Reverting back to Q&A conversation format for this one…

Q: Uh oh… market update time. I guess that means the stock market is in trouble?

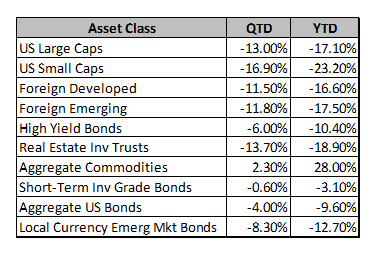

A: I wouldn’t say it’s in trouble because that gives the sense that something bad is about to happen. We don’t know what’s going to happen in the future. It sounds like semantics, but it’s an important distinction. What we do know is that stocks have performed terribly to start 2022, especially over the last 6 weeks. The Russell 2000 (small caps) and the Nasdaq are down ~30% from their highs and the S&P 500 is down 18.5%. Here’s a quick look at how the major asset classes that we track have performed quarter-to-date and year-to-date (by representative ETF):

High-growth tech has really taken it on the chin with more than 50% of the Nasdaq down more than 50% from its all-time high now. Stocks in ARK’s Innovation ETF (ARKK), perhaps the “growthiest” of growth stocks, are off even more, with the fund itself down 70%. Some other high-profile names that were booming a year or two ago make even that look not that bad (Shopify -81%, Zillow -82%, Zoom -85%, Coinbase -85%, Robinhood -88%, Peloton -93%). The market has woken up and remembered once again that price matters, and you can’t just put all your money in well-known, high-growth names at any price.

Q: That sounds awful. I know that individual stocks carry much bigger risks than the indexes, and that you don’t generally recommend individual stocks, and that PWA clients don’t own any of those names (or ARKK), so I’m not too worried about those. But, how does the decline in the S&P 500 compare to other historical declines?

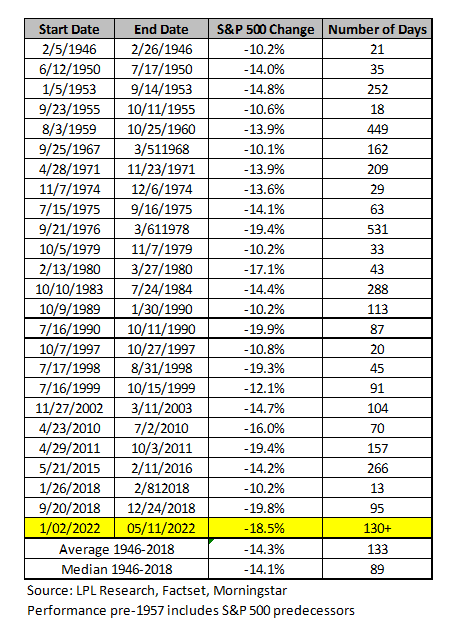

A: It’s just slightly worse than the average case. Looking at the all the times since WWII that the S&P has dropped by more than 10% from its previous high, on average, it has fallen 14.3% and it has taken 133 days from top to bottom. We’re currently down 18.5% and its been 130 days since the high. So really, this is pretty routine behavior for the S&P.

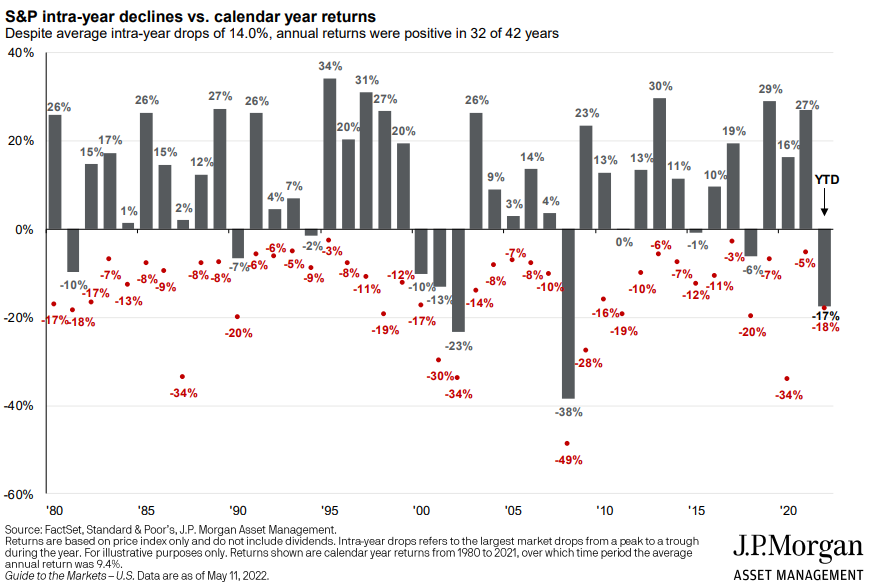

Another way of looking at this, courtesy of JP Morgan, is shown below:

You can see there are quite a few years where stocks are down significantly at some point during the year, but actually finish the year much better off. In fact, in the 23 years since 1980 that the market has been down more than 10% during the year, it finished up in 14 of them.

Q: You’ve often reminded me that there’s a nearly 100% chance that stocks are going to fall 50% from their highs, in aggregate, during my lifetime. Is this going to be one of those times?

A: While I’m very certain it’s going to happen eventually, there’s no way to know when it’s going to happen. That’s why we don’t try to time the market, moving money in an out of stocks pretending we have a crystal ball. Instead, we plan for it in client financial plans and incorporate it as a likely outcome in risk tolerance discussions. That lets us construct portfolios that can achieve client goals regardless of when (not if) the stock market temporarily declines.

Q: From the index returns table, it looks like even bonds are having a tough time. Aren’t they supposed to be the conservative, more stable part of a portfolio?

A: Bond returns can be negative from time to time. But they’re much less negative than their stock counterparts. Additionally, our client portfolios lean toward short-term bonds and incorporate inflation-protected bonds, both of which are down less than long-term or even aggregate bond funds. The long-term US treasury bond fund is down 20% so far this year. Short-term bonds are down 3.5-5.5% and short-term TIPS (treasury inflation protected securities) are actually up 0.3%. When interest rates rise, existing bond prices fall because they’re paying older/lower fixed interest rates, and are less appealing to investors. The shorter the term of the bond (or bonds in a bond fund), the less they’ll fall when interest rates rise because the bonds mature fairly quickly, investors get their principal back, and they can reinvest in new, higher interest rate bonds. With rates as low as they have been, we’ve tilted client portfolios toward short-term bonds, feeling like there’s an asymmetric chance of rising rates over falling rates. Short-term bonds are now paying nearly 3%, vs. the ~1% they were paying a year ago. The good news in rising rates is that while they temporarily depress bond prices, the interest they pay increases (quickly if the bonds are short-term), and eventually you are made whole and then some. Incorporating TIPS into portfolios also helps in times like these because TIPS pay a fixed interest rate + an inflation adjustment. When rates rise due to higher inflation, the higher inflation adjustment increases the interest payment and helps to offset the impact of the higher rate on fixed interest bonds prices. So, while this has been an ugly period for bonds, it’s within the bounds of what we expect for this type of environment and is going to lead to higher interest payments over the next couple of years a result.

Q: Understood. So what’s causing all this financial market stress?

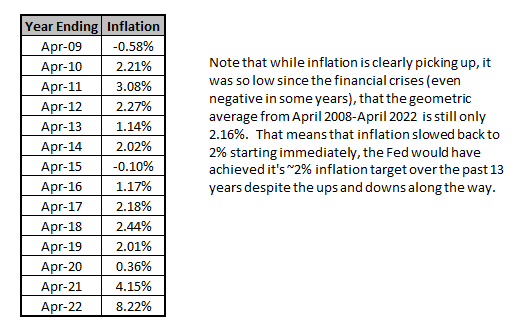

A: It’s hard to know with certainty, but I’d say a combination of fear of rising inflation and fear of slowing economic growth around the world. Inflation had been running stubbornly below the Fed’s 2% target for quite some time and has recently accelerated substantially (see table below). As world demand for goods and services came back online after covid, supply was unable to keep up. Supply chain issues led to goods shortages and rapid growth in open job positions led to employee shortages. This combined with seemingly endless money printing to support the post-financial crisis / post-covid economy and large fiscal stimulus resulted in too much money in the system chasing shortages of goods and services. People had savings and didn’t want to go back to work in a restaurant. Everyone wanted to travel at the same time. There was suddenly worldwide demand for energy at a pace that made negative oil prices of two years ago seem like a lifetime ago. It started with energy, then travel / tourism, then hospitality / dining, and now is impacting just about everything. The war in Ukraine caused another jump in energy and food prices and put more pressure on inflation. China’s latest bout with covid has also further increased supply shortages on various goods imported around the world.

As a result, the Federal Reserve and other central banks are pulling back on the liquidity they’re providing via Quantitative Easing (money printing to buy government debt and finance spending more than we’re collecting in tax revenue) and starting to raise interest rates. This month, the Fed raised interest rates by 50 basis points, taking overnight rates up to 0.75-1.00%, following a 25 basis point hike in March. They’ve signaled much more on the way.

Q: How much more?

A: Fed Funds Futures markets tell us (see derived probabilities below) that the market is currently forecasting nearly 3% rates by the of 2022 with potential of higher than that into 2023.

Q: Wow. That’s a pretty big change from what the economy is used to right?

A: Exactly. And it’s happening very fast. In anticipation of the higher overnight rates, longer-term rates have been climbing. Mortgage rates which were in the mid-3% range last year are suddenly over 5.5%. This puts pressure on housing and other activities that depend on financing. Q1 GDP came in negative (i.e. the US economy shrank in the first three months of 2022) and so the Fed is planning on substantial more tightening into a rapidly slowing economy.

Q: This is starting to sound really bad. Where’s the good news? There’s always good news isn’t there?

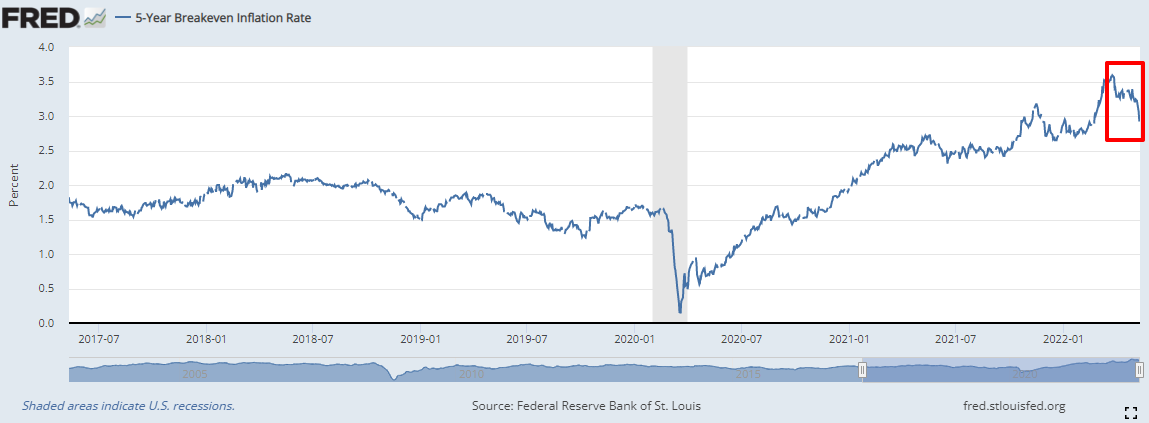

A: There is good news. Rising rates and a slowing economy should bring inflation back down. Eventually, higher prices tend to also bring more supply online (more people come into the workforce if they’ll get paid more, more oil drilling projects if the price of oil is ~$100/barrel, more crops planted if wheat/corn/etc. prices are high). The faster supply increases and demand decreases, the more dovish the Fed can be. While prices will likely remain high, it’s their year-over-year change that matters to the Fed. They don’t want a wage-price spiral to begin and take prices endlessly higher in a self-reinforcing cycle. Now, the market has already priced in massive interest rate increases. Either the economy withstands those increases and continues chugging along (means better than expected growth), or the economy puts on the brakes (means no need to take rates much higher than that, if at all). Either scenario would help stocks find a bottom and start to recover. The real danger is that the Fed raises rates too quickly in its attempt to break inflation and really hurts the economy or they don’t raise rates quickly enough and inflation accelerates from here, causing rates to ultimately have to go even higher in the future. The higher that terminal rate, where the Fed stops hiking, looks to be, the harder it temporarily is on stock and bond values. There are some signs that inflation may start to slow soon though. Using TIPS vs. non-inflation protected treasuries, we can look at what the market is pricing for future inflation. Below is a chart of the 5-year breakeven between the two, a measure of future inflation expectations. The red box shows that inflation expectations have started to decline in recent days.

Q: Ok, here’s the million dollar question… when is this all going to get better.

A: Timing is impossible and no one has a functioning crystal ball (though many in the financial industry will try to sell you one!). I wouldn’t expect an immediately turnaround. But, every time stocks have fallen in the past has turned out to be a buying opportunity in hindsight. Coincidentally, every time stocks have fallen in the past has looked like impending doom. If you’re a net saver, then the lower stocks go, the better for you as your purchases are being done cheaper than if the market never dropped. If you’re a retiree, and a net spender, then much of your portfolio isn’t in stocks and your portfolio has been stress tested to endure well beyond the current drop (if you’re a PWA client that is). I can’t reassure you as to when it will get better. I can reassure you that the timing doesn’t really matter. It will get better eventually and we’ll be in an even better place financially when it does.