The budget deal that was agreed upon in Congress and signed by the President early this morning includes “Tax Extenders”, which extend some previously expired tax provisions retroactively to 2017. These include the exclusion from gross income of discharge of qualified principal residence indebtedness, the ability to deduct mortgage insurance premiums, the deduction for college tuition and fees, and the credit for residential energy improvements (windows, etc.). See this summary (https://email.steptoecommunications.com/22/1412/uploads/summary-of-tax-extenders-agreement.pdf) for a full list. Make sure to consider these items when gathering inputs for your 2017 taxes.

Month: February 2018

Market Update (2/5/2018)

I had hesitated to send one of these out after the two-day pullback in the market because while it looks bad on a point basis (Dow, S&P, etc.), it’s far from exceptional on a % basis, which is what counts. After today’s fall, the S&P is down a little over 1% for the year. Some other assets classes are down a bit more, others are still up on the year. This is far from “Markets in Turmoil”, but that business news headline attracts attention, raises fears, and up go ratings. Because of that, I thought a quick note was warranted to both show there is not turmoil at this point and to give you my perspective on what’s going on. Here’s a quick look at year-to-date performance (including any dividends paid) by asset class (representative ETF) AFTER today’s “plunge”:

US Large Cap (SPY): -1.1%

US Small Cap (VB): -2.7%

Foreign Developed (VEA): -1.5%

Foreign Emerging (VWO): +1.7%

Real Estate Investment Trusts (VNQ): -9.9%

High-Yield Bonds (HYG): -1.3%

Aggregate Bonds (BND): -1.4%

Short-Term Investment Grade Credit Bonds: CSJ: -0.1%

Local Currency Emerging Market Bonds: +2.5%

Aggregate Commodities: +0.5%.

As you can see, with the exception of REITs, which are getting beaten up as interest rates rise, this is far from turmoil.

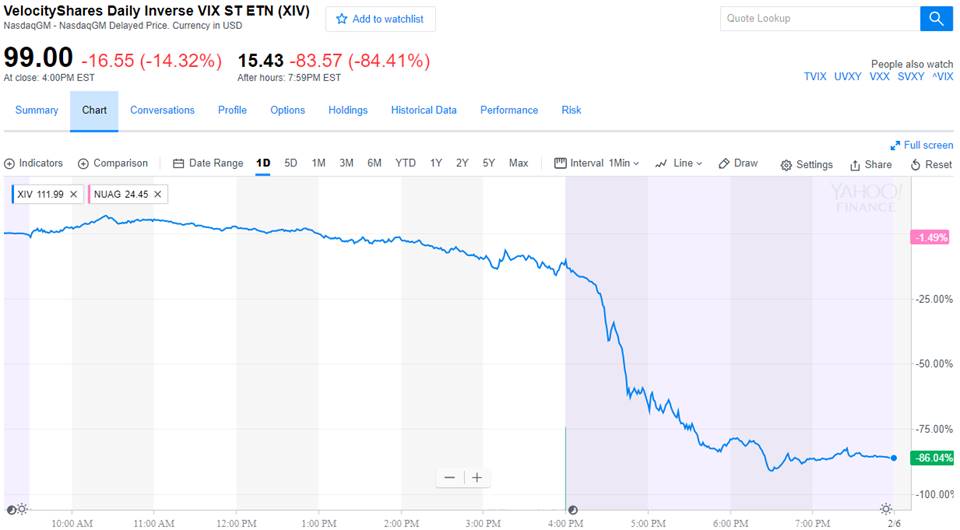

What happened today is concerning though. Stock markets behaved erratically. Futures liquidity dried up as this started to happen and liquidity in the S&P 500 futures contracts after-hours tonight are as low as they have been in a long time. That means it’s fairly easy to push the market around with relatively small orders, causing big moves in either direction. As a result, S&P futures have been moving 10+ points repeatedly over only a few minutes throughout the evening (this is the equivalent of the Dow moving in about 100 points per few minutes). The markets are down sharply overnight, with recent lows having Dow futures down another 1100 points from today’s close and S&P futures down a little over 100 points. This isn’t being caused by economic issues, bank liquidity issues, terrorism, recession, or anything that caused the last two major (-50%+) market falls. In my opinion, it’s being caused by large, leveraged bets on continuing low volatility which are unraveling in what should have been some mild profit-taking and re-pricing as interest rates moved a bit higher in January. Volatility has been running well below normal as I’ve pointed out in recent quarterly updates. Futures markets generally price in a return to normal volatility over time. Therefore, if one shorts future volatility in futures markets (or via multiple exotic ETFs and other financial products) and volatility remains low, money can be made over and over again very quickly. Hedge funds have been started that engage in this tactic and it has paid off massively over the past year as there has been virtually no volatility in the stock market. The longer the strategy pays off, the more money moves into it, chasing its success. People / funds begin to borrow money to invest in the strategy (leverage) because they can pay a few % of interest per year for their borrowing costs and make 10%+ per month if the strategy continues to do well. For all of history this has been a recipe for disaster and sure enough, it is beginning to unravel. An otherwise ordinary increase in volatility surrounding a few days of rising interest rates / declining stocks causes these bets on low future volatility to lose massive amounts of money very quickly. Fear that they won’t be able to pay back their loans causes margin calls which forces more selling of this strategy. Selling of short volatility funds is essentially buying volatility into a spike in volatility, which causes (of course) more volatility. Other hedge funds know this is happening and try to take advantage of the forced volatility buying (stock selling) causing even more. From there, it’s the same old vicious cycle that has fueled market drops like this in the past. Want proof that this is what’s going on? Today was the single biggest % increase in the VIX (the volatility index) in the history of the market on what wasn’t even in the top 100 down days on a % basis in the history of stocks. Want more proof? Here’s the after-hours chart of an exchanged traded note that tracks the inverse of the volatility index (I know that’s a mouth-full… it’s basically one of these short-future-volatility funds that is blowing up):

You’re reading that right… -86.04%, just since 4pm today! This is going to cause some hedge fund meltdowns. It’s going to cause some margin calls. It’s going to strain markets for a while. But I find it hard to believe an obscure greed-based strategy is going to bring down earnings growth, which is really starting to pick up around the world. That’s not to say there aren’t other factors playing a role here, but I think this short-volatility blow up is a big part of it. Another cue that this is probably a shorter-term event is that it’s not flowing through to currency markets at all (at least not yet). Despite futures being down 4% overnight, the dollar index, a normal flight to quality when there is a lot of fear in the market, is up only 0.1%.

Anything is possible, and as I’ve said many times, I’m certain that the stock market will eventually fall more than 50% again. We probably won’t see it coming in advance of that happening. But, if someone forced me to place a bet, I would bet that this will be a fairly short-term event that will allow the market to build again from whatever bottom that forms. To be clear, I’m not advising anyone to invest money they wouldn’t otherwise invest as a result of this. I’m not advising anyone to be more aggressive or conservative in their portfolio or to reposition assets in any way (other than usual rebalancing) as a result of this. Financial plans are designed to weather market moves, not predict them, and not time them. I know seeing your portfolio value fall hurts. For some of you, it makes you want to sell stocks. For others, it makes you want to aggressively buy stocks. But it is going to happen over and over again and is the price you pay for the kind of growth you’ve experienced over the past several years. Markets can’t only go up, despite what they’ve done in the past year. We’ll be rebalancing client portfolios on the way down (sell bonds, buy stocks), just as we rebalanced in the other direction (sell stocks, buy bonds) on the way up. And, it never hurts to have your planned contributions and 401k deposits go in at a lower level than they otherwise would have.

In short, expect that wild swings in either direction are possible over the next several days. I hope that with the explanation above, you’ll find what happens more interesting than traumatic. As always, if you’re reading this as a PWA client, feel free to contact me with any questions.

2018 Federal Withholding

In January, the IRS released new withholding tables for employers to begin using by the end of Feb 28. These new tables will take into account the new tax rates under the Tax Cuts & Jobs Act (“TCJA”) and will reduce the amount of tax withheld from your paycheck in most circumstances. However, your W-4 on file with your employer determines how many allowances are used as part of the withholding calculation and how much additional tax you elected to have withheld. Those allowances reflect a combination of your expected deductions that exceed the standard deduction (if you itemize), the number of members of your family (exemptions), the impact of multiple earners filing jointly (marriage penalty), and the impact of certain credits based on your total expected income and family size. Because the rules for many of those items have changed under the TCJA, it is very possible that the number of allowances that you are claiming is no longer correct, meaning that the withholding calculations will not be accurate.

The IRS is revising the W-4 form and their online withholding calculators to reflect the changes, but they’re not expected to complete that task for at least a few more weeks. Until then, once your employer starts using the new withholding tables, you should be aware that too little (or in some cases) too much tax will be withheld. This will accrue a refund or an amount owed in April 2019 when you file for 2018, which may result in a higher or lower refund or amount owed than you are used to seeing. Assuming the new W-4 is released by the time your 2017 taxes being prepared, you should work through the new withholding settings and file a new W-4 with your employer at that time. A month or two of inaccurate withholding will result in a smaller impact on your April 2019 tax refund / amount owed than multiple months will. I will be initiating this conversation with financial advising clients for whom I prepare taxes. If you’re preparing your taxes on your own or through another preparer, make sure to consider a W-4 revision if appropriate. Contact your financial advisor if you’re not sure what to do.