*** We believe communicating with our clients is of utmost importance, especially during turbulent times in the market. While we don’t claim to have a crystal ball on the future of any financial market at a given point in time, we do believe that keeping clients informed on why things are happening increases their comfort level and understanding. This post contains an excerpt from the PWA Q2 2011 newsletter to clients, sent just the end of “QE2” (Fed stops buying new treasuries), explain three key issues for a continued rebound in the economy, as part of that communication effort***

…

• The End of QE – On 3/24/09, just after what we now know was the stock market bottom, I wrote in a “Market Update” note to clients that the announcement that the Federal Reserve was going to purchase U.S. Treasuries and other securities represented a “game changer” for the financial markets. Those purchases became known as Quantitative Easing (QE) with two distinct rounds of purchases being coined “QE1” and “QE2”. These were in fact a game-changer for the markets, with the S&P 500 rallying more than 100% from March ’09 to April ’11. They were a game-changer because the Fed was, in simplified terms, printing money to buy financial assets which put that newly printed money into circulation to offset the deflationary spiral that was occurring (the value of everything from houses, to bank assets, to the stock market, to commodities was falling rapidly and simultaneously causing credit markets, job markets, and the overall economy to grind to a halt). As of July 1st of this year, the Fed ended QE2 and has signaled that a QE3 is unlikely. This means the game-changer is over. However, the Fed is not selling the assets they’ve purchased to date and they will keep reinvesting in those assets as they mature which means we don’t expect a game-changer in the other direction to send the markets back down. What we do expect is that the days of 50% per year stock market gains are behind us for quite a while. We also expect interest rates to start to gradually rise on medium to long-term treasuries and mortgages, though probably not sharply because any sharp increase would set the economy back and likely force more intervention from the Fed. In the next 12-months we expect short-term rates on savings accounts, CDs, and short-term bonds to start to gradually increase as the Fed hikes the Fed Funds rate back to something less extraordinary (we believe 2-3% would still provide support for economic recovery without risking the inflationary dangers of the 0% emergency rate we have today. Finally, we expect a higher level of volatility (up and down) in all financial markets as the Fed-induced tailwind is no longer behind us and now the economy, business cycle, productivity, earnings, and jobs will take more focus.

• The Debt Ceiling – Much is being made of the U.S. debt ceiling and what might happen if it’s not raised and we’re unable to pay our bills. For the most part, this is political grandstanding. There is absolute certainty that the debt ceiling will be raised. But, there’s an important problem in the way Congress is currently dealing with the issue. August 2nd has been set as the “deadline” by the treasury secretary by which the ceiling must be raised in order to proceed with business as usual. For this reason, the credit rating agencies have to consider the possibility that the U.S. will not be able to pay its debts if the ceiling is not raised by that date. Ironically, Congress bashed the credit agencies for maintaining AAA status on collateralized debt obligations that later failed during the peak of the financial crisis, arguing that any risk of default should have caused an immediate downgrade of those instruments way before the crisis occurred. Those same credit rating agencies must now act accordingly and not wait until August 2nd to cut the U.S. rating or they risk having a AAA rating on August 2nd morning and a default rating on August 2nd evening. This means the real deadline to raise the limit is well before August 2nd, because a downgrade of the U.S. credit rating, if taken seriously by the world, will having a snowball effect through the financial markets and set off another deep, albeit temporary, financial crisis. The President’s comment that he will not approve a short-term extension, while obviously in good a faith effort to try to prevent this from being a recurring quarterly problem, actually worsens the situation because it makes the possibility of no deal by August 2nd more likely to the credit agencies. Congress is now playing a game of chicken and I expect a short-term deal is likely with an understanding of more short-term deals through the 2012 elections which will keep the ratings agencies at bay for now. In the meantime though, expect potentially violent moves in the markets, akin to those of the days of TARP being voted on, as momentum traders try to take advantage of the headlines. Since even a credit downgrade would be temporary (garnering a swift response in Congress if it ever did happen), market volatility due to these events is in my opinion, nothing more than an opportunity to rebalance portfolios taking advantage of dips in the market and to get a 401k or other savings contribution in at a cheaper price than without the debt ceiling issue. This issue will pass. The longer-term question of our government’s ability to govern if it’s willing to put us in these kinds of situations to begin with is a much broader issue but I’ll leave that discussion to those who enjoy politics.

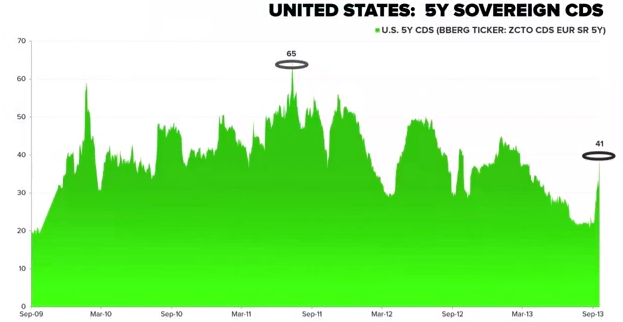

• European Sovereign Debt – A less-urgent, but much more important issue to long-term global financial markets is the vast amount of sovereign debt that exists in the world and the sudden realization by financial markets that some countries truly may not be able to pay their bills. This issue is not about an arbitrarily set debt ceiling. Countries like Greece and Ireland are struggling to pay their debts because they’ve taken on so much debt that tax revenues can’t support government spending plus interest payments any longer. These countries, with others like Italy, Portugal, and potentially Spain, not too far behind them, have simply lived on a national credit card for the last decade and are now forced with extreme austerity in return for global bailouts or default. Default means the loans made to those countries become worthless and the banks holding those loans lose the loans as assets. This has the potential to kick off a global financial crisis that is all too familiar after the ‘08/’09 Lehman Brothers default created much of the same. It can also kick off a currency crisis as it threatens the Euro, thereby strengthening the U.S. Dollar and causing harm in our own recovery as it makes our goods, services, and assets seem more expensive to the rest of the world. So far, rescue packages from the International Monetary Fund have staved off default for Ireland & Greece, but this warrants further monitoring. There are three important actions to take here:

· Like others, we have no crystal ball and believe that markets price information and risks fairly in general. That means that in most cases the market would fall before we have reason to believe it would fall or it would rise before we have reason to believe it would rise meaning there is no way to time news events. However, as I’ve discussed with all of you at one point or another, if I hear the whisper of a freight train coming, and sometimes it comes without making a whisper first, I will take corrective action. This means moving all models temporarily to a slightly more conservative allocation or using other protective measures as I see fit.

· It’s easy to be complacent when the stock market is rallying like it has for the better part of the last 28 months. If you have short-term needs for your money that is currently invested as if it was not needed for the short-term, please communicate that need to me ASAP. If your portfolio is 80% stocks and the stock market falls 50%, which has happened twice in the last decade, you will lose ~40% of your portfolio. For long-term money, by definition, you don’t need it over the short-term so that’s not an issue. In that case, continue to invest as planned, buying at lower prices if markets fall and when markets eventually recover you’ll actually be better off than if the fall hadn’t happened. For short-term money though, that kind of a loss could mean not being able to fulfill a goal and goal-fulfillment is the only reason to invest.

· Expect the market to move both up and down. Many have become accustomed to seeing their portfolio balances only increase, and quite sharply quarter after quarter. Don’t be shocked to see more volatility. As long as you’ve heeded the point in the preceding bullet, and you have an overarching financial plan, don’t worry about the short-term movements of the markets. The only ways to ensure that your account statements will only show increases in value are to 1) keep your money in the bank earning slightly more than 0% per year in interest while the cost of living increases far faster, or 2) have a crooked financial advisor that’s cooking the books (and we all know how that ends… google “Bernard Madoff”).

…