I don’t have a crystal ball and can’t tell you where the market is going, but I can tell you why I think it has fallen recently. Here are my top pain points in reverse order of concern/impact over the short-term (#6 having the biggest impact in my opinion):

1) Geopolitical Tensions / Civil Unrest – press on these has eased recently just because there seems to be worse news in other areas to take the headlines, but they’re still very present. Middle East, Russia / Ukraine, Hong Kong… all these sorts of issues threaten global economic growth through lower productivity and inefficient use of resources. Protests, sanctions, wars, fear, and loss of life around the world that seems like it will be ongoing indefinitely.

2) Central Banks – the US Federal Reserve is ending Quantitative Easing (QE), their bond buying program that essentially amounted to printing money to purchase treasury bonds (finance government debt spending) and mortgage backed securities (finance home purchases). Many worry that the end of QE and the ultimate beginning of an interest-rate hike cycle will put the brakes on a recovering US economy. So far, long-term treasury rates and mortgage rates have stayed low despite the Fed pulling back on QE as a potential economic slowdown tends to lower rates on its own. Other major economies of the world are also moving in the opposite direction, embarking on further monetary stimulus programs as the US pulls back. This forces their rates lower and acts as competition for US rates, dragging them lower as well. 10-year government bonds in Germany are paying less than 0.7% right now. US ending monetary stimulus while Europe and Japan extend stimulus tends to push the US Dollar up vs. the Euro and the Yen, making our exports less competitive which can also act to slow down the US economy. As one of very few sources of global economic recovery for the last few years, a lot is riding on continued US growth and the end of QE combined with a stronger dollar jeopardize that.

3) Europe – the majority of the continent’s economy is still a disaster and there aren’t any signs of improvements. Many suspect a QE-like program launching in Europe soon, but the legalities of such a program in a common currency with so many different jurisdictions involved make it difficult to pull off. There’s also no way of knowing how it effective it would even be given how low interest rates in the Euro zone already are. Additionally, some concerns from a few years ago are roaring back. Greece wants to end its participation in its bailout program, but doing so means it won’t be able to borrow at the low euro-zone rates, and potentially means it will need to exit the Euro completely which threatens the stability of the currency as a whole. If Greece reverts to its issues of a few years back, Portugal, Spain, and Italy (maybe even France) can’t be far behind.

4) Oil – the price of oil has been plunging in the past few weeks. While this is good for global economic growth in general (lower prices at the pump, lower heating oil this winter, lower costs for airlines, etc.), a portion of the US recovery has been led by the energy sector and our progression toward oil independence from the Middle East though domestic production and Canadian imports. It appears that OPEC is putting on a sort-of price war now with the US, keeping their production high despite falling prices because their drilling costs are lower than our more complex ways of extracting oil (oil sands, fracking, etc.). If they can push the price down for long enough, they may be able to force a reduction in US / Canadian production and maybe even put some US / Canadian companies out of business which will ultimately push prices back up with a larger share of oil production coming from the Middle East again. As energy prices dramatically fall, hedge funds that are dedicated toward energy investments, sometimes in a leveraged way, are forced to liquidate which causes further drops in energy prices and ultimately in other assets as well. Forced selling begets forced selling and the price of everything tends to fall in a whoosh until leverage is managed, markets clear, and price stability resumes. If oil continues to fall, it’s likely the rest of the market will fall with it until oil stabilizes. The good news is that once the forced selling is done, we’ll be left with lower energy prices overall and as long as the US / Canadian producers survive, that will be a stimulus to the economy in additional discretionary money in the pockets of consumers.

5) Ebola – this is one of those very low probability of extreme catastrophe events that makes it very hard for financial markets to price risk. When markets can’t price risk, then tend to avoid it, and that means short-term traders selling just about everything other than the safest assets (treasuries). Ebola has been around for a long time and there have been other outbreaks. There will be other outbreaks after this as well, since it is carried by animals that can transmit the virus to humans, without illness by the animals. If contained, as it has been in the past, it will come and go again as any other flare up of disease (remember SARS?). If not controlled, given a 70% mortality rate with the latest outbreak, it threatens large sections of the population. The concept of confident long-term market growth is based on population growth and productivity increases over time. If a disease eliminates substantial portions of the population, that premise fails and even over the long-term, economies will shrink and equity markets will shrink with them. Even if the most likely scenario happens (a minor breakout with no epidemic-like results), fear of the disease can temporarily cause fear of being out in public, traveling, shopping, etc. Each time more negative ebola news comes out, stock markets take another leg down. With a 10-14 day incubation period, It could take several weeks to see that the breakout is controlled before some confidence is restored. As I write this, details have emerged about a 2nd healthcare worker in Dallas having ebola and having flown on a commercial jet the night before her symptoms began. Sure enough the market fell to new lows shortly after the news. The US CDC needs to instill confidence soon or ebola will take the economy down in the short-term (best case) and could take it down in the long-term if it truly does become an epidemic. Again, very low probability of extreme catastrophe, but until it’s a zero probability, it will have an impact in financial markets.

6) Fear / Self-Fulfillment – Fear of all of the above having a negative impact on the economy causes markets to fall which causes confidence to fall which causes spending to drop and layoffs to begin, which causes the economy to contract. It can be self-fulfilling and can happen very quickly. The more the stock market falls and the longer the fall drags on due to fear of a recession, the higher the potential that the recession occurs as a result. This is the biggest concern for the stock market short-term. This correction, so far, has happened quickly and hasn’t taken market levels to a point that the fall will impact the economy. That doesn’t stop the market from starting to worry about though.

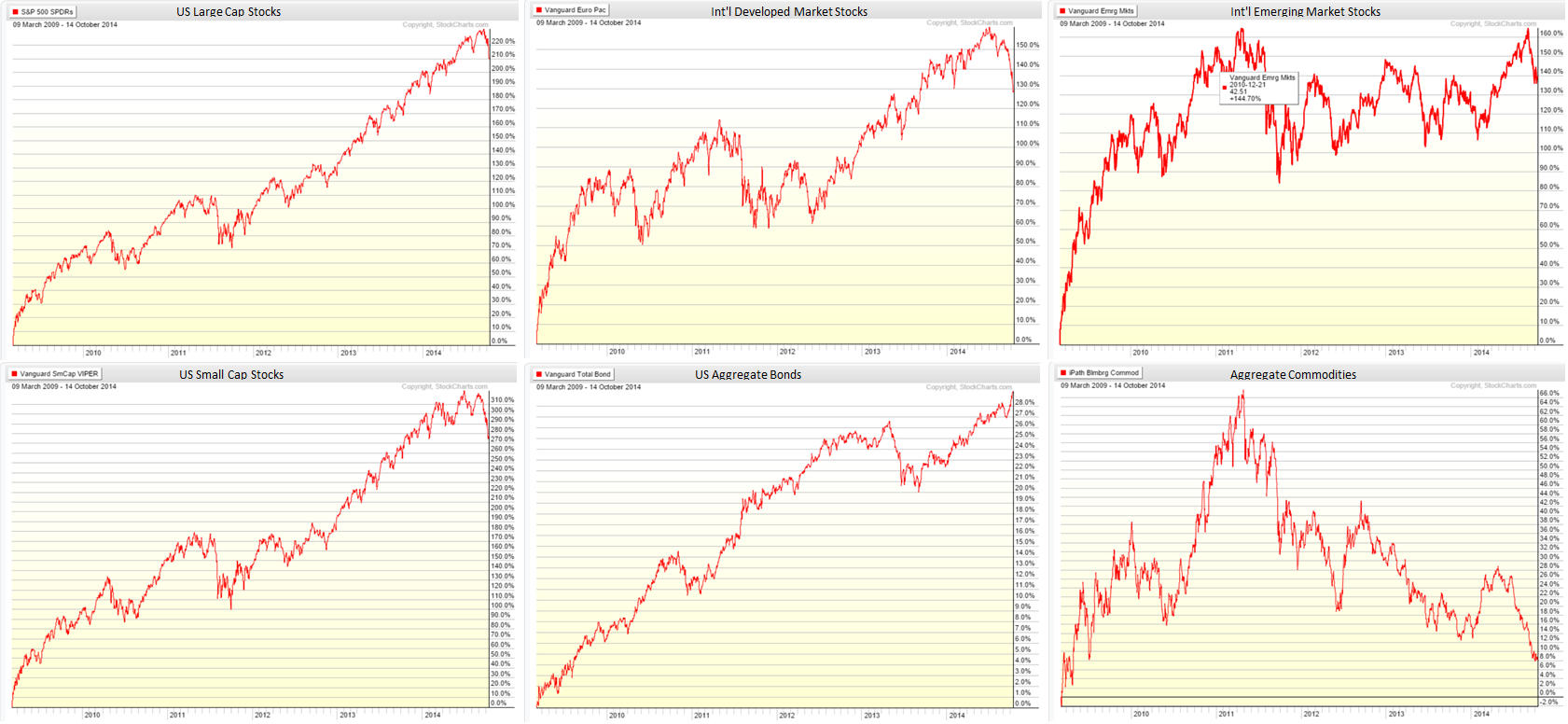

Remember, markets tend to climb the wall of worry. As long as there are reasons to worry, there’s room for the market to go up. New worries will push it down temporarily (no one was talking about ebola a year ago), but the lower prices go, the better the price you get if you’re using a consistent plan of buying over time. This is why people are so successful with 401ks. Volatility creates wealth for those who don’t fear it (see https://blog.perpetualwealthadvisors.com/2013/06/20/the-value-of-volatility/). While we can’t control the aggregate market going through a fear-cycle, I hope that understanding the reasons that cause the fear helps you avoid it.