This one hasn’t gotten a fancy name yet (that I know of) like the CARES Act since it is attached to the 2021 Consolidated Appropriations Act (the “2021 spending bill” that funds the government), so I’m just referring to it as the Dec 2020 COVID Relief Bill. It was signed into law on 12/27/2020 and consists of ~$900B of funding, not to be confused with the $1.4T in general “keep the lights on” type funding in the rest of the Act. The full Consolidated Appropriations Act is 5,593 pages. I cannot claim to have read the whole thing. However, I’ve skimmed through it and read enough summaries now to feel comfortable calling out the top line virus-related items and the key tax and personal financial planning items for you. This list below includes the COVID Relief Bill portions, the relevant tax and financial planning-related items from the rest of the Act, and a few other callouts. Here goes:

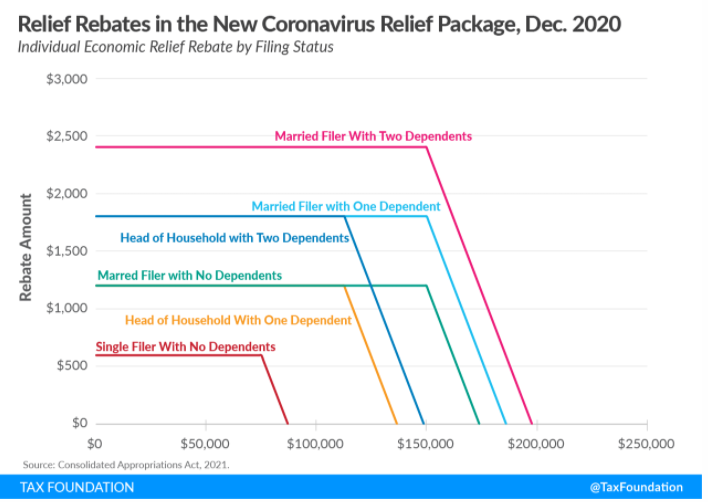

- Direct Payments (“stimulus checks”) – ~$170B for direct payments to taxpayers. $600 per individual earning $75k or less, or $1200 per couple earning $150k or less, +$600 per dependent child under age 17 (e.g. $2400 for a family of 4 earning $150k or less). Above the $75k/150k threshold, the payment amount drops by $5 for every $100 of income until it is completely phased out. Income used is the lower of 2019 or 2020. Payments will be sent out by direct deposit or check based on 2019 income, but can be trued up on the 2020 tax return if income was lower or more children were born. For more details, see this fantastic article from Forbes, and this nifty chart from the Tax Foundation

- Unemployment Benefits – $120B. extends emergency Federally funded benefits (including that for self-employed) for 11 weeks and provides a $300/week Federal amount in addition to existing state-provided benefits.

- Paycheck Protection Program (“PPP”) – $284B extends PPP v 1.0 and issues a new round of funding for PPP v2.0 Additionally, reverses the IRS interpretation that business expenses used to qualify for PPP forgiveness were not deductible. They clarified that those expenses are deductible. It also broadens the list of qualifying expenses for forgiveness to include operating expenses, supplier costs, property damage costs, and PPE expenses, still subject to the limitation that non-payroll expenses cannot exceed 40% of the forgiven loan amount. Not exactly auto-forgiveness for small loans (many were calling for this), but the Act does tell SBA to create a one-page form to apply for auto-forgiveness (*smacks my head*) for loans < $150k. Side note: Auto-forgiveness = Ease of use as the main course, but with a large side of increased fraud. I think this auto-forgiveness means that an applicant would get forgiveness even if payroll was reduced during the covered period, so long as the PPP money wasn’t used improperly and no fraud was involved. PPP v 2.0 is for businesses w/ < 300 employees (<500 if accommodation or food service) and that had at least one quarter of 2020 with revenue at least 25% lower than the same quarter in 2019. Max loan is $2M or 2.5x avg monthly payroll whichever is less, (3.5x for accommodation or food service).

- Vaccines, Testing, Health – $63 billion for vaccine distribution, testing and tracing, and other health-care initiatives, most of which will be administered by the states.

- Transportation – $45 billion for transit agencies, airlines ($15B specifically allocated for airline payroll support), airports, state departments of transportation, and rail service.

- Education & Childcare & Broadband Support – $82B in funding for colleges and schools, including support for HVAC upgrades to mitigate virus transmission + $10 billion for child care assistance + $7B for enhanced broadband access.

- Nutrition & Agriculture – $26B for food stamps, food banks, school/daycare feeding programs, and payments, purchases, and loans to farmers and ranchers impacted by covid-related losses.

- Rental Assistance – the eviction moratorium is extended through 1/31/2021 (for now). $25B is authorized to help troubled renters and landlords by paying future rent and utilities as well as back rent owed or existing utility bills.

- SBA Loan Relief – The CARES Act authorized SBA to pay up to six months of principal and interest on existing Section 7 SBA Loans for impacted borrowers. This Act extends that by another three months.

- Economic Injury Disaster Loans (EIDL) – $20B in additional funding for businesses in low-income communities + $15B of dedicated funding is set aside for live venues, independent movie theatres, and cultural institutions.

- Credit for Paid Sick + Family Leave – this was created by the Families First Act and is now extended through 3/31/2021 (was 12/31/2020).

- Employee Retention Tax Credit – created under the CARES Act, is extended through 6/30/2021 and improved. It’s now up to 70% of wages capped at $10k of wages per employee per quarter, instead of 50% capped at $10k in total. Business qualifies if revenue for the quarter was down at least 20% from the same quarter in 2019. Important: it appears this credit is now allowed along with a PPP Loan (under the CARES Act, it was one or the other), though you still can’t double count the same wages for the credit and PPP forgiveness.

- Payroll Tax Deferral – the president signed an executive order in September allowing employers to opt in to a payroll tax deferral for employees. Almost no one did (except the government) because it was too risky on the employer and deferral for a few months was pretty meaningless. Those that did were supposed to repay the deferral by 4/30/2021. That has now been extended to 12/31/2021, giving more time to spread out the payback.

- Lookback for Earned Income Tax Credit and Refundable Child Care Credit – taxpayers can, but don’t have to, use 2019 income instead of 2020 income to qualify for these in 2020.

- Residential Solar Tax Credit – this was reduced to 26% of the cost of the project in 2020, scheduled to drop to 22% in 2021, and then eliminated after 2021. The Act extends the 26% credit for 2021 and 2022, dropping to 22% for 2023. It is now eliminated in 2024, unless additional legislation is passed.

- Employer Paid Student Loans – Employers can continue to give up to $5250 per year tax-free to employees for student loan principal and interest repayment (either direct to the loan or to the employee to pay the loan). This is extended through 2025 (was set to expire at the end of 2020).

- Tuition Deduction / Lifetime Learning Credit – The tuition deduction, unless extended in other legislation, is gone. Instead, there is now a higher income threshold for the Lifetime Learning Credit, now sync’d up with the American Opportunity Credit phaseout ($80-90k single / $160-180k married).

- Student Loan Payment Forbearance – this WAS NOT extended in the Act. Student loan payments resume 1/1/2021.

- Retirement Plan Distributions / Loans – The CARES Act allowed up to $100k of distributions from retirement plans for covid-impacted individuals, waiving the 10% penalty, and allowing the amounts to be repaid over 3 years such that no net tax would be owed. It also raised the 401k loan amount to the minimum of $100k or 100% of the balance (from $50k or 50%). These were effective through 12/30/2020. This treatment is now extended to non-covid-related Federally declared disaster areas between 1/1/2020 and 2/25/2021 where the individual has their principal place of residence and is economically impacted by the disaster.

- Retirement Plan Required Minimum Distributions – these were waived by the CARES Act for 2020. This WAS NOT extended by the new Act. RMDs will be required for 2021 unless additional legislation is passed.

- Medical Expenses Deduction – the deduction for medical expenses has been bouncing back and forth between a 7.5% AGI floor and a 10% AGI floor for years. It’s 7.5% for 2020 and was supposed to revert back to 10% for 2021. The Act sets this to 7.5% PERMANENTLY. One thing I can stop writing about every year!

- Mortgage insurance premiums – remain deductible for another year through 2021.

- The taxability of forgiven housing debt (foreclosure/short-sale) – is extended to 2025, but the amount is reduced to $375k single / $750k married.

- Charitable Giving – The $300 charitable contribution deduction for those who don’t itemize is sticking around for 2021 now and joint filers will get $600 instead of $300 for 2021. Remember this is for cash donations only and donations to a Donor Advised Fund don’t count. And, the cap on the portion of your income you can give via a cash donation (other than to a Donor Advised Fund) and deduct stays at 100% for 2021.

- Healthcare & Dependent Care Flexible Spending Account (FSA) flexibility – The Act allows plans to allow 2020 unused amounts can carryover to 2021 and 2021 can carryover to 2022. Additionally, the Act allows 2021 elections to be modified even though benefits enrollment is now closed for most employees. However, this only updates what the law will allow employer plans to do. The plans themselves would have to adopt the change in order for employees to be able to use the increased flexibility. Check with your benefits rep to see if your plan is adopting / has adopted the change.

- Educator’s Deduction – this is the $250 per year that teachers get to deduct for money spent on school supplies for their classrooms (as if that’s all teacher’s spend on their classrooms). PPE and cleaning supplies now qualify for that $250.

- Business Meals – for business owners, restaurant meals are 100% deductible for 2021 and 2022 (formerly only 50% deductible) as long as they meet the requirements of the previous 50% deduction (i.e. non-lavish, taxpayer is present, etc.). Note that this still does not include employee expenses, only schedule C filers. Applies to dine-in or take-out.

- Surprise Billing Fix – an attempt to reduce the amount of “surprise billing”, which typically occurs when a patient goes to an in-network facility and uses an in-network doctor, but is provided services by an out-of-network provider along the way (e.g. anesthesiology, transportation, etc.). There are lots of carve outs and exceptions, so I’m skeptical of how much this really fixes, but it’s a start at least, going into effect in 2022. I’m sure much more will be written on the implications here soon.

- Financial Aid Changes – Student Loan Application (FAFSA) simplification – lots of changes here, but they don’t go into effect until 2023. In the interest of time, I’ll table this one for now. Just know there are changes coming. Additionally, the number of Pell Grants will be increased.

In order to reach a bipartisan agreement, both of the following WERE NOT INCLUDED in the Act:

- Business liability protection (i.e. can’t sue if you get covid at a business as long as they were following CDC guidelines), which Republicans wanted

- State and Local Aid above and beyond that specifically budgeted for the items in the Act, which Democrats wanted.

I suspect there will be more to come, though the type of relief/stimulus likely depends on the outcome of the GA Senate run-offs. There is already a proposal to increase the $600 direct payments to $2000, supported by the House and the President, but that will have a difficult time in the Senate. We’ll have to wait and see what happens.

Pingback: American Rescue Plan Act (ARPA) of 2021 | PWA Financial Tastings Blog