Timing is impossible and no one has a functioning crystal ball (though many in the financial industry will try to sell you one!). I wouldn’t expect an immediately turnaround. But, every time stocks have fallen in the past has turned out to be a buying opportunity in hindsight. Coincidentally, every time stocks have fallen in the past has looked like impending doom. If you’re a net saver, then the lower stocks go, the better for you as your purchases are being done cheaper than if the market never dropped. If you’re a retiree, and a net spender, then much of your portfolio isn’t in stocks and your portfolio has been stress tested to endure well beyond the current drop (if you’re a PWA client that is). I can’t reassure you as to when it will get better. I can reassure you that the timing doesn’t really matter. It will get better eventually and we’ll be in an even better place financially when it does.

There is no free lunch. I’m sure you’ve heard that statement before. As it relates to financial markets, it generally means that you can’t get an expected return above the risk-free rate without taking some level of risk. The higher the potential for return, the more risk must be embedded in the investment. Currently, there is somewhat of an exception, at least for the short-term, courtesy of the United States government.

Savings bonds are generally poor investments for the long-term. There are many types (“series”) of savings bonds and all but one are beyond the scope of this post. The exception, Series I Savings Bonds (“i-bonds”). These bonds are unique in that their variable interest rate is determined by a fixed rate, set by the Treasury at issuance (currently 0% and never below 0%) and a variable rate tied to the CPI (Consumer Price Index). The fixed rate portion is intended to reflect the “real” risk-free rate (i.e. net of inflation), with a 0% floor, while the variable portion is intended to reflect inflation. In this way, i-bonds pay an inflation-protected risk-free rate. Because of the current bout of inflation, the CPI increased by just over 3.5% in the last six months ending in September 2021. The variable portion of the i-bond rate is recalculated every six months based on the annualized change in CPI from the preceding six months. That means that i-bond rate for November 2021 through April 2022 is the 0% fixed rate + 7.12% variable rate = 7.12%. These bonds are backed by the full faith and credit of the U.S. Treasury, meaning they are about as default risk-free as can be and they’re currently paying 7.12%! So what’s the catch? There’s no free lunch right? No catches per se, but there are some things to be aware of…

First of all, that 7.12% is variable and will reset in May of 2022 based on the change in CPI between November 2021 and April 2022. For each six-month period of time, you’ll receive the variable interest rate, which is not known in advance. It’s unlikely to stay anywhere near 7% over the long-term unless inflation persists. Even then, your return will always only equal inflation. In normal times, that’s not much of a goal, but in a world of negative real interest rates, keeping up with inflation alone may appeal to at least some investors. While it’s unlikely to beat equity investments over the long-term, it’s certainly better than a savings account at one of the major banks paying 0.01%. But there are a few more disadvantages here…

Second, you are required to hold i-bonds for a full year from purchase. I know what you’re thinking… there’s always a way around requirements like that (CD’s charge some interest penalty for example, or illiquid investments that can be sold at below-market prices in case of emergency). Unfortunately, there is no work-around in this case. One full year holding period is required and there is no way to liquidate during that time. Beyond the one-year holding requirement, you can liquidate at any time, but, if you liquidate during the first five years, you are charged a three-month interest penalty (e.g. if you hold for 18 months, you only get the interest for the first 15 of those months). Once you’re past five years, the bond becomes fully liquid with no penalty, and you can hold it for up to 30 years when it will mature and stop paying interest.

Third, you can only purchase $10k of i-bonds per entity per year. What does “per entity” means? It generally means per person, but if you have a business or a trust, those entities can purchase $10k per year as well. So there’s no way to park hundreds of thousands of dollars in i-bonds for the short-term while they’re paying this rate and then liquidate them if rates fall over the next few periods.

Fourth, because i-bonds pay interest rather than qualified dividends or capital gains, that interest is taxed as ordinary income taxed at your highest marginal tax rate (meaning your after-tax return is going to be well less than the rate of inflation). On the plus side though, that interest is deferred until the year you cash in the bonds, so you can choose an otherwise low-income year to keep the marginal tax rate down. Also, as an obligation of the federal government, they are state income tax free, which makes them a bit more appealing if you live in a high income tax state.

So, what’s the bottom line? Should you run out and buy $10k of i-bonds as soon as possible? Well, they’re not a great long-term investment, paying a guaranteed after-tax rate that is less than inflation. They’re not a good emergency fund given the one-year holding requirement. But, right now, in a negative real risk-free rate environment, the fact that the fixed rate portion of the bond cannot go below 0% makes them appealing for those who have significant savings in cash, beyond an emergency fund and other liquid assets. If you’re the type of investor who likes to have a surplus of cash, beyond what you’d need over the course of a year in the case of an emergency like a job loss or disability, this can be a good place to park $10k ($20k if married, $40k if married with trusts, $60k if married with trust and two businesses). It can also be a good replacement for part of the (especially short and/or inflation-protected) bond portion of an asset allocation, since it’s going to pay a higher rate of return, at least for now.

If you decide that i-bonds are for you, you can’t purchase them or hold them in a bank or brokerage account and your financial advisor can’t buy them for you. You’ll need to go to www.treasurydirect.gov and buy them directly from the US Treasury. Opening an account is fairly straight forward and you can link a bank account quickly which will allow you to schedule a purchase right away. If your information is mismatched with something in the Treasury databases, you may have to mail in a form with a Signature Guarantee (like a notarization, but obtained from a bank) to prove your identity. This is also likely if you open an account for a Trust or a business. Once the account is opened an a purchase is made, you’ll see interest being credited after the first three months you hold the bond (that’s the three-month penalty you’d incur if you sell in the first five years). You can track the bond values over time as they accrue interest and can purchase more in future years as desired. Just remember, you’ll always earn the fixed rate that was in place when you purchased the bond (currently 0%) + the variable rate for each six-month period going forward.

Over the past two weeks, we have seen unprecedented, by size and speed, Central Bank action. Here’s just some of what I’ve been able to capture:

· US cuts the Fed Funds rate target range to 0-0.25%, down 1.5% via two emergency cuts between scheduled meetings.

· US cuts the discount rate, the rate that it charges banks for loans from its discount window, to 0.25%, lower than during the great financial crisis.

· US re-launches quantitative easing (QE) of at least $700 billion with no cap on total or monthly purchases. In the past, they’ve always capped both. This includes at least $200 billion in mortgage-backed securities. It is purchasing both at ludicrous speed and on Friday, just five days after announcing the program and publishing a planned schedule, announced plans to accelerate from the planned purchases.

· US opened twice-daily short-term repurchase operations of up to $1 trillion. This basically tells banks “if you need any money at all for any reason, we will provide it.”

· US eliminated the bank reserve requirement, the amount of deposits that need to be on hand at any time (which is fine b/c banks can borrow from the discount window if needed), and encouraged banks to temporarily dip into regulatory and capital buffers if needed.

· US reduced the rate of interest on swap lines with foreign central banks in Canada, England, the Eurozone, Japan, and Switzerland (we give them dollars, they give us foreign currency, we charge them interest… now less interest) to ease any dollar shortages that result from a flight to safety.

· US opened swap lines with Australia, Brazil, Denmark, Korea, Mexico, New Zealand, Norway, Singapore, and Sweden.

· US launched the Commercial Paper Funding Facility (CPFF) which allows the Fed to buy commercial paper and for the treasury to cover up to $10 billion of losses. Read this as the Fed is backstopping the short-term corporate lending market.

· US launched the Primary Dealer Credit Facility (PDFC) which effectively provides low-interest loans to primary dealers in return for collateral which now includes corporate debt and municipal bonds.

· US launched the Money Market Mutual Fund Liquidity Facility (MMLF) which provides loans to money market mutual funds in exchange for loans that the funds hold. As individual and businesses liquidate money market funds during the current cash crunch because of the economic pause, this prevents the funds from having to sell illiquid short-term loans in a fire sale. Instead, now they can give them to the Fed for cash to handle fund redemptions and not “break the buck”. Treasury provides $10 billion for any losses.

· In summary, the Fed is either outright purchasing or accepting as collateral: treasuries, mortgages, commercial paper / corporate debt, and municipal bonds (state/local government debt). There are limits on term and quality which can be expanded. There are limits on who can borrow with collateral (banks and primary dealers), which can also be expanded further. As of right now, the Fed cannot purchase preferred stock or common stock under their current powers. I say “current” because powers can be changed by Congress or, in some cases (maybe with legal challenges) by Executive Order in times of emergency.

· Bank of Japan (BOJ) doubled its ETF purchase plans (that’s right, the BOJ actually prints money to buy funds that hold stocks, and they’re buying more!!!) for 2020. They increased their corporate bond buying plan by almost 50% for 2020.

· European Central Bank (ECB) expanded QE, is allowing banks to borrow cash at -0.75% (that’s right, the ECB will pay their banks to borrow money from them). They also launched a 750 billion euro Pandemic Emergency Purchase Programme to purchase the debt of EU countries, as well as lower quality debt. That’s ON TOP OF their existing purchase plans.

· Canada cut rates to 0.75% and launched QE via mortgage purchases.

· UK cut rates to 0.1%, increased existing QE bond purchases, eliminated their bank reserve requirement, and launched a new term funding arrangement that provides up to 100 billion pounds of 4-year loans to banks to provide low interest loans to individuals and companies.

· Australia cut rates to 0.5% opened a fund for lending to banks, and launched QE via purchases of government debt to controlthe 3-year borrowing rate at 0.25%.

This doesn’t even take into account the fiscal response across the world as virtually every government spends money it doesn’t have to help their economy get through this. The buying of government debt by central banks via quantitative easing is what makes that possible. So what’s the end game here? Central banks and national governments have shown their respective hands. In a coordinated manner, they will do everything to not let the global economy spiral into deflation. Deflation causes the price of everything to come down, encouraging anyone who wants to buy or invest to wait until prices fall further, which inevitably makes prices fall further due to lack of demand. It is a chain reaction that can lead to long-lasting depressions. If they print money to afford government spending and cash to individuals as support for this economic pause, they can offset the economic damage the pause would cause. This risks massive inflation in the future since increasing the supply of money and giving everyone their share of it, just increases demand for everything, thereby pushing up prices. In the simplest example, imagine if the government decided to match dollar for dollar, what everyone has in net worth. Everyone would feel richer. Bids for homes would rise immediately. Stock prices would rise due to flood of investment. Commodity prices would rise as global demand for everything increased. Everyone would be spending money at a pace never before seen leading to shortages everywhere from increased demand. The only response will be prices increasing sharply and dramatically until they are about double where they were before the government’s action. Then everything stabilizes (gross oversimplification) right back to where it was before with two times the money available and everything costing twice as much. In a sense, government and central bank action is walking a tightrope of trying to offset reduced demand due to the economic shock without causing too much demand that creates inflation. On which side will they land? Like I said, they tipped their hand already. Expect more from central banks as needed to get through the crisis. At some point, financial markets will realize what lies on the other side… a whole lot of money looking for a place to go.

Note: As I wrote this, the Financial Times announced that the UK plans to buy stock in their airlines and other companies affected by the pandemic. The bazooka keeps getting bigger, from the monetary and fiscal sides.

The IRS has released the key tax numbers that are updated annually for inflation, including tax rates, phaseouts, standard deduction, exemption amount, and contribution limits. Since inflation was relatively low in 2017, only small changes have been made in most cases. Note that all of this is subject to change if new tax legislation is passed in 2017 (doubtful) or in 2018, retroactive to 1/1/2018 (I’d give this a 50% chance). Some notable callouts for those who don’t want to read all the way through the update:

· Social Security payments will increase by 2.0% in 2018. The Social Security Wage Base (the max amount of income subject to the 6.2% Social Security Tax) increases from $127,200 to $128,700.

· Max contributions to 401k, 403b, and 457 retirement accounts increases by $500 to $18,500 (+$6000 catch-up if you’re at least age 50).

· Max contribution to a SIMPLE retirement account remains unchanged at $12,500 (+$3000 catch-up if you’re at least age 50).

· Max total contribution to most employer retirement plans (employee + employer contributions) increases from $54,000 to $55,000.

· Max contribution to an IRA remains unchanged at $5,500 (+$1,000 catch-up if you’re at least age 50).

· The phase out for being able to make a Roth IRA contribution is $199k (married) and $135k (single). Phase out begins at $189k (married) and $120k (single).

· The standard deduction increases by $300 to $13,000 (married) and by $150 to $6,550 (single) +$1,300 if you’re at least age 65.

· The personal exemption increases by $100 to $4,150 per family member. Remember that exemption amounts begin to be phased out if your income exceeds $320,000 (married) or $266,700 (single). The exemption is reduced by 2% for every $2500 of AGI over threshold until reduced to $0.

· Itemized deductions are reduced by 3% of the amount AGI is over $320,000 (married) or $266,700 (single).

· The annual gift tax exemption increases by $1,000 to $15,000 per giver per receiver.

· The maximum contribution to a Health Savings Account (HSA) increases to $6,900 (married) and $3,450 (single).

· Standard mileage rates have not been updated yet for 2018.

The Federal Reserve Open Market Committee (FOMC) today announced a new program of quantitative easing that goes above and beyond all previous actions they’ve taken to stimulate the economy. For the past several years, the Fed has been buying primarily long-term treasuries with essentially newly printed money, in an attempt to inject liquidity into the economy and keep long-term treasury rates (the rates that long-term loans like mortgages rely on) low. The new program announced today, which goes into effect starting tomorrow, has the Fed buying mortgage-backed securities in the amount of ~$40 billion per month with no fixed end date. The purchase of these securities should directly lower mortgage rates (all else being equal) and allow for another wave of refinances for those who qualify. The purchases themselves were mostly expected by the market given lackluster economic growth and an anemic job market. But, the open-ended nature of the purchase program is the bazooka of monetary weapons.

Ben Bernanke, chairman of the Fed, indicated that the Fed will continue the monthly purchases until economic conditions improve. Read another way, that means the Federal Reserve will continue print money until there is enough money to go around. That money will flow into the economy through lower mortgage and other loan payments for borrowers and through the reduced incentive to hold cash savings since interest rates are virtually zero. If $40 billion per month isn’t enough, they’ll do more. If mortgage-purchases aren’t enough, they’ll print money to purchase other assets too. It’s a commitment that essentially puts a floor under the economy and under asset prices, thereby removing the risk of deflation. Without the risk of deflation (think of housing prices falling), the desire to purchase assets can return (think of people in their early 20’s deciding to buy condos again instead of renting). While the ramifications of the commitment will take a while to filter through the economy, they should result in the following:

· Lower mortgage rates for those with good credit attempting to obtain conforming loans (loans for principal residence that are under the FHA loan limits for the county of residence – typically $417k)

· Another wave of refinancing reducing payments for existing borrowers and freeing up more for discretionary spending

· Reduced risk in house price declines leading to more buyer confidence leading to a bottom to the housing market

· Higher business confidence that the economy will not “double dip” back into recession (the Fed simply won’t let it happen)

· A very gradual improvement in the job market

· A continuing erosion in the value of cash (no interest paid and the cost of living will start to increase more rapidly, especially in volatile food and energy prices)

· Higher inflation (virtually a guaranteed byproduct in eliminating the risk of deflation), higher energy prices, higher food prices.

It’s that higher inflation that will be the next big economic problem in my opinion. How fast it happens is unknown, but when it does, the Fed will have to reverse course and start extracting stimulus or face a 1980s-like bout of hyperinflation. Their forecasts are for that to occur beyond 2015 (they currently promise to keep rates low through 2015 and wouldn’t do that if they didn’t think inflation would be in control through at least that year). I’m not so sure, since I think a promise for an unlimited amount of stimulus could very quickly cause inflation expectations to become unanchored. Either way, taking deflation, double-dip recession, and maybe even depression off the table is certain to be a short-term net positive on the economy in aggregate. It’s also virtually certain to make cash have less and less value over time. So, what should you do to take advantage of today’s changes:

1) Only hold enough cash to serve as an emergency fund and to pay for short-term upcoming lump-sum purchases.

2) Avoid long-term fixed-income commitments (long-term bonds, long-term cd’s, fixed annuities without an inflation rider).

4) If you’re renting, you live in an area where house prices are reasonable in relation to rent, and you have enough money for a 20% down-payment, consider buying a house. I’ve been very patient in delivering this message but my confidence is now fairly high that affordability (based on the mortgage payment you’d expect given home price and interest rate) will peak by Spring ’13.

Most of all, stay alert and stay flexible. Today’s announcement is unprecedented and therefore at least partially unpredictable. Bazookas are powerful, but they’re not the most precise weapon and they may have some collateral damage. If we’re using imprecise, extremely powerful, and somewhat unpredictable tools to try to control the economy, the result, well, let’s just say this is probably not the final chapter of this economic cycle.

*** We believe communicating with our clients is of utmost importance, especially during turbulent times in the market. While we don’t claim to have a crystal ball on the future of any financial market at a given point in time, we do believe that keeping clients informed on why things are happening increases their comfort level and understanding. This post contains a message initially sent to clients just after the start of Q3 2012 as part of that communication effort***

Q2 2012 proved to be yet another roller coaster quarter in the financial markets led mostly by continuing debt problems plaguing European governments & banks, and the economic slowdown driven in part by fear and in part by the austerity measures that are being put in place to try to rectify the debt overhang. After losing much of the Q1 gains through the month of May, markets rallied back in June on hopes of progress in Europe following the latest Greek elections (a win for the party that wants to stay in the Euro), a hint that Germany may be willing to concede to a cross-country banking union of some sort, and the extension of Operation Twist by the U.S. Federal Reserve (thereby also extending hope of more easing in the future). US stocks a whole lost just over 3% for the quarter, with international stocks losing just over 7%. U.S. interest rates continued to fall with short-term rates pinned near zero and long-term rates plunging to historic lows (U.S. 10-year yields just under 1.6% as I type this note). This helped bond funds to perform fairly well in aggregate, up about 2% for the quarter. Commodities fell on global growth concerns, down 4.5% for the quarter with energy components leading the way down. While investments in commodities lost value, the economy as a whole likely felt some relief from declining energy prices which helps consumer confidence and more importantly, consumer budgets. As we noted in our Q1 update, we expect risk assets like stocks and commodities to continue to remain volatile, both up and down, for the short-term, with bonds in aggregate generating fairly constant, albeit low returns. Interestingly, the national average rate on a savings account is now 0.12%. While it doesn’t get much safer than an FDIC-insured savings account, with year over year inflation running close to 2%, that’s a guaranteed loss of almost 2% per year by keeping money in cash.

While much has been blamed on Europe over the last two years, the U.S. faces its own issues heading into 2013. At current pace, we borrow approximately fifty cents of every dollar we spend as a government. This completely unsustainable way of running of the country will take its toll at some point in the future. The good news is that we seem to know that we have a problem. The bad news is that the method by which we fix it is heavily debated by our two political parties, each seeming to move toward a more extreme position as time goes by. It would be difficult to call them deadlines, but at least strong milestones loom in the not too distant future with the major credit ratings agencies noting that if the U.S. doesn’t come up with a credible plan for reducing the deficit by the start of 2013, another rating downgrade will follow. As current law stands, three dramatic changes are scheduled to be implemented in 2013. These have become known in aggregate as “The Fiscal Cliff”. They include the sequestration of defense spending budgets, the repeal of the 2001 & 2003 tax cuts which will increase tax rates on everyone who pays U.S. taxes, and the next steps in the implementation of the new healthcare laws which will institute a new Medicare surtax on certain individuals. If these changes go into effect, they combine spending cuts with tax increases in a slowing economy that is plagued by high unemployment already. This dramatically increases the possibility of another sharp recession. If the changes don’t go into effect and no other credible plan is put into place to balance the budget over time, the credit worthiness of the U.S. will come into question. If/when that happens, borrowing costs will start rise, putting more pressure on the budget (higher interest payments) and that spiral of debt that is all too familiar in southern Europe could attack the U.S. in much the same way. The answer to this problem in our opinion is one that Congress will get to eventually. That is, easing the Fiscal Cliff for the short-term and simultaneously publishing a credible plan for the long-term, likely through an overhaul of the tax system and a review of programs like Social Security and Medicare that are growing to levels we can’t support over the long-term. What’s not clear is whether the will exists to accomplish this before sharp and severe economic realities hit.

Led by the election in November, we believe the issues in the U.S. will come to the forefront over the next few months. It is likely that the stock market will gyrate, perhaps wildly at times, as solutions are brought forward and political power for the next 2-4 years is revealed. Further stimulus by the Federal Reserve, possibly in a coordinated effort with central banks around the world, will become more likely if economic conditions deteriorate. Monetary stimulus would continue to provide a temporary floor to the economy and to asset prices by simply pumping more money into the banking system. If the Fed does this, cash is one of the worst places to be as interest rates will continue to near zero while inflation would likely pick up as more money enters the financial system.

What all of this means is that we’re unfortunately stuck in the middle of a potentially deflationary bout of economic deterioration (where we’d want to hold cash and bonds and avoid stocks and commodities) and a potentially inflationary move by the Federal Reserve and other central banks to offset that economic deterioration (where we’d want to avoid cash and bonds and own stocks and commodities). The market in aggregate continues to do a very good job of pricing the risks to both sides. The current best course of action is to maintain asset allocation targets and continue to take advantage of volatility through portfolio rebalancing. We are monitoring the economic landscape closely and are prepared to take action if risk/reward does come out of balance in the coming months. If the market rally significantly from here on a perception that the world’s problems are solved, we will likely move toward more conservative portfolios by adjusting all models and using hedging positions where appropriate. For now though, we believe the inflation/deflation scenario is well-balanced and that stocks, especially in comparison to other asset classes, remain well-priced.

More on the fiscal cliff, stock valuations, Europe, and a host of investment and other personal finance topics will be presented on the new PWA blog which is officially live as of today (blog.perpetualwealthadvisors.com). In future quarters, rather than sending you emails like this, we’ll be posting shorter, more easily digested ruminations on the blog. You can subscribe to receive emails on new blog posts if you prefer to receive the content in your inbox rather than on the sites. Our Facebook and Twitter pages are also live, though with each still under construction and notably light on content (as is the case for all new pages). We’ll rectify that shortly. Feel free to provide encouragement by “Liking” & “Following” us. You can find links to all the pages via the icons in the signature below. For those of you who have made it this far into reading this email, you’ll be receiving a second notice about the blog, Facebook, and twitter pages in the coming days specifically because I’m guessing only a few of you made it this far (which I find as solid confirmation that a blog will be more useful than long emails each quarter). You have my apologies in advance for the double notice. As a reward however, reply to this message with a suggestion for a future blog post topic and you’ll be entered into a drawing to receive a gift card at the end of the quarter. As always, if you have any questions or comments about this message or anything else, please don’t hesitate to ask. Thanks for reading and enjoy the rest of the summer.

*** We believe communicating with our clients is of utmost importance, especially during turbulent times in the market. While we don’t claim to have a crystal ball on the future of any financial market at a given point in time, we do believe that keeping clients informed on why things are happening increases their comfort level and understanding. This post contains a message initially sent to clients just after what turned out to be the market bottom in March of 2009 as part of that communication effort***

With so much focus on the seemingly endless economic collapse that is happening around us I’ve been looking forward to begin able to send a more optimistic update for quite a while. Toward the end of 2008, I provided a few regular updates to all of you as events unfolded that led us into this decline. Over the last week, much has changed and while I’m sure it won’t get as much TV airtime as the bad news did, it’s just as important. Many of you know by now that the stock market rallied more than 7% today. This followed previous rallies over the past two weeks such that the market is now up more than 20% from its recent lows. Many regard the stock market as a view into what is around the next corner for the broader economy. This was certainly true last October when the credit markets froze, the stock market fell 25% in a week, and the real impact hit most people a few months later when layoffs rapidly accelerated. Similarly, I suspect the events of the last week, including today, will not be felt by Main St. until mid to late summer when those layoffs will slow down or cease. So, I wanted to provide a similar update to you now on what has changed, and why the market is reacting the way it did today.

To some of you in our conversations, I’ve already described the announcement by the Federal Reserve last week as a “game-changer”. In case you don’t know what I’m talking about, let me summarize what the Fed said they’re going to do. First some background. We all know that the government is spending a ton of money right now and that we don’t have enough tax revenue to pay for it all. This is commonly known as “The Deficit”. Years of deficits have added up to a very large national debt of just over $11 trillion, or some $36,000 per U.S. citizen. The debt is financed by issuing government bonds called “treasuries”, which are purchased by individuals, corporations, and foreign nations. Because the U.S. has a very stable political system and has never defaulted on its debts in the past, it is considered credit worthy and lenders don’t demand a very high rate in return for their money. But, the deeper the hole we dig, the greater the interest that we have to pay on our debt. As that interest becomes a bigger and bigger slice of the tax revenue, it creates some risk that we might not pay our debts off. This risk would push interest rates up, just at a time that the government wants to keep them low for investment, refinancing, etc. So, we seem to have to choose between deficit spending (needed to turn the economy around) or low interest rates (also needed to turn the economy around). Quite the dilemma. Meanwhile, the recession continues to take its toll on asset prices (stocks, real estate, commodities, etc.). To put it simply, there is just less money out there than there used to be which means people can’t afford to pay what they previously could for similar assets. This creates a deflationary spiral where asset prices are falling because of the recession, and the recession is deepening because of falling asset prices. To combat this, the Fed announced last week that they will now be buying treasuries directly from the Treasury to finance the deficit, and mortgages directly from mortgage lenders to free up capital for new lending and keep mortgage rates low. Where will they get the money? Good question. Believe it or not, they’re just printing it.

Printing money is highly inflationary. If we just double the amount of dollars in the economy, then we double the demand for everything which raises prices until it takes two dollars to buy what we used to be able to buy with one dollar. No one is wealthier, but because prices are rising so quickly, people start to hoard assets pushing up prices further, which can start an inflationary spiral. But, if we’re in a deflationary spiral now, putting some seemingly inflationary actions into play could break the spiral. If done carefully, we’ll end up perfectly replacing the lost wealth that is pressuring the economy which will put a floor under asset prices and return confidence to the normal buyers of those assets. In short, the recession will end and growth will be restored… a game-changer. Things won’t get better overnight, but for the first time in several months, I believe recovery is in sight and that the economy will begin to slowly stabilize over the next 3-6 months. Note that by stabilize I don’t mean the Dow returns to 2007 levels, that unemployment returns to 5%, that housing prices start increasing 10% per year, and that things feel “normal” (per 2004-2006 expectations) again. I mean that stocks will stop falling, unemployment will stop rising, and we’ll have time to get used to the new normal (stable, sustainable, moderate growth). It’s likely that the stock market today and over the past couple of weeks senses this as well, and is pointing toward signs of recovery.

In some additional good news, the Treasury today announced their long-awaited plan for handling illiquid mortgage-backed securities commonly known in the press as “toxic assets”. The plan includes a public-private partnership that will team up private capital, government programs such as TARP (the name for the $700 billion “bailout” that Congress passed in December), and the FDIC to purchase and create a market for these previously illiquid assets. Without a market to sell them, banks were forced to keep ownership despite their rapidly declining value and uncertain future. This in turn rattled investor confidence and prevented banks from raising new capital from private markets; hence the need for government bailouts. The details of the program make a lot of sense, with the private investors determining what price they’re willing to pay for the assets via an auction process, the government backing their investment in a way that will reward them for taking risk while also rewarding taxpayers alongside the private investors, and no penalties for banks that participate in a sale of their assets. As stated currently, this program should be another big positive for both the markets and the economy.

Before we sound the “All Clear” signal, we have to realize that along with all the positives come some greater risks as well. Buying treasuries and mortgages is bold action by the Fed and while it is likely to end the recession in the medium term, if it’s not done carefully, it will lead to potentially bigger problems down the road. We could face runaway inflation, lost confidence in the dollar as a currency, and political tensions with other nations who suffer because our actions devalue the dollar that they own a ton of in the form of our debt (the financial engineering equivalent to highway robbery). The Treasury, the Fed, and the Federal government will all have to work together to cut spending, remove excess dollars, and reign back the flood of liquidity as soon as confidence is restored and the recession is over. If they don’t, $140 oil will seem like a bargain compared to the prices we’ll be paying in a few years!

In addition to the risk of inflation going forward, there is another risk that is worth mentioning. The government is beginning to meddle in the private markets in ways that could hurt the willingness of corporations to do business with them in the future. Last week, the House passed a bill that would tax AIG bonuses at a 90% rate as a way of punishing the firm for paying bonuses after taking government money via the TARP program. While I think we can all agree that rewarding failure at the expense of the taxpayer is not what was intended by TARP, we have to be very careful in retroactively changing the rules on government programs. When TARP was passed there were no stipulations on how the money could be used. While the focus is on AIG who took the money to keep their business afloat, many firms took TARP money so that they could provide additional loans to homebuyers and businesses that needed credit. Now, the government is imposing additional rules on executive compensation for all companies that took TARP funds. If you change the rules in the middle of the game, it’s possible that no one will play with you anymore. In this case, many companies are now seeking to return TARP money which would cut off the added credit to the economy and reduce the effectiveness of the program. This government behavior could also cause skepticism of the new public-private partnership announced today. If there’s danger that participating banks may face new rules 3 months into the program, they may not want to participate at all. Congress needs to make sure that it writes all the rules ahead of the release of programs like TARP, and whatever those rules are, that it consistently enforces them without modifying them midstream. If we have a fair and consistent set of rules, which encourage participation in government sponsored programs to stimulate the economy, then those programs stand a chance of working. If not, we’re just wasting our time creating the programs that no one will use and the downward spiral will continue.

In conclusion, let me be clear… I’m not claiming that the worst is over for the economy. There will be more layoffs, there will be more housing price declines, and there will be more foreclosures as the current damage flows through the system. But, over the next few months, these new programs and the lack of new damage will stabilize the economy and it will eventually begin to grow again. I’m also not claiming the stock market has necessarily bottomed. The short-term stock market is too unpredictable to say with certainty what will happen over a matter of days. But, IF the risks stated above are controlled, and that is a BIG IF, then I believe these plans are likely to stabilize the market. That is why we saw the gains we saw today and why we probably have seen the last of the 20% monthly market drops for a while.

As always, if you have any questions about this update or anything else, feel free to contact me.