This post contains the usual returns by asset class for this past quarter (by representative ETF), year-to-date, last 12 months, last five years, last ten years, and since the covid low (3/23/2020). While there is still no predictive power in this data, I’ll continue to post this quarterly for those of you that are interested.

A few notes:

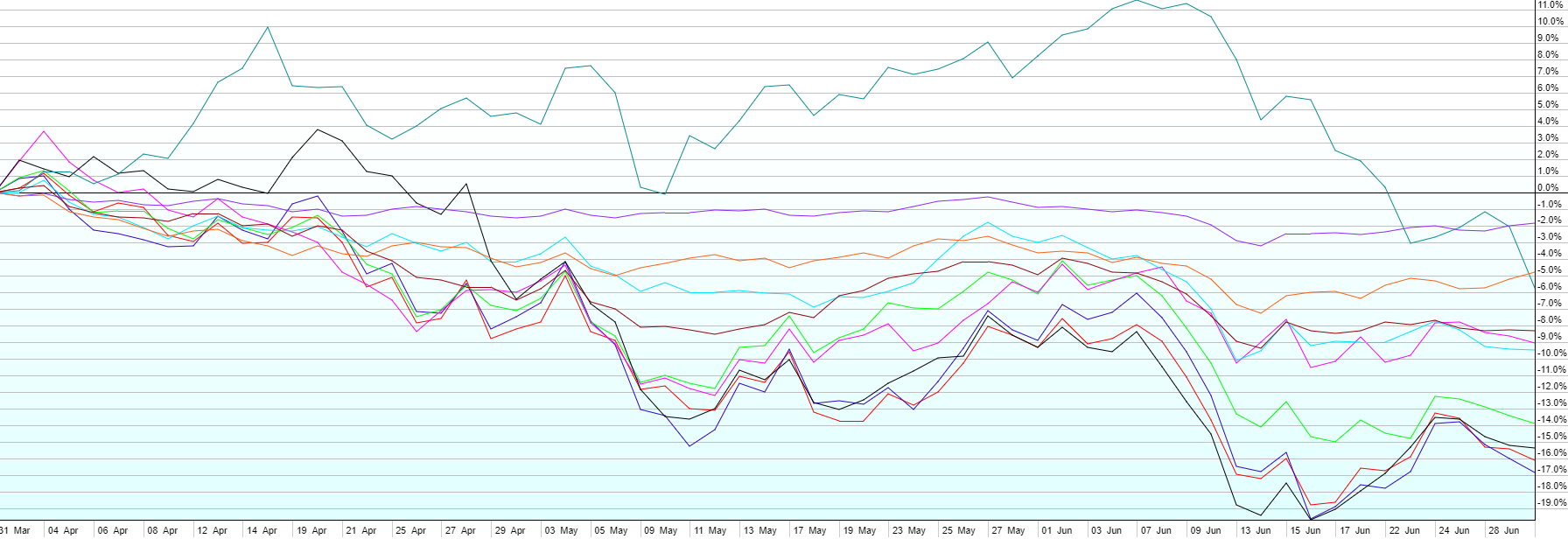

- Q2 was an awful quarter for stocks across the board. Emerging markets performed best out of the major asset classes (-9%), with foreign developed (-14%), US REITs (-15%), US Large Cap (-16%), and US Small Cap (-17%) lagging behind. Continued interest rate hikes by the Federal Reserve to battle continued increases in inflation have pressured asset values and sparked fears of a sharp economic slowdown as a result. Whether we’re technically in a recession now (two consecutive quarters of negative GDP growth) or not, it’s clear that the Fed is determined to slow inflation at all costs right now, both by raising rates and via Quantitative Tightening (QT), or selling assets from their balance sheet.

- Bonds had another tough quarter too in Q2. Long-term treasuries (TLT, not shown above) were down 13% in the quarter, now down 22% YTD as rates spiked, and prices (which are inversely correlated with rates) sank. We generally keep the bond side of client portfolios much shorter in duration, and include inflation-protected bonds, both of which faired much better again. Short-term inflation protected treasuries were only down 1.2% for the quarter., with short-term investment-grade credit down 1%.

- Even commodities turned in negative performance for Q2. After being up as much as 11% for the quarter in early June, a sharp downturn across the board, and especially in energy delivered a -6% quarter.

- The worst performing areas of the market in Q2 were the same as in Q1. The ARK Innovation ETF (ARKK), down almost 30% in Q1, tumbled another 40% in Q2, and is now down almost 75% from its 2021 peak. On the flip side, US value stocks are still holding up relatively well, down only 9% YTD vs. the S&P 500’s -20%.

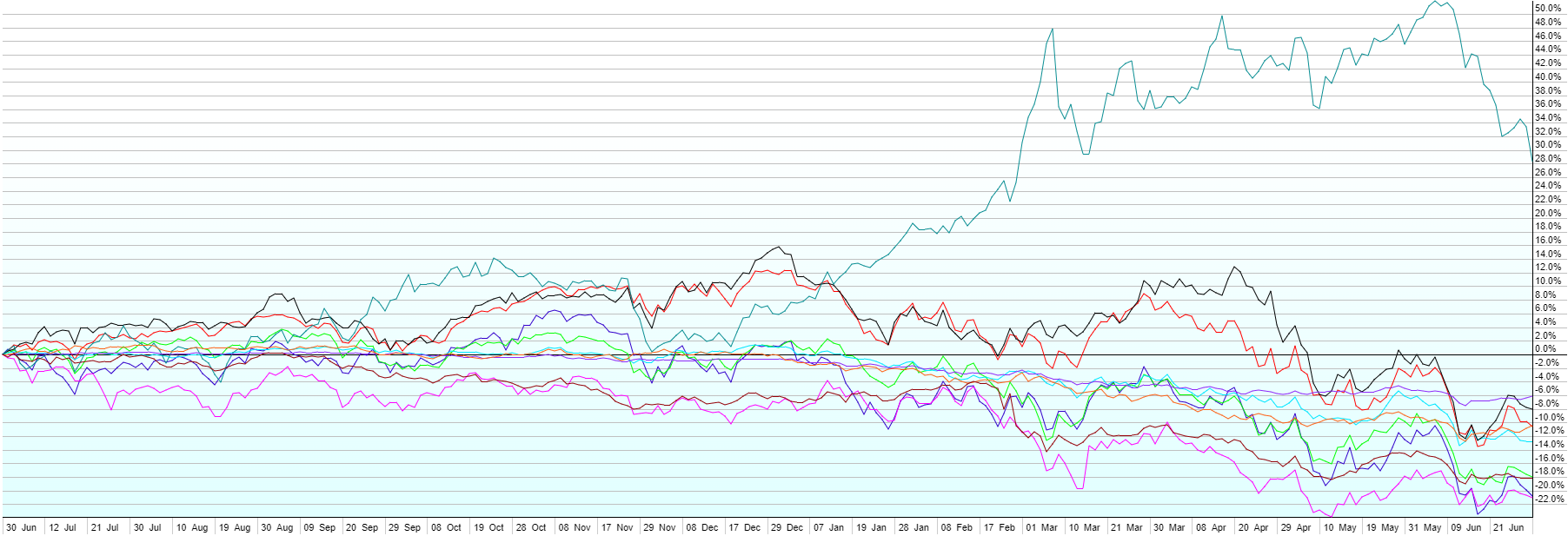

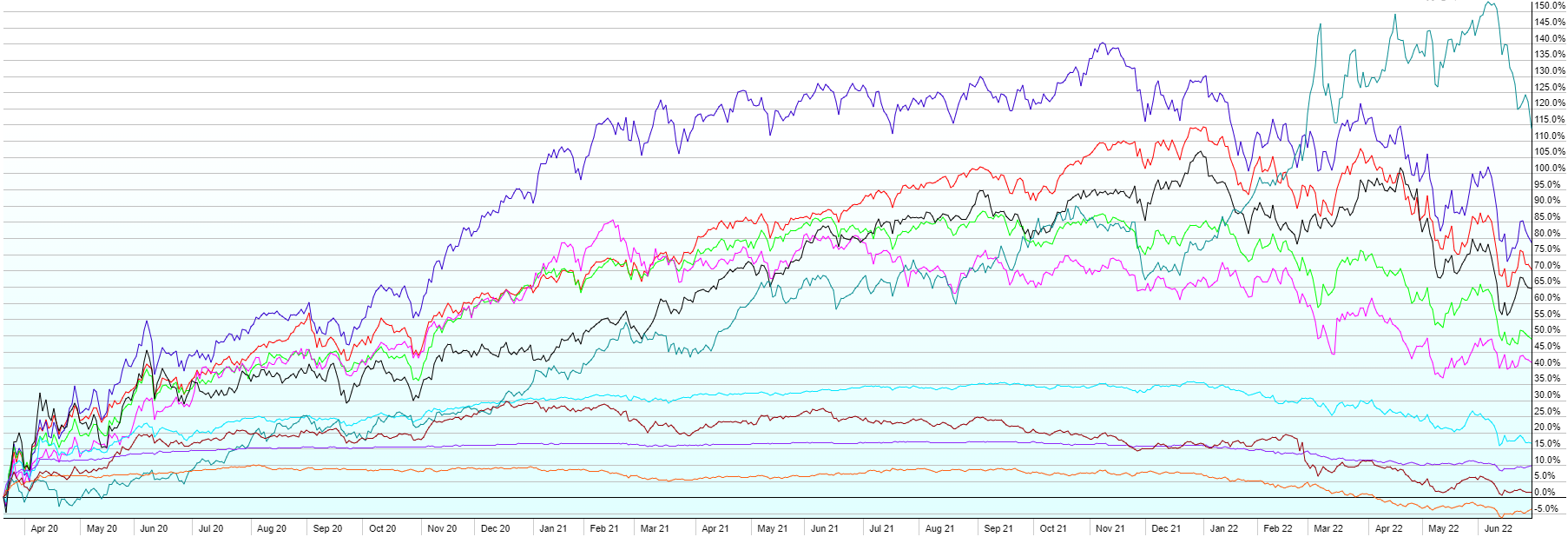

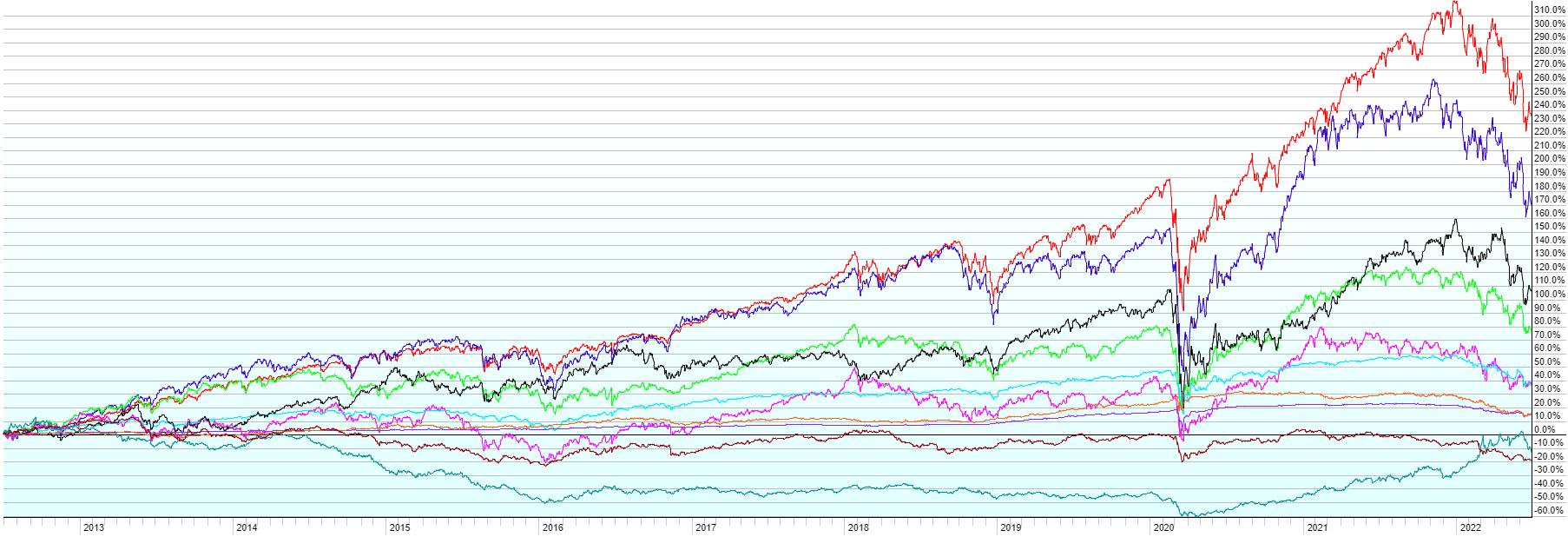

- Markets in general are still sharply up from the 2020 Covid lows and over the last 5 and 10 years. US Large and Small Caps have dominated global performance over the last decade.