In the last post, I covered the potential “pay-fors” that would… well… pay for some of the spending, deductions, and credits enabled by the proposed infrastructure and broader spending legislation that Congress is working on passing via reconciliation this fall. That proposed legislation is currently 645 pages, and subject to many changes as it makes its way through committees in both chambers. There are many proposed changes to the tax code (enough to make the TCJA look simple) to go along with various spending appropriations. The majority have to do with infrastructure incentives and credits for business. But, there are a few notable ones for individuals/families. Keeping in mind that this is just a proposal, here is a non-exhaustive list of the provisions that may provide some benefit to you:

Increases the credit for adding solar to a residence back to 30% of the cost. Extended through 2031, then phases down to 26% in 2032, 22% in 2033, and then expires. Includes residential battery storage technology as well.

Extends the non-business energy property credit (energy-efficient windows, doors, furnaces, , water heaters, etc.) to 2031 and expands the credit to 30% of the cost from the current 10%. Additionally, it eliminates the (frustrating and hard to track) lifetime limit and replaces it with a $1200 annual limit.

Creates a new Plug-In Electric Vehicle Credit ranging from $4000 to $12,500 (limited to 50% of the cost), depending on battery capacity, assembly location, and what portion of the vehicle is made with domestic parts. It won’t apply to vehicles weighing more than 14,000 lbs or vehicles with an MSRP exceeding certain thresholds. The credit phases out starting at income of $400K single / $800K Joint.

Creates a new Plug-In Electric Vehicle Credit for purchase of used qualifying vehicles. Much lower income thresholds, lower credit amount, and the vehicle must be at least 2 years old.

Creates a new credit for certain electric bicycles, and reinstates the employer provided fringe benefit for bicycle commuting (with the max benefit raised to $52.50/mo from $20/mo)

Extends the enhanced Child Tax Credit ($3k per child age 6-17, $3600 per child age 5 or under), as created by the American Rescue Plan (ARPA) earlier in 2021, including monthly checks of half of the expected amount of the credit, through 2025 (previously expired in 2021). However, instead of defaulting to including the monthly checks, the default will be to not have monthly checks sent and the taxpayer will have to opt in in some manner to be determined at a later date by the Treasury/IRS. Income phaseouts continue to apply as defined in ARPA (phaseout for the original $2k is $200K Single / $400K Married, and for the enhanced $1600 it’s $75K Single / $150K Married.

Makes the Child Tax Credit permanently (until changed by future legislation) refundable. This means the credit amount can exceed the taxpayer’s total tax liability for the year and the taxpayer will still get the full credit. No longer reverts back to the pre-ARPA rules after 2025

Extends the $500 credit for “Other Dependents” through 2025.

Makes the Dependent Care Credit changes from APRA permanent. That increased the maximum qualifying expenses to $8K for one child or $16K for two or more children. The amount of the credit starts at 50% of qualifying expenses. If income exceeds $125K, the credit percentage is reduced, until it drops to 20% at $400K. It then completely phases out if income exceeds $500K. Also makes permanent the income exclusion for employer provided Dependent Care Assistance (e.g. Dependent Care Flexible Spending Accounts) at the ARPA enhanced level of $10,500 per year (up from the $5k limit pre-ARPA). Note that employers still need to adopt this change in order for employees to take advantage of it.

Creates a new credit for caregivers of 50% of qualified expenses up to a $4K maximum credit. Begins to phase-out at $75K of income. This is for people who care for those with long-term care needs in their own home.

Enhances the Earned Income Credit.

Creates a new credit for contributions to a Public University that provide infrastructure for research. The credit, available through 2032, is 40% of the amount contributed to the qualifying project (lots of rules as to what qualifies). Note: this is a credit, not a deduction, so you don’t have to itemize to take it.

With the latest covid relief / stimulus bill now signed into law, I wanted to give the usual summary of the key financial planning / tax-related elements that may impact clients. Another round of stimulus checks has gotten most of the press to date about the $1.9 trillion legislation, but there are quite a few provisions, including those stimulus checks, in here that are worth noting:

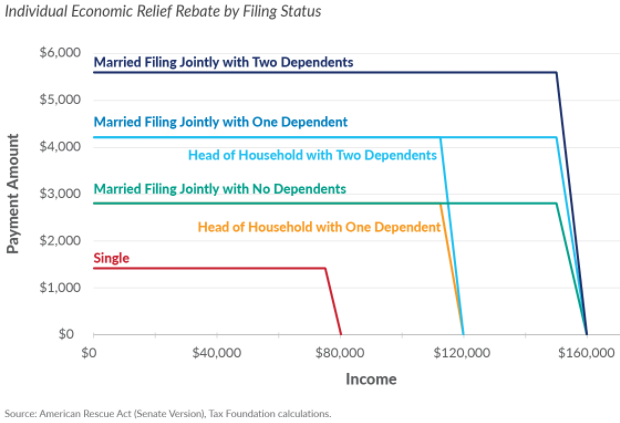

Direct Payments (Stimulus Checks) – $1400 per eligible individual, $2800 for joint filers, and $1400 per qualifying dependent (which include full-time students under 24 and adult dependents this time). The payment begins phasing out at $75k per individual filer and $150k per joint filer, and is completely phased out at $80k individual and $160k joint, regardless of the size of the payment (different that in previous rounds of stimulus). See the graphic from the Tax Foundation below for a visual depiction of the phaseouts. The IRS will use 2020 income if available, otherwise 2019 to determine the payments. These will be reconciled on 2021 tax forms so that anyone who should have received a payment based on 2021 income and didn’t, will get a credit for the missing amount. Anyone who received a payment and shouldn’t have based on 2021 income will not have to pay it back. Payments are set to start going out the weekend of 3/13/21.

Unemployment Benefits:

Extension to the first week of September of the additional $300/week of Federal unemployment benefits which is added on to existing state benefits.

New provision that exempts the first $10,200 per person of unemployment benefits from tax for 2020. Limited to those with AGI < $150k single or joint (all filers, no phaseouts). The IRS is expected to provide guidance in the coming weeks for those who already filed their 2020 returns and treated the unemployment benefits as taxable. Note that this is for 2020 only. It currently does not include 2021 benefits. The IRS has released guidance on how this should be reported for tax purposes for those who have not filed yet. Tax software will need to be updated over the next few weeks to reflect the change and make sure everything passes through to state returns correctly.

Child Tax Credit – formerly $2k per child under age 17, now raised to $3k per child for children age 6-17 and $3600 for those under age 6. Lower income phaseouts apply to the expanded credit through (starting at $150k married, 75k single and reducing the enhancement portion of the credit by $50 for each $1k of income over the threshold). The law also instructs the IRS to pay the Child Tax Credit periodically (monthly?) for the 2nd half of 2021, meaning additional periodic checks to be received by qualifying taxpayers. Keep an eye on this. While we don’t know yet how it will be implemented, if you start receiving checks for the credit through the year and you have withholding set to take the credit into account, then you’ll need to adjust withholding or you’ll wind up owing the credit back in April. When the IRS sets this up, they’re supposed to provide a website which will allow you to opt out. Keep in mind that the IRS hasn’t even opened some mail from mid-2020 yet, so they have a bit on their plate. A good article from Kiplinger in available with more details.

Dependent Care Credit – For 2021 only the credit will be worth up to 50% (was 35%) of eligible expenses up to $8k for one child or $16k for more than one (was $3k/$6k) with a sliding scale % based on income. It is reduced at income levels over $125k and reduced below the previous lower bound of 20% at income levels over $400k (i.e. this is a reduction in credit available at those levels vs. previous years).

Dependent Care Flexible Spending Accounts (DCFSA) – for 2021 only, you can contribute a max of $10,500 (instead of the usual $5k) toward a DCFSA. But, your employer’s plan has to enact this change and they are not forced to do so. They’d also have to allow mid-year changes in contribution level (which was authorized under the last covid bill). Note that because of the enhancement to the Dependent Care Credit (see above), and the fact that any contributions to a DCFSA reduce the amount of expenses that qualify for the Dependent Care Credit, many taxpayers (generally AGI< mid $100,000’s) would be better off foregoing a DCFSA and using the Dependent Care Credit instead. Again, just for 2021.

Affordable Care Act (ACA) – increases subsidies for plans purchased through the ACA exchanges. This includes the level of subsidy for a given income level and the eligibility for any subsidy for a given income level (now > 400% of the Federal poverty level). Total cost after subsidy, regardless of income cannot exceed 8.5% of income. Effective for 2021 and 2022. Also, big change, excess subsidies received for 2020 only will not need to be paid back. And, (even bigger!) if you have any unemployment benefits in 2021, you’re subsidy for 2021 only is 100% of the cost of the second highest Silver plan available to you, regardless of your actual income.

COBRA Subsidies – covers 100% (!!!) of COBRA premiums for eligible individuals who are unemployed (lost job or reduced hours, not voluntary termination), and their families, Effective from enactment through 9/30/2021.

Earned Income Tax Credit (EITC) – for 2021:

raises the maximum credit for those without children to ~$1500

makes 19-24 year old workers eligible if they are students

makes those over age 65 eligible

can use 2019 income to determine EITC instead of 2021.

Student Loan Forgiveness – will not be taxable for 2021-2025 (normally debt forgiveness is taxable as income). Note that the new law does not actually forgive any student loans.

Employee Retention Credit (ERC) – extended to 12/31/2021, adds new clauses that allow newly formed businesses post 2/15/20 to claim (which wouldn’t be able to claim the credit because they don’t have the required decline in revenue), and adds special benefits to “severely financially distressed employers” with revenue down 90%+ to the same quarter of 2019.

Paid Leave Credits – credits for employers that provide paid leave under certain situations (which is no longer mandated). For 4/1/21 – 9/30/21, eligible wages climb to $12k per employee (from $10k), includes vaccination leave as qualified, and increases the leave for self-employed individuals to 60 days (from 50).

Executive Compensation Limits – Businesses currently can’t deduct compensation > $1M for CEO, CFO, and the next three highest paid employees. This legislation increases that to the next eight highest paid employees starting in 2027.

$15B for new Economic Injury Disaster Loans (EIDL) grants and clarification that EIDL grants are non-taxable and the expenses the money is used to pay are still deductible.

$22B toward emergency rental assistance for individuals and families struggling to pay rent and utilities. Renters must meet several conditions to receive the assistance.

$10B toward assistance for homeowners struggling to pay their mortgage, utilities and other housing costs.

$86B toward rescuing multiple soon-to-fail-without-help union pension plans. The plans that will receive the money cover approximately 11 million people in various unionized trades.

$25B Restaurant Revitalization Fund to be administered by the SBA. These are non-taxable grants for qualified businesses.

$7B additional funding for Paycheck Protection Program (PPP), mostly under the same rules as before.

$350 Billion for state and local government support, which could create more state/local level tax changes or stimulus actions.

Various other spending allocations for K-12 schools, vaccines, testing, etc., that are beyond the scope of the financial planning discussions so I won’t dive into the details here. You can read the table of contents of the actual bill/law and dive into those areas if you’re interested. The non-tax provisions are mostly written in English rather than legalese/financialese.

This one hasn’t gotten a fancy name yet (that I know of) like the CARES Act since it is attached to the 2021 Consolidated Appropriations Act (the “2021 spending bill” that funds the government), so I’m just referring to it as the Dec 2020 COVID Relief Bill. It was signed into law on 12/27/2020 and consists of ~$900B of funding, not to be confused with the $1.4T in general “keep the lights on” type funding in the rest of the Act. The full Consolidated Appropriations Act is 5,593 pages. I cannot claim to have read the whole thing. However, I’ve skimmed through it and read enough summaries now to feel comfortable calling out the top line virus-related items and the key tax and personal financial planning items for you. This list below includes the COVID Relief Bill portions, the relevant tax and financial planning-related items from the rest of the Act, and a few other callouts. Here goes:

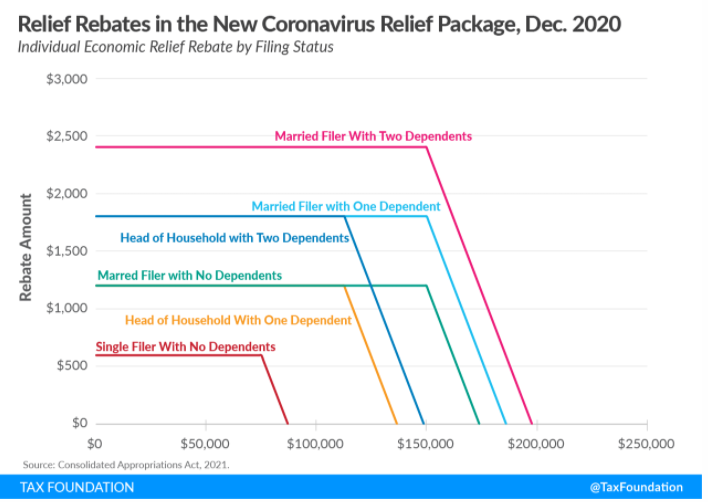

Direct Payments (“stimulus checks”) – ~$170B for direct payments to taxpayers. $600 per individual earning $75k or less, or $1200 per couple earning $150k or less, +$600 per dependent child under age 17 (e.g. $2400 for a family of 4 earning $150k or less). Above the $75k/150k threshold, the payment amount drops by $5 for every $100 of income until it is completely phased out. Income used is the lower of 2019 or 2020. Payments will be sent out by direct deposit or check based on 2019 income, but can be trued up on the 2020 tax return if income was lower or more children were born. For more details, see this fantastic article from Forbes, and this nifty chart from the Tax Foundation

Unemployment Benefits – $120B. extends emergency Federally funded benefits (including that for self-employed) for 11 weeks and provides a $300/week Federal amount in addition to existing state-provided benefits.

Paycheck Protection Program (“PPP”) – $284B extends PPP v 1.0 and issues a new round of funding for PPP v2.0 Additionally, reverses the IRS interpretation that business expenses used to qualify for PPP forgiveness were not deductible. They clarified that those expenses are deductible. It also broadens the list of qualifying expenses for forgiveness to include operating expenses, supplier costs, property damage costs, and PPE expenses, still subject to the limitation that non-payroll expenses cannot exceed 40% of the forgiven loan amount. Not exactly auto-forgiveness for small loans (many were calling for this), but the Act does tell SBA to create a one-page form to apply for auto-forgiveness (*smacks my head*) for loans < $150k. Side note: Auto-forgiveness = Ease of use as the main course, but with a large side of increased fraud. I think this auto-forgiveness means that an applicant would get forgiveness even if payroll was reduced during the covered period, so long as the PPP money wasn’t used improperly and no fraud was involved. PPP v 2.0 is for businesses w/ < 300 employees (<500 if accommodation or food service) and that had at least one quarter of 2020 with revenue at least 25% lower than the same quarter in 2019. Max loan is $2M or 2.5x avg monthly payroll whichever is less, (3.5x for accommodation or food service).

Vaccines, Testing, Health – $63 billion for vaccine distribution, testing and tracing, and other health-care initiatives, most of which will be administered by the states.

Transportation – $45 billion for transit agencies, airlines ($15B specifically allocated for airline payroll support), airports, state departments of transportation, and rail service.

Education & Childcare & Broadband Support – $82B in funding for colleges and schools, including support for HVAC upgrades to mitigate virus transmission + $10 billion for child care assistance + $7B for enhanced broadband access.

Nutrition & Agriculture – $26B for food stamps, food banks, school/daycare feeding programs, and payments, purchases, and loans to farmers and ranchers impacted by covid-related losses.

Rental Assistance – the eviction moratorium is extended through 1/31/2021 (for now). $25B is authorized to help troubled renters and landlords by paying future rent and utilities as well as back rent owed or existing utility bills.

SBA Loan Relief – The CARES Act authorized SBA to pay up to six months of principal and interest on existing Section 7 SBA Loans for impacted borrowers. This Act extends that by another three months.

Economic Injury Disaster Loans (EIDL) – $20B in additional funding for businesses in low-income communities + $15B of dedicated funding is set aside for live venues, independent movie theatres, and cultural institutions.

Credit for Paid Sick + Family Leave – this was created by the Families First Act and is now extended through 3/31/2021 (was 12/31/2020).

Employee Retention Tax Credit – created under the CARES Act, is extended through 6/30/2021 and improved. It’s now up to 70% of wages capped at $10k of wages per employee per quarter, instead of 50% capped at $10k in total. Business qualifies if revenue for the quarter was down at least 20% from the same quarter in 2019. Important: it appears this credit is now allowed along with a PPP Loan (under the CARES Act, it was one or the other), though you still can’t double count the same wages for the credit and PPP forgiveness.

Payroll Tax Deferral – the president signed an executive order in September allowing employers to opt in to a payroll tax deferral for employees. Almost no one did (except the government) because it was too risky on the employer and deferral for a few months was pretty meaningless. Those that did were supposed to repay the deferral by 4/30/2021. That has now been extended to 12/31/2021, giving more time to spread out the payback.

Lookback for Earned Income Tax Credit and Refundable Child Care Credit – taxpayers can, but don’t have to, use 2019 income instead of 2020 income to qualify for these in 2020.

Residential Solar Tax Credit – this was reduced to 26% of the cost of the project in 2020, scheduled to drop to 22% in 2021, and then eliminated after 2021. The Act extends the 26% credit for 2021 and 2022, dropping to 22% for 2023. It is now eliminated in 2024, unless additional legislation is passed.

Employer Paid Student Loans – Employers can continue to give up to $5250 per year tax-free to employees for student loan principal and interest repayment (either direct to the loan or to the employee to pay the loan). This is extended through 2025 (was set to expire at the end of 2020).

Tuition Deduction / Lifetime Learning Credit – The tuition deduction, unless extended in other legislation, is gone. Instead, there is now a higher income threshold for the Lifetime Learning Credit, now sync’d up with the American Opportunity Credit phaseout ($80-90k single / $160-180k married).

Student Loan Payment Forbearance – this WAS NOT extended in the Act. Student loan payments resume 1/1/2021.

Retirement Plan Distributions / Loans – The CARES Act allowed up to $100k of distributions from retirement plans for covid-impacted individuals, waiving the 10% penalty, and allowing the amounts to be repaid over 3 years such that no net tax would be owed. It also raised the 401k loan amount to the minimum of $100k or 100% of the balance (from $50k or 50%). These were effective through 12/30/2020. This treatment is now extended to non-covid-related Federally declared disaster areas between 1/1/2020 and 2/25/2021 where the individual has their principal place of residence and is economically impacted by the disaster.

Retirement Plan Required Minimum Distributions – these were waived by the CARES Act for 2020. This WAS NOT extended by the new Act. RMDs will be required for 2021 unless additional legislation is passed.

Medical Expenses Deduction – the deduction for medical expenses has been bouncing back and forth between a 7.5% AGI floor and a 10% AGI floor for years. It’s 7.5% for 2020 and was supposed to revert back to 10% for 2021. The Act sets this to 7.5% PERMANENTLY. One thing I can stop writing about every year!

Mortgage insurance premiums – remain deductible for another year through 2021.

The taxability of forgiven housing debt (foreclosure/short-sale) – is extended to 2025, but the amount is reduced to $375k single / $750k married.

Charitable Giving – The $300 charitable contribution deduction for those who don’t itemize is sticking around for 2021 now and joint filers will get $600 instead of $300 for 2021. Remember this is for cash donations only and donations to a Donor Advised Fund don’t count. And, the cap on the portion of your income you can give via a cash donation (other than to a Donor Advised Fund) and deduct stays at 100% for 2021.

Healthcare & Dependent Care Flexible Spending Account (FSA) flexibility – The Act allows plans to allow 2020 unused amounts can carryover to 2021 and 2021 can carryover to 2022. Additionally, the Act allows 2021 elections to be modified even though benefits enrollment is now closed for most employees. However, this only updates what the law will allow employer plans to do. The plans themselves would have to adopt the change in order for employees to be able to use the increased flexibility. Check with your benefits rep to see if your plan is adopting / has adopted the change.

Educator’s Deduction – this is the $250 per year that teachers get to deduct for money spent on school supplies for their classrooms (as if that’s all teacher’s spend on their classrooms). PPE and cleaning supplies now qualify for that $250.

Business Meals – for business owners, restaurant meals are 100% deductible for 2021 and 2022 (formerly only 50% deductible) as long as they meet the requirements of the previous 50% deduction (i.e. non-lavish, taxpayer is present, etc.). Note that this still does not include employee expenses, only schedule C filers. Applies to dine-in or take-out.

Surprise Billing Fix – an attempt to reduce the amount of “surprise billing”, which typically occurs when a patient goes to an in-network facility and uses an in-network doctor, but is provided services by an out-of-network provider along the way (e.g. anesthesiology, transportation, etc.). There are lots of carve outs and exceptions, so I’m skeptical of how much this really fixes, but it’s a start at least, going into effect in 2022. I’m sure much more will be written on the implications here soon.

Financial Aid Changes – Student Loan Application (FAFSA) simplification – lots of changes here, but they don’t go into effect until 2023. In the interest of time, I’ll table this one for now. Just know there are changes coming. Additionally, the number of Pell Grants will be increased.

In order to reach a bipartisan agreement, both of the following WERE NOT INCLUDED in the Act:

Business liability protection (i.e. can’t sue if you get covid at a business as long as they were following CDC guidelines), which Republicans wanted

State and Local Aid above and beyond that specifically budgeted for the items in the Act, which Democrats wanted.

I suspect there will be more to come, though the type of relief/stimulus likely depends on the outcome of the GA Senate run-offs. There is already a proposal to increase the $600 direct payments to $2000, supported by the House and the President, but that will have a difficult time in the Senate. We’ll have to wait and see what happens.

The IRS announced yesterday that it is relaxing the rules around the use-it-or-lose-it “feature” of healthcare flexible spending accounts (FSAs). Plan sponsors will now be able to all plan members to rollover up to $500 of unspent FSA dollars into the following year’s FSA. Currently, any money not used during the plan year would be forfeited, though most plans do have a grace period that allows until 3/15 of the following year to zero out balances before forfeiture. Starting with the 2013 calendar year, plan sponsors can now choose whether to:

Implement the new $500 rollover rule OR

Maintain the grace period rule that extends the deadline for using a year’s FSA funds until 3/15 of the following year OR

Neither

It is up to the employer (plan sponsor) to set the rules for the given plan. Since 2013 is almost over and most plans already allow the grace period rule, I suspect few plans will be changed for the 2013 plan year to allow the new rule. It is possible that plans may be updated to the new $500 rollover rule for 2014. If you’re going through your Annual Benefits Enrollment, plan to use a healthcare FSA, and have not received any direction form your employer as to whether or not they plan to implement the new rule, please contact your HR representative and ask.

Full text for the rule change can be found in Notice 2013 -71 on the IRS Website.