As I’ve wrote back in May, inflation, leading to higher interest rates, leading to fear of a sharp economic slowdown, seems to be dominating stock/bond market performance of late (and not in a good way). I’ve been seeing some signs of inflation cooling of late and wanted to share a few, because you generally don’t get early/good signs of stuff like this on the news. Remember though, it’s very doubtful that overall prices will ever come back down to where they were. What’s were looking for is the increase in prices going forward to moderate back toward 2% per year. Below are some signs of actual price moderation, which would likely start to flow through the economy and ease the rate of growth of other prices. Has inflation peaked? No one has a crystal ball, but I’d say the below charts are a good sign for the short-term.

1) Baltic Dry Index – benchmark for the price of moving the major raw materials by sea. Moderating after the huge spike in late 2021.

2) US Natural Gas – a heavy input into the price of electricity in the US. Sharp decline from recent peak as exporting to Europe has been disrupted by facility issues.

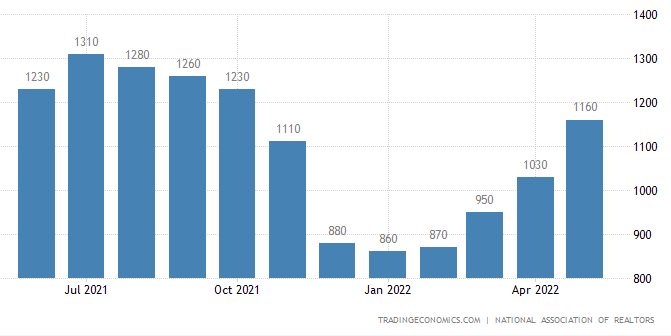

3) Total Homes Currently For Sale – rising sharply after hitting all-time low levels that drove up prices over the last year. When combined with higher mortgage rates, this should slow down an overheated housing market.

4) Lumber – key input into new home construction costs, down over 60% from 2021 peak and more than 50% from winter 2022 just a few months ago.

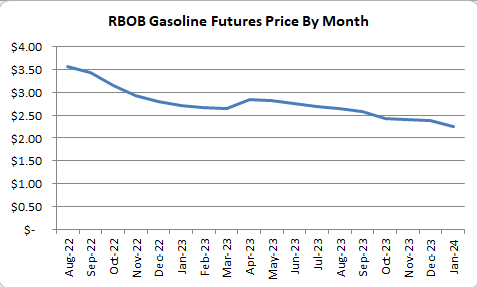

5a) Gasoline Futures (RBOB) – we all know prices at the pump are a LOT higher over the past few months, but the price of gasoline futures is down pretty sharply from peak a few weeks ago. That takes a while to filter through the system since prices come down only a cent or two per day via competition between stations. But it’s a good sign. The current front month futures price of $3.55/gallon would generally translate to ~$4.35 national average at the pump.

5b) Gasoline Futures (RBOB) – In addition to the front month futures contract trending down, the shape of the futures curve is also down with Jan 2023 down to $2.70/gallon and Dec 2024 all the way down to $2.25.

6) 5-year Breakeven Inflation Rate – by comparing the interest rate on Inflation Protected Treasuries (TIPS) vs. Non-Inflation-Protected Treasuries, we can estimate the inflation rate that the market has priced in over the next 5 years on average. After rising considerably (though still nowhere near the current 8%+ / year actual levels, the breakeven rate has fallen and is getting closer to the Fed’s comfort range ~2%.

So maybe, just maybe, we’ve seen the worst, at least for the short-term. Much depends on both controllable factors like policy responses (hint: cutting the gas tax and handing out cash aren’t going to help increase supply or decrease demand) as well as non-controllable factors like the war in Ukraine. (global energy and food supplies this winter are going to be tight). Even if food/energy inflation stays high, if the “core” inflation moderates, it will give the Fed room to be a bit more dovish, and that’s likely to be taken positively by the financial markets.