Yesterday, the IRS issued this statement with regard to the tax deductibility of prepaid property tax. In it, they state that the property tax must be both assessed and paid in 2017 in order to be deductible in 2017. The statement is just a reminder/clarification, not a new rule. It follows with what I wrote in my last post about prepaying property taxes… “Be aware though that in most cases, if the county accepts the prepayment as a deposit placed in an escrow account, it is not considered “paid” for Federal tax purposes. It has to be paid against a levied tax to be deductible.” If there is no tax yet, then your county could just be putting your prepayment in a suspense or escrow account and that is definitely not deductible. If your tax has not yet been assessed, then there is no tax bill to prepay and that means your situation is the same as the 2nd example in the IRS statement. Clearly not deductible. If the tax was already assessed and payment isn’t due until sometime in 2018, or if they are taking your payment, levying a tax to offset it, and applying the payment against a levied tax (with amount not finalized, but known to be at least as much as last year), then that should be deductible. I highly doubt many counties are going through that level of trouble though. Most likely, either the tax has already been assessed and you’ve been notified of it, in which case payment would be deductible if make by 12/31/2017, or the tax has not been assessed and is not deductible for 2017, regardless of when it is paid.

Month: December 2017

Pre-Paying Property Taxes

For those of you who are looking into making extra property tax payments in 2017 per this previous post in an attempt to make payments deductible in 2017 that would may not be deductible for 2018, I compiled a list of relevant (to my clients) states and their policies on prepayment. In some states, even if the official property tax bill(s) for calendar year 2018 haven’t been published, they will accept pre-payment. Be aware though that in most cases, if the county accepts the prepayment as a deposit placed in an escrow account, it is not considered “paid” for Federal tax purposes. It has to be paid against a levied tax to be deductible. This information is posted for reference only and is not a substitute for communicating directly with your tax collector and/or a CPA, EA, or tax attorney. Use it as a guide to get started, not as the law. Here’s what I’ve found so far:

California: taxes are managed at the county level but it appears that for all counties payment #2 for fiscal 2018 is due in early 2018 (payment #1 was due in late 2017). These bills have been published and the amounts are known. If you want to make a pre-payment, simply pay your 2nd payment prior to 1/1/2018.

Georgia: taxes are managed at the county level. For Dekalb and Cobb counties, there is no mention of prepayment of taxes for 2018 on their websites. They just collected 2017 taxes in the Fall of 2017, so there is no assessment nor bill for 2018 yet. However, they may still accept a payment for 2018. Call the county tax office for details. For Fulton county, due to issues I don’t fully understand, their 2017 tax bills were issued later than usual. Residents in the City of Atlanta have a due date of Dec. 31, while residents in Fulton County have a due date of Jan. 15, 2018. Pay by 12/31/2017 if you want the payment to count for 2017’s Federal taxes. For 2018 pre-payments, again, call your county tax office.

Illinois: taxes are managed at the county level. In Cook county, taxes are paid in arrears. 2016 taxes were paid in 2017. 2017 taxes are due 55% on 3/1/2018 and 45% on 8/1/18. The county website indicates that they are now accepting prepayments for the 3/1/2018 portion, but makes no mention of the 8/1/2018 installment. Call your tax collector for more detail if you’re interested in paying beyond the first installment.

Maryland – taxes are managed at the county level. For Baltimore County, tax payments are divided into two installments. The first installment is due on July 1 of the tax year and may be paid without interest on or before September 30 of the tax year. The second installment is due on December 1 of the tax year and may be paid without interest on or before December 31 of the tax year. So, all tax bills for 2017 should be paid by end of calendar 2017. I haven’t found any information about pre-paying 2018 taxes in Baltimore County, but Howard county just announced that it is accepting pre-payments for 2018 and will hold those payments in escrow until bills are generated. I expect other counties to follow suit. Contact your tax collector for more details. Be aware though that in most cases, if the county accepts the prepayment as a deposit placed in an escrow account, it is not considered “paid” until they accept it against an levied tax, so you may still not get a deduction for it.

Michigan – taxes are managed at the county / city level. For Detroit and the rest of Wayne county, tax bills are divided into two installments. The first is due 8/15 and the second is due 1/15 of the following year. You can make your 1/15 payment by 12/31 for it to count toward 2017 Federal taxes. I haven’t found any information about pre-paying 2018 taxes so call your county tax collector to inquire.

Minnesota: taxes are managed at the county level, but at least for Hennipen county, they are accepting prepayments based on the amount stated in your proposed property tax (Truth in taxation ) notice sent in November 2017. Payments must be received (not postmarked) by the county by 12/29/17 to process for 2017 and they may be made in person or by mail. Other counties probably have similar policies so check with your county tax collector if you want to pre-pay. For Hennepin County, see their website for more info.

New Jersey: the annual property tax bill is due 25% each quarter on 2/1, 5/1, 8/1, and 11/1. I believe you should already know the 2/1/18 and 5/1/18 payment amounts so those could easily be prepaid by 12/31/2017 if you want them to count for 2017 Federal tax. I have no information about pre-paying beyond 5/1/18. Call the county tax office for more info.

New York: there are two types of tax bills each year: 1) School and 2) Municipal and County. School tax bills are typically mailed in Sep each year, with due date varying by district. Municipal/County bills are typically mailed in Jan each year, with due date varying by locale. If your School tax bill hasn’t been paid yet, you can definitely due that by 12/31/2017 if you want it to count toward 2017 Federal tax. For the Municipal/County bill, call your tax office and ask if they can give you the amount that will be on the January 2018 bill and if you’re allowed to pay it by 12/31/2017. There is no mention on state websites I looked at about pre-paying Municipal/County taxes for the following year. That would be taxes not due until 2019 so I doubt that would be allowed, but check with your county tax office to inquire.

Update 12/23 – per Jeff Levine, CPA via Twitter: ” Interesting… NY’s Governor Cuomo has signed an executive order allowing the early payment of 2018 property #taxes in order to help New Yorkers impacted by the #TaxReform‘s new SALT restrictions #TCJA“

North Carolina: taxes are managed at the county level. I checked Mecklenberg and Union counties and both show due dates for 2017 tax of September 2017, but no interest will be due if paid by 1/5/2018. If you want your 2017 tax payment to count for 2017 Federal tax, pay by 12/31/2017. For 2018 prepayments, policy seems to vary by county but I was able to verify that both Mecklenburg and Union counties are accepting pre-payments by check with parcel number and “prepayment” noted on the check. Incidentally, I’m writing this at 3pm on 12/21 and Mecklenburg County issued their policy at about 2:30pm on 12/21.

Pennsylvania – taxes are managed at the county / city level and the procedures vary greatly by municipality. In Philadelphia tax bills are mailed in December for the following year and are due in March. So you can definitely pay 2018 property tax bills in 2017 if you make payment by 12/31/2017. In Delaware County, bills are mailed 2/1 and are payable at a slight discount through 4/1, full amount through 6/1, and with a 10% penalty through 12/31. Call your tax collector to inquire about prepaying the following year’s taxes if you wish to do so.

South Dakota – Property tax bills are divided into two payments. The first half of the property tax payments are accepted until April 30th without penalty. The second half of taxes will be accepted until October 31st without penalty. So 2017 taxes have already been paid. I haven’t found any information about pre-paying 2018 taxes so call your property tax collector to inquire.

Texas: 2017 property taxes are due 1/31/2018. If you want them to count as a deduction for 2017 Federal tax, pay them by 12/31/2017. There is no mention on state websites I looked at about pre-paying 2018 taxes. That would be taxes not due until 2019 so I doubt that would be allowed, but check with your county tax office to inquire.

Virgina – taxes are managed at the county level. Most counties seem to have tax due in two installments during the calendar year. The counties I researched, including Fairfield County appear to be accepting prepayments of 2018 property taxes. They need to be paid (not postmarked) by 12/26 to be credited as paid in calendar 2017.

Washington: 2017 tax bills have already been paid. It is against state law for county tax collectors to accept payments for 2018 taxes during calendar 2017 per the Kings County website.

Calling your city/county tax collector and specifically asking if they will accept prepayment (and by what method) is the best way to get an accurate answer. Many counties still appear to be figuring this out, so there’s a lot of changing / stale information out there.

Remember, if you’re in AMT for 2017 already, without the additional payment, then this will not help you. But, the only way it hurts you is if the 2018 tax law changes again and would have made the payment deductible in 2018 (seems like a low probability), if your state/local income/property tax deductions would be less than $10k in 2018 (meaning you could have deducted the property taxes in 2018 instead), or if it’s tying up money you otherwise need for something else, leading you to take on debt or make other inefficient financial decisions. So, if you can pre-pay your 2018 property taxes, unless you know for sure that it won’t help you to do so, you can consider doing it.

Other (Less Urgent) Things To Do Regarding The Tax Bill (TCJA)

The following is a quick brainstorming list of things to think about doing if/when the TCJA becomes law. They don’t need to be done before the end of 2017 so I carved them out separately from my previous post.

- Update your tax withholding to account for your new level of deductions. Note that IRS guidance on this may be delayed until late Jan / early Feb due to the complexity in calculations.

- Payoff HELOC debt if the loss of tax deductibility makes the after-tax interest rate cost prohibitive vs. other options.

- Revise estate plan (if necessary) to account for bigger exemption. Consider lifetime gifting plans to take advantage of the bigger exemption if estate tax may be an issue for you in the future.

- Increase 529 contributions to account for private K-12 expenses if you know you will incur those expenses.

- Keep in mind that alimony will not be deductible to the payer / taxable to the receiver starting with divorces that take place after 12/31/18 (the bill gives one extra year to prepare for this).

- If you have any children with financial accounts in their names, review the new “kiddie tax” rules and plan accordingly as their tax system has shifted to follow the trusts and estates rates.

- If you have an AMT credit, likely due to the exercise of an Incentive Stock Option, without a corresponding sale in the same year, prepare for that credit to get “released” more quickly (i.e. larger credit each year until fully used).

- Note that the floor for deducting medical expenses in 2017 and 2018 only, is changing from 10% to 7.5% (if you’re able to itemize). For some, this may mean tracking their out-of-pocket expenses and providing them to their tax preparer at tax time. Again, this is retroactive and applies to 2017.

- Since unreimbursed employee expenses are no longer deductible, the days of keeping mileage logs to take a tax deduction for use of your vehicle for work as an employee are over (unless required for your employer to reimburse you). In a related note, if you use your car for work as an employee (outside of commuting) and your employer doesn’t pay for that mileage, it’s worth discussing that with them since you are no longer going to be able to deduct the mileage for tax purposes.

- If you own a business, client entertainment is no longer deductible. Meals are still 50% deductible. Keep that in mind when setting up events if the tax treatment matters.

- Employers can no longer reimburse employees tax-free for moving expenses. Any moving expense that an employer pays will be considered taxable income. If you’re signing on with a new employer and they say they’ll pay for moving expenses, ask them to “gross up” those payments such that you are made whole after-tax. If they refuse, note that they’re really only paying / reimbursing you for 55-80% of the net moving cost.

What To Do (or not do) In 2017 Regarding The Tax Bill (TCJA)

The House and Senate have now passed the tax bill (though the House needs to vote again after some minor amendments in the Senate) and then it will be on its way to the President for signature. While anything is possible, and the odds of the President signing in January rather than December have increased dramatically, it seems safe to assume that the bill will eventually become law. There’s not a ton of time left to take action and there aren’t a lot of people who can take any action to take advantage of / avoid the disadvantages of the new tax law. In this post, I’ll outline what you might be able to do, why you might be able to do it, and (maybe most importantly) why it may not work in certain situations. These are general rules. Proceed with caution. Things can get very complicated and unintended consequences are possible. The bill has not yet become law and there is some small risk that something prevents it from becoming law which means that actions you take under the assumption that it will become law may backfire. I tried to keep this list simple, but unfortunately, there’s just no way to do that while providing enough actionable information. Taxes simply aren’t simple. Thanks Congress!

Consideration #1

Because: Federal tax rates are falling for every tax bracket in 2018,

Consider: Deferring income to 2018 from 2017 when you have the ability to do so,

Unless: You’re going to have substantially more income in 2018 than 2017 that could push you up to the next tax bracket OR you’re able to deduct state income taxes this year that you won’t be able to deduct next year (see below) and those state income taxes cause more tax savings than deferring the income to a lower federal rate year.

Examples:

- avoid exercising non-qualified employee stock options in December that could be exercised in January 2018 (all else being equal)

- contribute more to your 401k in the final payroll of 2017 and less in 2018 (but not less than the match amount),

- defer some end of year revenue if possible if you’re self-employed or have a side job, or accelerate some expenses that you can take in 2017 instead of 2018 (including equipment purchases that would qualify for Sec 179 immediate expensing). This is especially important if your business would qualify for the 20% deduction on pass-thru income in future years.

- perform deductible repairs / maintenance on rental properties in 2017 that you were considering doing in 2018.

Consideration #2

Because: Federal tax rates are falling for every tax bracket in 2018,

Consider: Accelerating deductions to 2017 from 2018 when you have the ability to do so since they will have a larger impact in reducing your taxes in 2017,

Unless: You’re going to have substantially more income in 2018 than 2017 that could push you up to the next tax bracket OR those deductions wouldn’t provide as much (or any) benefit in 2017 as they would in a future year due to the Alternative Minimum Tax (AMT) in 2017, or because you can’t itemize in 2017.

Examples (but see below for limitations):

- Pay any state income tax that you might owe for 2017 via an estimated tax payment before the end of 2017. Note: this won’t work if you’re already “in AMT” for 2017 and you have to reasonably believe that you owe what you pay (can’t just pay an extra amount in 2017 to deduct it Federally and then receive a big state refund in 2018 and take it as income Federally at a lower tax rate).

- Pay your Jan 1st mortgage payment prior to the end of December 2017 (your mortgage lender should report the interest for that payment on your 2017 1098), though most people do this already.

- Pay outstanding property tax bills that aren’t due until some time in 2018 before the end of 2017 (this is only relevant in certain jurisdictions that bill in one year but set the bill’s due date in the following year). Note: this won’t work if you’re already “in AMT” for 2017 and you generally can’t prepay future year property tax bills that haven’t been generated yet.

- Make additional charitable contributions in 2017 that you would have otherwise made in a future year or consider starting a Donor Advised Fund which allows you to make a lump charitable contribution into a fund, take the full deduction this year, and then distribute to charity in future years as you see fit.

- Take any Miscellaneous Itemized Deductions in 2017 that you would have otherwise taken in a future year (see link for list). Note: this won’t work if you’re already “in AMT” for 2017.

Comment: How do you know that you’re “in AMT” for 2017? If your income and deductions are similar in 2017 than they were in 2016, you can use your 2016 taxes as a guide. Check line 45 of your 2016 Form 1040. If there is a number on it, you’re “in AMT” and assuming the same situation in 2017, you will not benefit from those items above marked as not working if you’re in AMT. If there’s no number on line 45 it means you likely wouldn’t be in AMT if you didn’t pay additional state income / property taxes or those items that would be considered Misc. Itemized Deductions. But, if you do make those extra payments, it could push you into AMT. To determine how much room you have until you hit AMT, check with your tax preparer who should be able to go back to your 2016 return and slowly increase your deductions that aren’t deductible for AMT until you hit AMT. That will give you an approximate limit to the extra payments you can make in 2017 before hitting AMT. If your 2017 situation is different from 2016, then the only way to know how much room you have for additional payments in 2017 is to prepare a mock tax return for 2017 which is not an easy task as it means gathering all the information that would be on your tax documents (W-2, 1099s, 1098s, etc.) without actually getting your tax documents in the mail.

Consideration #3

Because: The standard deduction is increasing substantially starting in 2018, fewer and fewer people will be able to itemize, meaning that their deductions won’t provide any benefit above the standard deduction. To estimate whether you’ll be able to itemize or not in 2018, add up the following for 2018 (use your 2016 Schedule A as a guide if your situation is going to be the same: 1) state/local taxes = the sum of Line 5 + Line 6 of your Schedule A, but only $10k as a max, 2) mortgage interest = Line 15 of your Schedule A (but back out any mortgage interest that’s associated with a HELOC, 3) charitable contributions = Line 19 of your Schedule A. If you are single and the above adds up to less than $12k or if you’re married filing jointly and it adds up to less than $24k,

Consider: Accelerating deductions to 2017 from any future year.

Unless: those deductions wouldn’t provide any benefit in 2017 due to the Alternative Minimum Tax (AMT) in 2017, or because you can’t itemize in 2017.

Examples: Same as Consideration #2

Comment: Same as Consideration #2.

Consideration #4

Because: The deduction for state/local taxes paid is going to be limited to $10k per year (both Single and Married Filing Jointly!), which includes state/local income taxes, sales taxes, and property taxes,

Consider: Accelerating deductions to 2017 from 2018 for state/local income/sales taxes or property taxes,

Unless: those deductions wouldn’t provide any benefit in 2017 due to the Alternative Minimum Tax (AMT) in 2017, or because you can’t itemize in 2017. Note that if the total of your state/local tax deductions in future years will be less than $10k, the only benefit here is that which is described by #2 above.

Examples (note that none of these work in AMT):

- Pay any state income tax that you might owe for 2017 via an estimated tax payment before the end of 2017. Note that the tax bill specifically outlaws pre-paying 2018 state income taxes. They would not be deductible in 2017 and would instead be treated as paid in calendar 2018 so that the system can’t be gamed.

- Pay outstanding property tax bills that aren’t due until some time in 2018 before the end of 2017 (this is only relevant in certain jurisdictions that bill in one year but set the bill’s due date in the following year). You can only do this if the bill has already been generated. Also, for those who pay their property taxes through an escrow account, you can still make a payment out-of-pocket. Your escrow company will eventually make the same payment and it should be refunded back to the escrow account or back to you at that time. If it goes back to the escrow account, your next escrow reconciliation will pick up the overpayment and refund it back to you.

- If you live in a state with no income tax and you instead deduct sales taxes, and you’re planning to buy a big ticket item (car, truck, boat) soon, do it before the end of 2017 so you get the additional sales tax deduction in 2017.

Individual Income Tax Provisions of the TCJA – now updated w/ details of the final bill

The Conference Committee has now released their Conference Report which resolves the differences between the bills passed by the House and the Senate. In a previous post, I noted those differences. In this post, I’ll note the corresponding provisions in the conference report. This final bill will need to be passed on both chambers and then signed by the president to become law. Prediction markets currently give a ~90% chance of this happening prior to the end of 2017, a ~5% chance of it passing in the first half of 2018, and a ~5% chance of it not passing at all. So this is pretty close to a done deal.

- Income Tax Rates – lower rates for all, temporarily through 2025, but different from both the House and Senate plans. See comparison of today’s rates vs. the rates in the final bill below, courtesy of The Tax Foundation. All rates revert to 2017 law (indexed for inflation) after 2025 unless extended by another Congress.

- Kiddie Tax – follows the Senate proposal, such that a child’s investment income is taxed with trust and estates rates (higher), vs. being taxed at the parent rate after a threshold. Reverts to existing law after 2025.

- Tax Rates for Dividends and Long-Term Capital Gains – remain as they are today. 0% applies if income puts you in the old 0%, 10%, or 15% tax bracket, 15% applies if in the prior 25%, 33%, or 35% bracket, and 20% applies if in the old 39.6% bracket.

- Capital Gain / Loss Tax-Lot Accounting – the provision to force First In First Out (FIFO) treatment on sales was eliminated. Current rules which allow LIFO, specific, ID, or FIFO remain in effect.

- Alternative Minimum Tax (AMT) – follows the Senate proposal. AMT is not repealed, but the exemptions amounts are increased and the phaseout income at which the exemption begins to be reduced is also increased. When combined with the SALT limitations and the elimination of miscellaneous itemized deductions subject to the 2% of AGI floor (see below), AMT shouldn’t impact nearly as many taxpayers as it previously did. Reverts to existing law after 2025.

- Standard Deduction – increased to $12k single, $24k MFJ. This increase, when combined with the SALT limitations and the elimination of miscellaneous itemized deductions subject to the 2% of AGI floor (see below) means fewer taxpayers will itemize their deductions. Reverts to existing law after 2025.

- Child Tax Credit – credit is increased to $2k per child ($500 for other dependents like parents), and begins to phase out at $200k single, $400k MFJ. Reverts to existing law after 2025.

- Adoption Credit / Credit for Plug-In Vehicles / Hope Scholarship Credit / Lifelong Learning Credit – no change to any of these. Existing law remains in effect.

- Itemized Deductions Limited – Keep in mind though that with the higher standard deductions, fewer people will need to itemize so loss of some of the below isn’t as bad as it seems. All of these revert back to existing law after 2025. These include:

- State and Local Taxes (SALT) and / or Property Taxes will only be deductible up to a combined max of $10k. Note that this is the same for Single and MFJ, thereby imposing a marriage penalty via this deduction. Additionally a provision was added to disallow a 2017 deduction on 2018 state/local income taxes that are prepaid so that taxpayers can’t game the system by prepaying future year’s worth of state taxes in 2017.

- Mortgage interest deduction would only be allowed on up to $750k of new mortgage debt (vs. $1M today), and there would be no more $100k of HELOC debt interest deduction allowed. Existing mortgages (closing prior to 12/15/2017 or with a binding contract prior to that date) would be grandfathered in the old rules.

- Casualty loss deduction eliminated (unless specifically authorized by special disaster relief).

- Medical expense deduction remains, with the AGI threshold reduced from 10% to 7.5% for 2017 and 2018 only (reverts to 10% thereafter).

- Misc. Itemized Deductions that are subject to the 2% of AGI floor (see IRS Publication 529 for a list of these deductions) are all eliminated.

- Other deductions / exclusions:

- Moving expenses deduction eliminated. Reverts after 2025.

- Alimony deduction eliminated and alimony would no longer be taxable to the receiver. Effective starting 2019 and does not revert after 2025.

- Student loan interest deduction is NOT eliminated. Existing rules are retained.

- Tuition and fees deduction is NOT eliminated. Existing rules are retained.

- Sec 121 exclusion of gain on the sale of a principal residence is NOT changed. The 2 of 5 year rule remains in effect with no income caps.

- Retirement Accounts – generally unchanged except that 401k plan loan repayments get a little easier in the case of a termination. Rather than needing to repay the loan within 90 days of termination or treating the loan as a distribution, borrowers would have the ability to repay the loan to a new retirement plan or IRA by the due date of that year’s tax return (including extensions).

- 529 College Savings Plans enhanced to allow up to $10,000/year of tax-free distributions for private /

homeschoolK-12 expenses. Edit 12/19/17 – after Senate amendments to conform to Reconciliation rules, the “homeschool” portion of this provision was dropped. 529 withdrawals cannot be used for homeschool expenses.

- Estate Tax – is not repealed, but the exemption would be doubled (~$11M per person / $22M per couple).

- ACA Individual Mandate – repeals the “Individual Mandate” (the provision that requires everyone to have health insurance, or pay a penalty on their taxes), by reducing the penalty for not having insurance to $0.

- Employer Benefit Changes – No change to dependent care FSAs, adoption benefits, tuition reimbursement plans, reduced / free tuition for employees of educational institutions, pre-tax transportation plans (parking / commuting). free gym memberships. Tax-free moving expenses reimbursements would no longer be allowed though. There would also no longer be deductions to the employer for (1) an activity generally considered to be entertainment, amusement or recreation, (2) membership dues with respect to any club organized for business, pleasure, recreation or other social purposes, or (3) a facility or portion thereof used in connection with any of the above items.

Over the next few days, I’ll post my thoughts on what, if anything, we can do before the end of 2017 to take advantage of (or limit the disadvantages of) the new tax laws going into effect. Stay tuned!

Individual Income Tax Provisions of the TCJA – now updated w/ passed versions of House & Senate bills

- Income tax rates fall for everyone. The current 7 tax brackets would be compressed into 5: 0%, 12%, 25%, 35% and 39.6% (the 0% rate applies due to deductions and exemptions which subtract from income causing the first $x of income to be subject to no tax).. For singles, the 12% rate would run to $45,000, the 25% rate would top out at $200,000, the 35% one would end at $500,000, and the 39.6% rate would kick in for taxable incomes that exceed $500,000. For marrieds, 12% rate up to $90,000, 25% would max out at $260,000, 35% would end at $1 million, and the 39.6% rate would apply above $1 million. The 12% on the first $45k or 90k of income wouldn’t apply for those in the top tax bracket. Note that this schema reduces the marriage penalty that exists in the current tax brackets since the married brackets (with the exception of the 25% bracket) are double the single brackets.

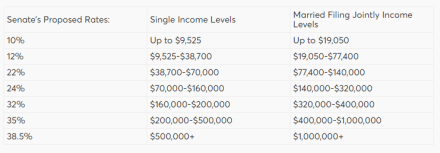

Senate Plan: 8 brackets, like today, but with different rates and caps as shown below:

All of these bracket changes would now sunset at the end of 2025 and revert back to today’s rates (inflation adjusted). Would also change the “kiddie tax” such that a child’s investment income is taxed with trust and estates rates (higher), vs. being taxed at the parent rate after a threshold.

- No change in tax rates for dividends and long-term capital gains. 0% applies if income puts you in the old 0%, 10%, or 15% tax bracket, 15% applies if in the prior 25%, 33%, or 35% bracket, and 20% applies if in the old 39.6% bracket.

Senate Plan is the same and specifically calls out that only the FIFO (first in first out) method of tax lot reporting will be allowed for the determination of gain (or average cost in the case of funds).

- AMT is completely repealed.

Senate Plan now retains the AMT, but increases the exemption amount by almost 40%, so that it will impact fewer taxpayers.

- The standard deduction is increased for everyone, but the personal exemption no longer applies. The standard deduction would be $24,400 for married filers (vs $13k now) and $12,200 for singles (vs. $6500 now). The $4150 per person personal exemption (which was phased out for upper incomers and treated differently for those in AMT) is eliminated.

Senate Plan is esentially the same, though the house plan eliminated the extra standard deduction for those age 65 and over and those who are blind while the Senate retains those additional standard deduction amounts.

- The child tax credit is increased. It would be $1600 per dependent age 16 and under (vs $1000 today). The income phaseouts are increased as well ($75k single / $115k married now to $115k single / $230k married).

Senate Plan would now increase the credit to $2,000 (up from 1650 in the original Senate plan) per dependent, raise the age to age 17 and under, and raise the income phaseouts to $500k single, $1M married. These changes would now sunset at the end of 2025.

- A new, temporary $300 tax credit for each adult taxpayer and each dependent over age 16. This applies for 5 years only and essentially offsets part of the loss of the personal exemption. It also phases out at higher incomes.

Senate Plan does not include this new temporary credit.

- Several credits go away. These include:

- Adoption Credit

- Credit for purchase of Plug-In Vehicles

- Hope Scholarship Credit & Lifetime Learning Credit, though the larger American Opportunity Credit remains.

Senate Plan retains these credits.

- Several itemized deductions go away or are reduced. Keep in mind though that with the higher standard deductions, fewer people will need to itemize so loss of some of the below isn’t as bad as it seems. These include:

- State and local tax deduction eliminated. Senate Plan is the same.

- Property tax deduction limited to $10k per year and only applies to real estate (no more auto registration deduction). Senate Plan is now the same ($10k limit)

- Mortgage interest deduction would only be allowed on up to $500k of new mortgage debt (vs. $1M today), only for primary residences (vs. first and second homes today), and there would be no more $100k of HELOC debt interest deduction allowed. Existing mortgages (closing prior to 11/2/2017 or with a binding contract prior to that date) would be grandfathered in the old rules. Senate Plan retains the $1M cap, but still eliminates the $100k of HELOC debt interest deduction.

- Casualty loss deduction eliminated (unless specifically authorized by special disaster relief). Senate Plan is the same.

- Medical expenses > 10% of AGI deduction eliminated. Senate plan retains this deduction and now reduces the AGI threshold to 7.5% for 2017 and 2018.

- Tax prep fees, and unreimbursed employee expenses (including mileage) would be eliminated. Senate plan also eliminates these deductions, but goes a step further by eliminating all Misc. Itemized Deductions that are subject to the 2% of AGI floor (see IRS Publication 529 for a list of these deductions).

- Other deductions / exclusions go away or are reduced. These include:

- Moving expenses deduction eliminated. Senate Plan is the same.

- Alimony deduction eliminated and alimony would no longer be taxable to the receiver. Senate plan does not modify alimony rules.

- The student loan interest deduction is eliminated. Senate plan retains this deduction.

- The tuition and fees deduction is eliminated. Senate plan retains this deduction.

- Sec 121 exclusion of gain on the sale of a principal residence is significantly changed. Instead of the exclusion applying regardless of income as long as the seller owned and lived in the residence for 2 of the last 5 years, the exemption would now be phased out for upper incomers (starts at $250k individual and $500k married) and the own/live requirement would be 5 of the last 8 years. Senate Plan also includes the 5 of the last 8 condition, but excludes the income caps.

- Retirement accounts are unchanged (401ks, Traditional IRAs, Roth IRAs, SEPS, SIMPLES, etc.)

Senate Plan is now the same.

- 529 College Savings Plans would be enhanced. Specifically:

- $10,000/year of tax-free distributions would be allowed from 529 college savings plans for (private) elementary and high school expenses

- 529s could be created for unborn children

Senate Plan now allows for the tax-free distributions for private K-12 education costs, but not the 529s for unborn children (which can be really be opened anyway in the parent’s name.

- The estate tax would be reduced and then eliminated. The exemption would be doubled for 2018 and eliminated completely in 2024. The gift tax system would be kept in place to prevent gaming the income tax system by shifting assets to those in lower tax brackets.

Senate Plan doubles current exemptions, but keeps the estate tax in place.

- ACA (“Obamacare”) provisions remain unchanged. The Individual Mandate (requiring health insurance or paying a penalty) remains, as do the other ACA-imposed Medicare surtaxes on wages and investment income.

Senate Plan now repeals the “Individual Mandate” (the provision that requires everyone to have health insurance, or pay a penalty on their taxes), by reducing the penalty for not having insurance to $0.

- Some employee benefits changes. These include:

- No more dependent care FSAs

- No more adoption benefits

- No more tuition reimbursement plans and no more reduced / free tuition for employees of educational institutions.

- No more moving expense reimbursements.

- No more pre-tax transportation plans (parking / commuting).

- No more free gym memberships or similar amenities without including their value in taxable income.

- 401k hardship withdrawals would still be subject to tax and penalties, but could now include employer contributions and employees would no longer be prevented from making new contributions to the plan for 6 months.

- 401k plan loan repayments get a little easier in the case of a termination. Rather than needing to repay the loan within 90 days of termination or treating the loan as a distribution, borrowers would have the ability to repay the loan to a new retirement plan or IRA by the due date of that year’s tax return (including extensions).

Senate Plan does not contain this language except for the moving expense reimbursements. Those would not be allowed in the Senate plan either. There would also no longer be deductions to the employer for (1) an activity generally considered to be entertainment, amusement or recreation, (2) membership dues with respect to any club organized for business, pleasure, recreation or other social purposes, or (3) a facility or portion thereof used in connection with any of the above items.