The Conference Committee has now released their Conference Report which resolves the differences between the bills passed by the House and the Senate. In a previous post, I noted those differences. In this post, I’ll note the corresponding provisions in the conference report. This final bill will need to be passed on both chambers and then signed by the president to become law. Prediction markets currently give a ~90% chance of this happening prior to the end of 2017, a ~5% chance of it passing in the first half of 2018, and a ~5% chance of it not passing at all. So this is pretty close to a done deal.

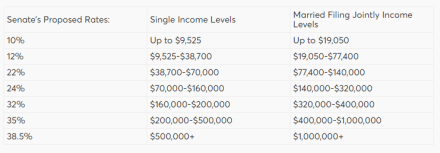

- Income Tax Rates – lower rates for all, temporarily through 2025, but different from both the House and Senate plans. See comparison of today’s rates vs. the rates in the final bill below, courtesy of The Tax Foundation. All rates revert to 2017 law (indexed for inflation) after 2025 unless extended by another Congress.

- Kiddie Tax – follows the Senate proposal, such that a child’s investment income is taxed with trust and estates rates (higher), vs. being taxed at the parent rate after a threshold. Reverts to existing law after 2025.

- Tax Rates for Dividends and Long-Term Capital Gains – remain as they are today. 0% applies if income puts you in the old 0%, 10%, or 15% tax bracket, 15% applies if in the prior 25%, 33%, or 35% bracket, and 20% applies if in the old 39.6% bracket.

- Capital Gain / Loss Tax-Lot Accounting – the provision to force First In First Out (FIFO) treatment on sales was eliminated. Current rules which allow LIFO, specific, ID, or FIFO remain in effect.

- Alternative Minimum Tax (AMT) – follows the Senate proposal. AMT is not repealed, but the exemptions amounts are increased and the phaseout income at which the exemption begins to be reduced is also increased. When combined with the SALT limitations and the elimination of miscellaneous itemized deductions subject to the 2% of AGI floor (see below), AMT shouldn’t impact nearly as many taxpayers as it previously did. Reverts to existing law after 2025.

- Standard Deduction – increased to $12k single, $24k MFJ. This increase, when combined with the SALT limitations and the elimination of miscellaneous itemized deductions subject to the 2% of AGI floor (see below) means fewer taxpayers will itemize their deductions. Reverts to existing law after 2025.

- Child Tax Credit – credit is increased to $2k per child ($500 for other dependents like parents), and begins to phase out at $200k single, $400k MFJ. Reverts to existing law after 2025.

- Adoption Credit / Credit for Plug-In Vehicles / Hope Scholarship Credit / Lifelong Learning Credit – no change to any of these. Existing law remains in effect.

- Itemized Deductions Limited – Keep in mind though that with the higher standard deductions, fewer people will need to itemize so loss of some of the below isn’t as bad as it seems. All of these revert back to existing law after 2025. These include:

- State and Local Taxes (SALT) and / or Property Taxes will only be deductible up to a combined max of $10k. Note that this is the same for Single and MFJ, thereby imposing a marriage penalty via this deduction. Additionally a provision was added to disallow a 2017 deduction on 2018 state/local income taxes that are prepaid so that taxpayers can’t game the system by prepaying future year’s worth of state taxes in 2017.

- Mortgage interest deduction would only be allowed on up to $750k of new mortgage debt (vs. $1M today), and there would be no more $100k of HELOC debt interest deduction allowed. Existing mortgages (closing prior to 12/15/2017 or with a binding contract prior to that date) would be grandfathered in the old rules.

- Casualty loss deduction eliminated (unless specifically authorized by special disaster relief).

- Medical expense deduction remains, with the AGI threshold reduced from 10% to 7.5% for 2017 and 2018 only (reverts to 10% thereafter).

- Misc. Itemized Deductions that are subject to the 2% of AGI floor (see IRS Publication 529 for a list of these deductions) are all eliminated.

- Other deductions / exclusions:

- Moving expenses deduction eliminated. Reverts after 2025.

- Alimony deduction eliminated and alimony would no longer be taxable to the receiver. Effective starting 2019 and does not revert after 2025.

- Student loan interest deduction is NOT eliminated. Existing rules are retained.

- Tuition and fees deduction is NOT eliminated. Existing rules are retained.

- Sec 121 exclusion of gain on the sale of a principal residence is NOT changed. The 2 of 5 year rule remains in effect with no income caps.

- Retirement Accounts – generally unchanged except that 401k plan loan repayments get a little easier in the case of a termination. Rather than needing to repay the loan within 90 days of termination or treating the loan as a distribution, borrowers would have the ability to repay the loan to a new retirement plan or IRA by the due date of that year’s tax return (including extensions).

- 529 College Savings Plans enhanced to allow up to $10,000/year of tax-free distributions for private /

homeschoolK-12 expenses. Edit 12/19/17 – after Senate amendments to conform to Reconciliation rules, the “homeschool” portion of this provision was dropped. 529 withdrawals cannot be used for homeschool expenses.

- Estate Tax – is not repealed, but the exemption would be doubled (~$11M per person / $22M per couple).

- ACA Individual Mandate – repeals the “Individual Mandate” (the provision that requires everyone to have health insurance, or pay a penalty on their taxes), by reducing the penalty for not having insurance to $0.

- Employer Benefit Changes – No change to dependent care FSAs, adoption benefits, tuition reimbursement plans, reduced / free tuition for employees of educational institutions, pre-tax transportation plans (parking / commuting). free gym memberships. Tax-free moving expenses reimbursements would no longer be allowed though. There would also no longer be deductions to the employer for (1) an activity generally considered to be entertainment, amusement or recreation, (2) membership dues with respect to any club organized for business, pleasure, recreation or other social purposes, or (3) a facility or portion thereof used in connection with any of the above items.

Over the next few days, I’ll post my thoughts on what, if anything, we can do before the end of 2017 to take advantage of (or limit the disadvantages of) the new tax laws going into effect. Stay tuned!