The House Ways and Means Committee released a tax plan designed to pay for (part of?) the bi-partisan Infrastructure Bill and the larger spending bill that Democrats are trying to pass through a process known as “reconciliation”. The House tax plan contains fewer tax hikes and fewer changes to the tax code overall than President Biden’s initial plan released earlier this year. While the President’s plan always seemed unlikely to garner enough support, the House plan has the makings of a real starting point for negotiation. The Senate is moving forward with its own legislation and eventually, both Chambers will need to pass a bill, then reconcile into one bill which is re-passed. With the Democrats having slim margins in both the House and Senate (courtesy of the VP tie-breaker there), it will be difficult to get enough support from the progressive and more moderate side of the party at the same time. They’ll either need to do that or bring some Republicans on board in order to get enough votes to pass the broad package. In summary, there are bound to be a lot of changes to the details here, but we’re close enough to actual proposed legislation, that I thought it would be a good idea to lay out the key portions of the current proposal. As a side note, there is a fair shot that some/all of the changes will wind up being last minute, end-of-year, potentially retroactive to this year changes. The timing of enactment and the effective date of each change are going to determine whether or not any action can/should be taken to minimize the impact of tax hikes, or take advantage of temporary opportunities for deductions, credits, etc. December is going to be a fun month tax-wise, as it has been for the past several years. Stay tuned.

Currently Included in the House Plan:

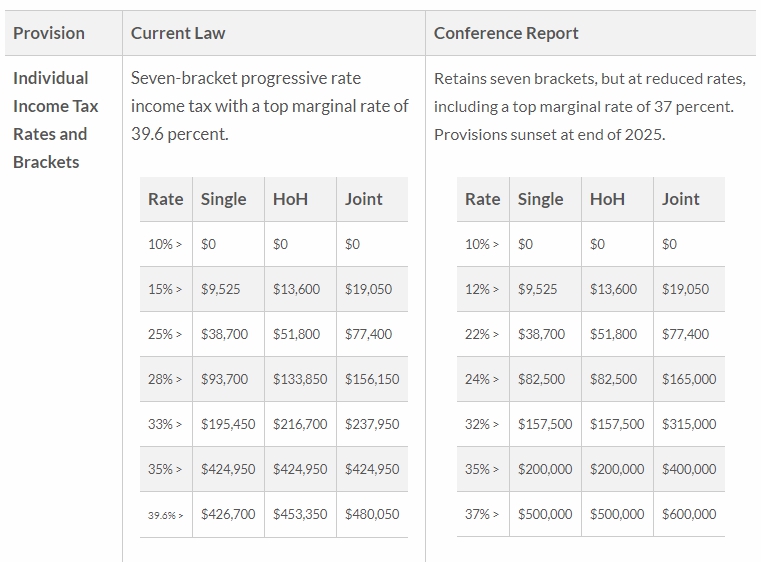

- An increase in the top marginal income tax rate from 37%, back to where it was pre-TCJA at 39.6%. In addition, the 32% and 35% brackets would be compressed so that the top bracket begins at $400K Single / $450K Joint.

- A 3% “surtax” on those earning more than $5M in a given year. A surtax is just a fancy way of adding to the income tax rate, effectively creating a new top bracket of 42.6% for those earning > $5M.

- An increase in the tax rate on long-term capital gains (LTCG) tax for upper-income taxpayers (in the top tax bracket for LTCG which starts at ~$450K single / 500K joint) from the current 20% to 25%. Note: this provision would become effective as of 9/13 if I’m reading it correctly (i.e. sales prior to that date would be taxed at the existing rate, sales on or after would be taxed at the new rate). If true, there’s no ability to sell in advance, though since the rate is only going up 5%, and that might change in a future administration, I can’t see why anyone would sell anything other than for a short-term need anyway.

- A decrease in the corporate tax rate from the current 21% to 18% for low-income (up to $400K) corporations and an increase to 26.5% for high-income (over $5M) corporations.

- Limits on the 199A “20% small business deduction” to a max of $400K Single / $500K Joint. Those aren’t income limits to take the deduction… they’re limits on the max amount of the deduction. There had been an alternate proposal (Wyden plan) to eliminate the Specified Services Trade or Business provisions as well as the W-2 income and unadjusted basis of assets provisions, and instead just institute income limits. That’s not included in the House plan. (Of course it’s not… it would have simplified something!)

- Contributions to IRAs / Roth IRAs would be prohibited if their value (in aggregate in case there are multiple accounts) exceeds $10M in value and income for the year exceeds $400k single / $450k joint.

- Add a new Required Minimum Distribution (RMD) to IRA, Roth IRA, and defined contribution (e.g. 401k) accounts (in aggregate) that exceed $10M in value if income for the year exceeds $400k single / $450k joint. The RMD would be 50% of the amount that exceeds $10M. Additionally, if the balance of those accounts exceeds $20M, a 100% distribution is required from the Roth portions until the total balance is less than $20M or the Roth accounts are exhausted.

- Roth IRA conversions and 401k Roth Conversions would be prohibited for those with income over $400k single / $450k joint. Additionally, after-tax contributions to 401k and the conversion of after-tax contributions to Traditional IRAs would be prohibited regardless of income (i.e. the end of the “backdoor Roth” and the “mega backdoor Roth”).

- IRAs would not be able to hold 1) private investments that can only be offered to “accredited investors”, 2) securities in which the owner has a >= 50% interest (10% if not tradable on an established securities market), and 3) the securities of an entity in which the IRA owner is an officer.

- Lifetime gift / estate tax exclusion is reset to its 2010 level of $5M per individual (adjusted for inflation) instead of that happening after 2025 as scheduled by TCJA.

- Changes to bring most Grantor Trusts back into the estate of the grantor and to eliminate the valuation discount frequently used when gifting portions of family limited partnerships (FLPs) to the next generation.

- More money for the IRS to boost its audit programs. Everyone hates and audit, but this is sorely needed. The IRS lacks the resources to keep up with tax cheats.

Notably Not Currently Included:

- Increase in the State And Local Tax (SALT) maximum deduction. This is the cap put in place as part of the TCJA that limits both single and joint filers to a maximum Federal deduction of $10k for taxes paid to states and localities. Several high-tax state representatives in the House have said they will not vote for any tax and spend package that doesn’t relax the current SALT limit, and House leadership has implied that a change to the SALT deduction is still on the table and may be added to the bill at a later date.

- Loss of Basis “Step-Up” at death. This feature of the current tax code allows those who inherit property (real estate, securities, farms, businesses, etc.) to have the cost basis of the property reset to its value on the date of death of the owner. This allows substantial gains to go untaxed if the property is held until death. The President’s tax plan would curb basis step up, but such curbs were not included in the recent draft from the House. The head of the Senate Finance Committee has indicated that this may wind up in the Senate bill, so it’s not dead yet either.

- Elimination of tax-free loans from securities portfolios. The current tax code allows owners of brokerage accounts to use the account as collateral to take out loans. The proceeds from the loans can then be used to support expenses, rather than selling assets and potentially paying capital gains tax on those sales. This practice helps to avoid selling assets such that basis can be stepped up at death (see bullet above) and capital gains tax is never collected.