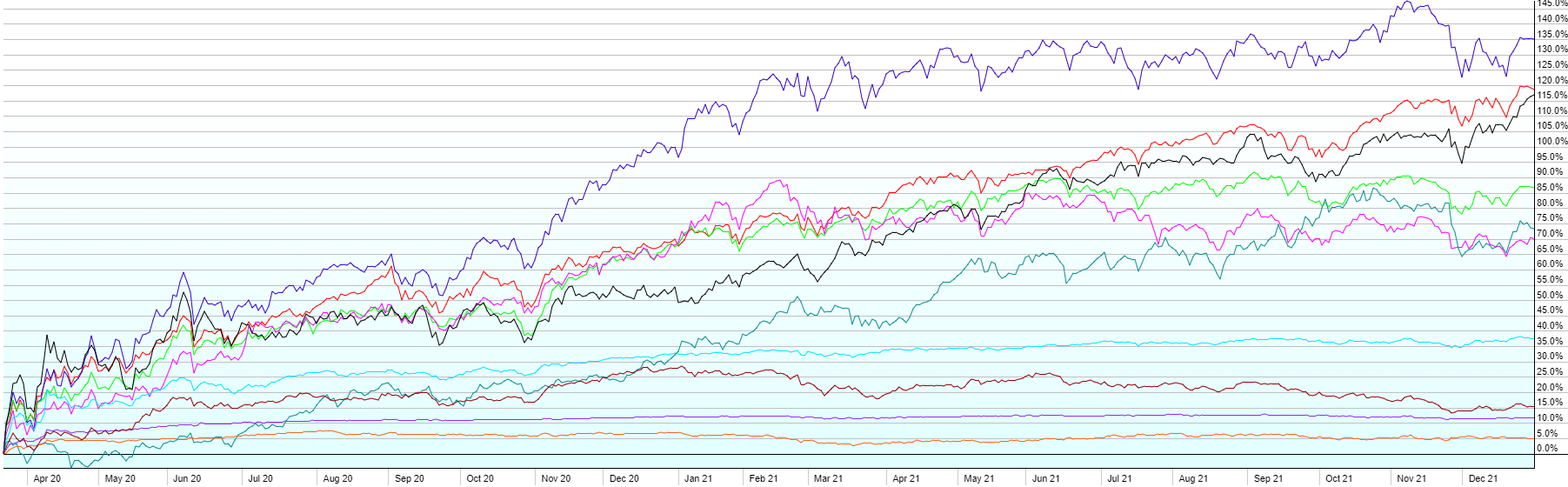

This post contains the usual returns by asset class for this past quarter (by representative ETF), last year, last five years, last ten years, and since the covid low (3/23/2020). While there is still no predictive power in this data, I’ll continue to post this quarterly for those of you that are interested.

A few notes:

- Q4 was a very strong quarter (with a mid-quarter dip) for US Large Cap (+11%) and US Real Estate (+15%), but other asset classes fared substantially worse. US Small Caps still did well (+4%), but underperformed. Foreign stocks did worse with Developed Markets (+3%) and Emerging Markets (-0%) finishing down slightly on the quarter. US Bonds were flat to down 1% with Emerging Market Bonds down 3%. Commodities finished down ~2% after rallying strongly for the past two quarters.

- For 2021 as a whole, the only truly poor performing asset class was Emerging Market Bonds (-10%) as the U.S. Dollar rallied and fears of a liquidity crunch in emerging markets dominated as the Fed begins to pull back on stimulus and even start raising rates in 2022. US significantly outperformed Foreign stocks as well. Real Estate (+41%) and Commodities (+29%) won the year as interest rates remained low as inflation spiked.

- US Large Cap (S&P 500) has dominated over one, five, and ten years. The largest US stocks have performed best and gotten even larger, year after year. The top 2 companies in the S&P 500 (Apple and Microsoft), now make up 11.5% of the index. The top 10 make up 27.4% of the index. Diversified portfolios that include the other asset classes have underperformed as a result. Eventually though, this tide will reverse and smaller stocks will outperform larger ones. Foreign stocks, especially emerging markets, are about as cheap as they’ve ever been relative to the U.S. How long the dominance of a handful of US stocks can continue is anyone’s guess. But, the odds seem to favor a diversified portfolio outperforming the S&P 500 over the next few years.