More political posturing today as President Obama and House Speaker John Boehner both had press conferences to say pretty much exactly what they’ve said for the past two weeks. They’re saying it louder and more sternly each time, giving it full grandstanding effect. Obama won’t negotiate unless Republicans pass a Continuing Resolution and raise the Debt Ceiling, which is like asking them to leave all their chips outside of the poker game. Boehner won’t allow a clean Continuing Resolution or Debt Ceiling bill to be voted on in the House, even though they would almost certainly pass, without some negotiation on spending reductions or Obamacare concessions attached to it. In other words, they have a complete standoff.

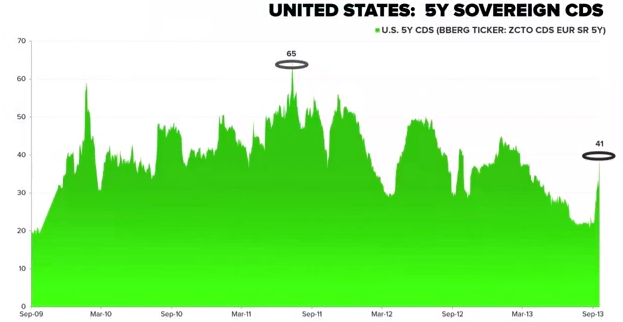

I expect more of the same for another week or so, but I don’t think the sands running out of the hourglass come with a proportional increase in the chance of a US debt default. Since there is virtually no chance that a resolution will be reached until the last minute (likely a few minutes after the last minute), the probability of non-resolution should not increase as time passes. Financial markets don’t believe there will be a debt default. Countries, companies, and individuals continue to lend money to the United States at absurdly low rates (essentially 0% for a year, 1.4% for 5 years, 2.6% for 10 years, and 3.7% for 30-years!!). The chart below shows credit default swaps (CDS) on five-year treasuries in basis points. CDS pay out in full in the event of a default. 41 basis points means that people are paying 41 cents for protection on $100 of treasuries implying a four tenths of one percent (e.g. negligible) chance of default over the next five years. While slightly elevated from a few weeks ago, 41 basis points is actually about the average over the last four years, and still substantially lower than the 65 basis points during the 2011 debt ceiling “crisis”. Today, even after the grandstanding, those same CDS actually traded down to 37 basis points.

I’m not worried about a default, just like financial markets aren’t worried about it. I’m not worried about 11:59pm on October 17th either, because that is not the exact moment that a debt default would happen if the Debt Ceiling isn’t raised (ironically, the govt. shutdown has slowed spending for the last week, so there should be a bit more wiggle room). I’m confident the debt ceiling will be raised just before it needs to be raised. I really only worry about self-fulfilling feedback loops that occur in a negative direction (like the death spiral that occurs when businesses layoff workers in mass which results in less spending in aggregate in the economy which results in lower profits which results in more layoffs). I don’t worry about those things that provide a self-regulating effect. In this case, any increase in the probability of default would lead to an increase in the probability of politicians being held directly responsible for another deep recession, which leads to the sudden ability to be rational, compromise, and save their future jobs.

The stock market will continue to be jittery as program trading, momentum trading, and day trading dominate day-to-day volume and direction of movement. I have full faith that there will be no default and no permanent damage to the economy. When that becomes certain, the economy in aggregate, the actions of the Federal Reserve, and the profitability of individual companies will once again dominate the way the market is valued. I’m not making any changes to client portfolios or asset allocation models in general as result of the debt ceiling / continuing resolution “crisis”. As the old proverb states, this too shall pass.