With the latest covid relief / stimulus bill now signed into law, I wanted to give the usual summary of the key financial planning / tax-related elements that may impact clients. Another round of stimulus checks has gotten most of the press to date about the $1.9 trillion legislation, but there are quite a few provisions, including those stimulus checks, in here that are worth noting:

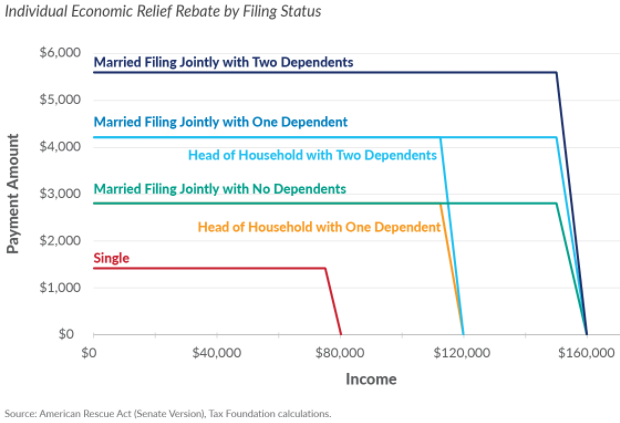

- Direct Payments (Stimulus Checks) – $1400 per eligible individual, $2800 for joint filers, and $1400 per qualifying dependent (which include full-time students under 24 and adult dependents this time). The payment begins phasing out at $75k per individual filer and $150k per joint filer, and is completely phased out at $80k individual and $160k joint, regardless of the size of the payment (different that in previous rounds of stimulus). See the graphic from the Tax Foundation below for a visual depiction of the phaseouts. The IRS will use 2020 income if available, otherwise 2019 to determine the payments. These will be reconciled on 2021 tax forms so that anyone who should have received a payment based on 2021 income and didn’t, will get a credit for the missing amount. Anyone who received a payment and shouldn’t have based on 2021 income will not have to pay it back. Payments are set to start going out the weekend of 3/13/21.

- Unemployment Benefits:

- Extension to the first week of September of the additional $300/week of Federal unemployment benefits which is added on to existing state benefits.

- New provision that exempts the first $10,200 per person of unemployment benefits from tax for 2020. Limited to those with AGI < $150k single or joint (all filers, no phaseouts). The IRS is expected to provide guidance in the coming weeks for those who already filed their 2020 returns and treated the unemployment benefits as taxable. Note that this is for 2020 only. It currently does not include 2021 benefits. The IRS has released guidance on how this should be reported for tax purposes for those who have not filed yet. Tax software will need to be updated over the next few weeks to reflect the change and make sure everything passes through to state returns correctly.

- Child Tax Credit – formerly $2k per child under age 17, now raised to $3k per child for children age 6-17 and $3600 for those under age 6. Lower income phaseouts apply to the expanded credit through (starting at $150k married, 75k single and reducing the enhancement portion of the credit by $50 for each $1k of income over the threshold). The law also instructs the IRS to pay the Child Tax Credit periodically (monthly?) for the 2nd half of 2021, meaning additional periodic checks to be received by qualifying taxpayers. Keep an eye on this. While we don’t know yet how it will be implemented, if you start receiving checks for the credit through the year and you have withholding set to take the credit into account, then you’ll need to adjust withholding or you’ll wind up owing the credit back in April. When the IRS sets this up, they’re supposed to provide a website which will allow you to opt out. Keep in mind that the IRS hasn’t even opened some mail from mid-2020 yet, so they have a bit on their plate. A good article from Kiplinger in available with more details.

- Dependent Care Credit – For 2021 only the credit will be worth up to 50% (was 35%) of eligible expenses up to $8k for one child or $16k for more than one (was $3k/$6k) with a sliding scale % based on income. It is reduced at income levels over $125k and reduced below the previous lower bound of 20% at income levels over $400k (i.e. this is a reduction in credit available at those levels vs. previous years).

- Dependent Care Flexible Spending Accounts (DCFSA) – for 2021 only, you can contribute a max of $10,500 (instead of the usual $5k) toward a DCFSA. But, your employer’s plan has to enact this change and they are not forced to do so. They’d also have to allow mid-year changes in contribution level (which was authorized under the last covid bill). Note that because of the enhancement to the Dependent Care Credit (see above), and the fact that any contributions to a DCFSA reduce the amount of expenses that qualify for the Dependent Care Credit, many taxpayers (generally AGI< mid $100,000’s) would be better off foregoing a DCFSA and using the Dependent Care Credit instead. Again, just for 2021.

- Affordable Care Act (ACA) – increases subsidies for plans purchased through the ACA exchanges. This includes the level of subsidy for a given income level and the eligibility for any subsidy for a given income level (now > 400% of the Federal poverty level). Total cost after subsidy, regardless of income cannot exceed 8.5% of income. Effective for 2021 and 2022. Also, big change, excess subsidies received for 2020 only will not need to be paid back. And, (even bigger!) if you have any unemployment benefits in 2021, you’re subsidy for 2021 only is 100% of the cost of the second highest Silver plan available to you, regardless of your actual income.

- COBRA Subsidies – covers 100% (!!!) of COBRA premiums for eligible individuals who are unemployed (lost job or reduced hours, not voluntary termination), and their families, Effective from enactment through 9/30/2021.

- Earned Income Tax Credit (EITC) – for 2021:

- raises the maximum credit for those without children to ~$1500

- makes 19-24 year old workers eligible if they are students

- makes those over age 65 eligible

- can use 2019 income to determine EITC instead of 2021.

- Student Loan Forgiveness – will not be taxable for 2021-2025 (normally debt forgiveness is taxable as income). Note that the new law does not actually forgive any student loans.

- Employee Retention Credit (ERC) – extended to 12/31/2021, adds new clauses that allow newly formed businesses post 2/15/20 to claim (which wouldn’t be able to claim the credit because they don’t have the required decline in revenue), and adds special benefits to “severely financially distressed employers” with revenue down 90%+ to the same quarter of 2019.

- Paid Leave Credits – credits for employers that provide paid leave under certain situations (which is no longer mandated). For 4/1/21 – 9/30/21, eligible wages climb to $12k per employee (from $10k), includes vaccination leave as qualified, and increases the leave for self-employed individuals to 60 days (from 50).

- Executive Compensation Limits – Businesses currently can’t deduct compensation > $1M for CEO, CFO, and the next three highest paid employees. This legislation increases that to the next eight highest paid employees starting in 2027.

- $15B for new Economic Injury Disaster Loans (EIDL) grants and clarification that EIDL grants are non-taxable and the expenses the money is used to pay are still deductible.

- $22B toward emergency rental assistance for individuals and families struggling to pay rent and utilities. Renters must meet several conditions to receive the assistance.

- $10B toward assistance for homeowners struggling to pay their mortgage, utilities and other housing costs.

- $86B toward rescuing multiple soon-to-fail-without-help union pension plans. The plans that will receive the money cover approximately 11 million people in various unionized trades.

- $25B Restaurant Revitalization Fund to be administered by the SBA. These are non-taxable grants for qualified businesses.

- $7B additional funding for Paycheck Protection Program (PPP), mostly under the same rules as before.

- $350 Billion for state and local government support, which could create more state/local level tax changes or stimulus actions.

- Various other spending allocations for K-12 schools, vaccines, testing, etc., that are beyond the scope of the financial planning discussions so I won’t dive into the details here. You can read the table of contents of the actual bill/law and dive into those areas if you’re interested. The non-tax provisions are mostly written in English rather than legalese/financialese.

Pingback: More Checks Coming From The IRS | PWA Financial Tastings Blog

Pingback: Proposed Credits & Deductions in the Upcoming Infrastructure & Broader Spending Plan | PWA Financial Tastings Blog