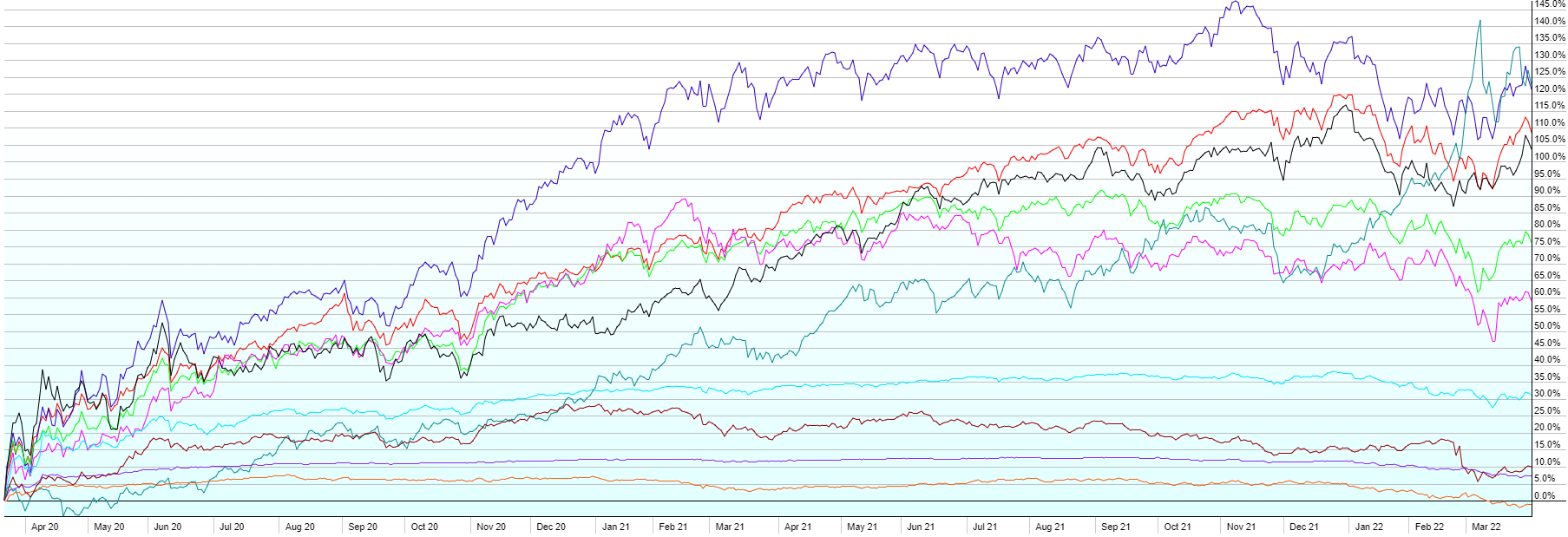

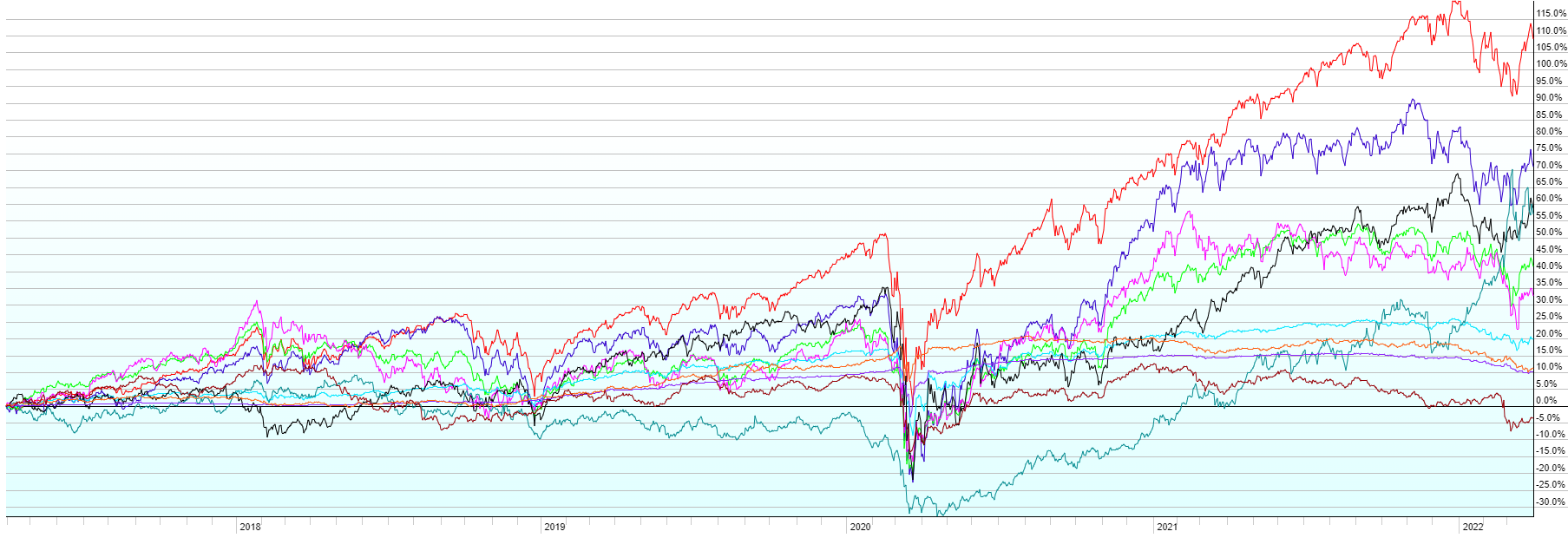

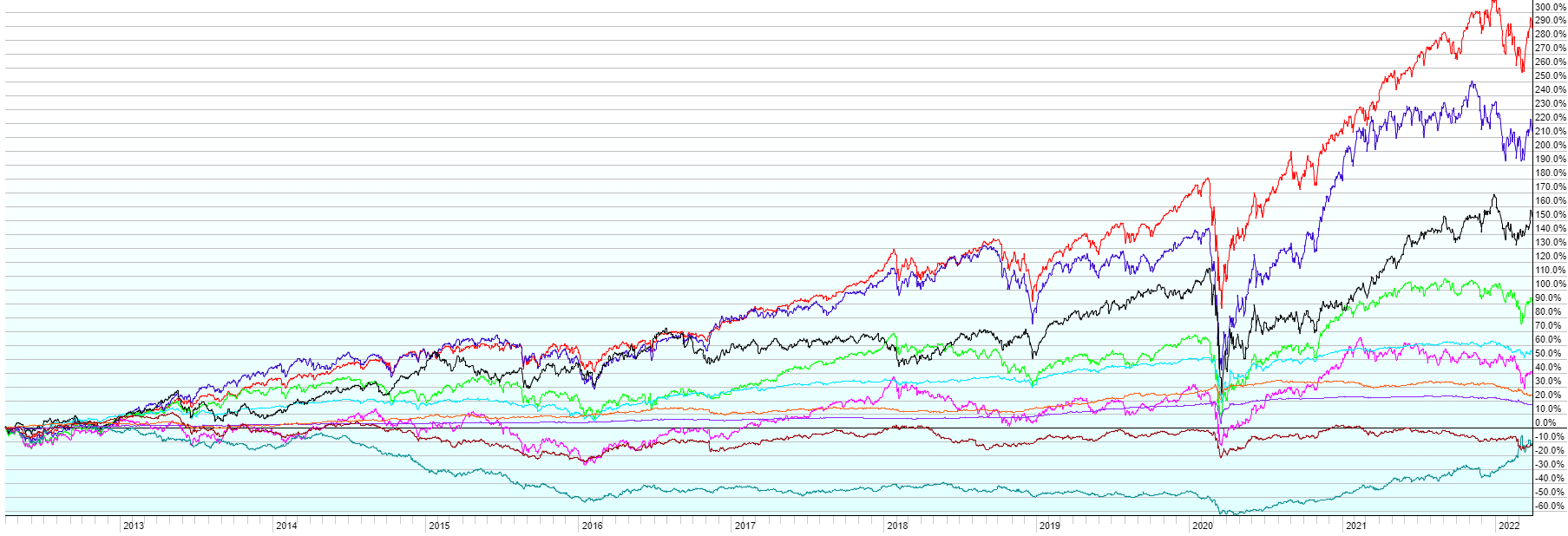

This post contains the usual returns by asset class for this past quarter (by representative ETF), last year, last five years, last ten years, and since the covid low (3/23/2020). While there is still no predictive power in this data, I’ll continue to post this quarterly for those of you that are interested.

A few notes:

- Q1 was the first down quarter for US stocks since the start of covid. All asset classes shown above except commodities, ended the quarter down between 3.8% (Short-term corporate bonds) and -6.5% (Emerging market stocks). Causes of the poor performance include the Russia/Ukraine war, spiking energy prices, high overall inflation, the Federal Reserve’s plan to raise interest rates over the next 2 years, and a re-emergence of covid in China, likely causing more supply chain disruptions. The bright side in all of that is the performance of commodities, which returned (in aggregate), over 28% for Q1. After being down and out since the financial crisis and pummeled again by covid, commodities have come roaring back over the last two years the top performer over that period.

- Bonds had their worst quarter since the 1980s. Long-term treasuries (TLT, not shown above) were down 11% in the quarter as rates spiked, and prices (which are inversely correlated with rates) sank. We generally keep the bond side of client portfolios much shorter in duration, and include inflation-protected bonds, both of which faired much better. Short-term inflation protected treasuries were only down 0.4% for the quarter.

- The worst performing areas of the market in Q1 were the high-flying US growth stocks with the ARK Innovation ETF (ARKK), down almost 30% for the quarter. On the flip side, US value stocks actually had a positive 1% return for the quarter. Higher interest rates are generally viewed as a headwind for growth stocks since much of their future earnings is far off in future years. The higher interest rates are, the higher the opportunity cost of investing in distant earnings rather than current earnings (more value-oriented). Growth has outperformed value for much of the last 15 years, which is a trend that may finally be reversing.