There’s an old saying on Wall Street that markets tend to climb a wall of worry. That couldn’t be more true over the last few years. Whether it’s our own political and fiscal dysfunction, high unemployment, geopolitical tensions in the middle east, a debt crisis in Europe, slowing growth in emerging markets like China, the old “too much too fast” theory on stock market gains, the Federal Reserve and other central banks printing money, the potential end of that money printing, etc., there has been no shortage of reasons to worry the next correction cometh soon. Yet the stock market, as it usually does, makes a fool of those who try to predict it’s short-term behavior, and continues to climb that wall of worry. There is also no shortage of stock market prognosticators. Despite natural instincts to attempt to join them, I avoid it wherever possible and help clients design a plan that will be successful regardless of what the stock market does over the short-term. We don’t have to predict the short-term movements of the stock market in order to invest money toward particular financial goals. We simply have to keep money that’s necessary for short-term goals, predominantly out of the stock market!

As strongly as I feel that trying to predict market movements is a fools game, I do think it’s possible and necessary to present a rational explanation for what the stock market has done in the recent past. This is to help clients past the natural fears that prevent them from sticking to their plan at times like 2009 (and for some, even now because of a feeling that the market is “too high”). It’s also to help clients past the natural greed that can develop when you see cash earning nothing for years while the stock market gains 200%. I believe that those gains came as part of a recovery cycle from very depressed levels, spurred on by the actions of the Federal Reserve and other central banks around the world. Those actions (low short-term interest rates, quantitative easing or “QE”, and forward guidance in the form of promised low rates for an extended amount of time) allowed the recovery cycle to take place in an environment that could otherwise have taken decades. I think of the recovery in four phases of realization that impart increasing and self-reinforcing confidence in the economy and financial markets. I describe them in more detail below, but for those without the time/desire to read that detail, they run from 1) “the world is not ending”, 2) “we’re growing again, but only because of the Fed”, 3) “interest rates are absurdly low and won’t stay that way for long” to 4) “we’re growing and interest rates are staying low even as the Fed pulls back”. With each realization, the stock market has made a move higher. The phases, in more detail:

· Pre-Recovery: Markets plunging, unemployment soaring, Lehman default, credit markets seizing up… I described the aggregate psychology of the markets during this period as beginning to price in the potential for the end of the financial world.

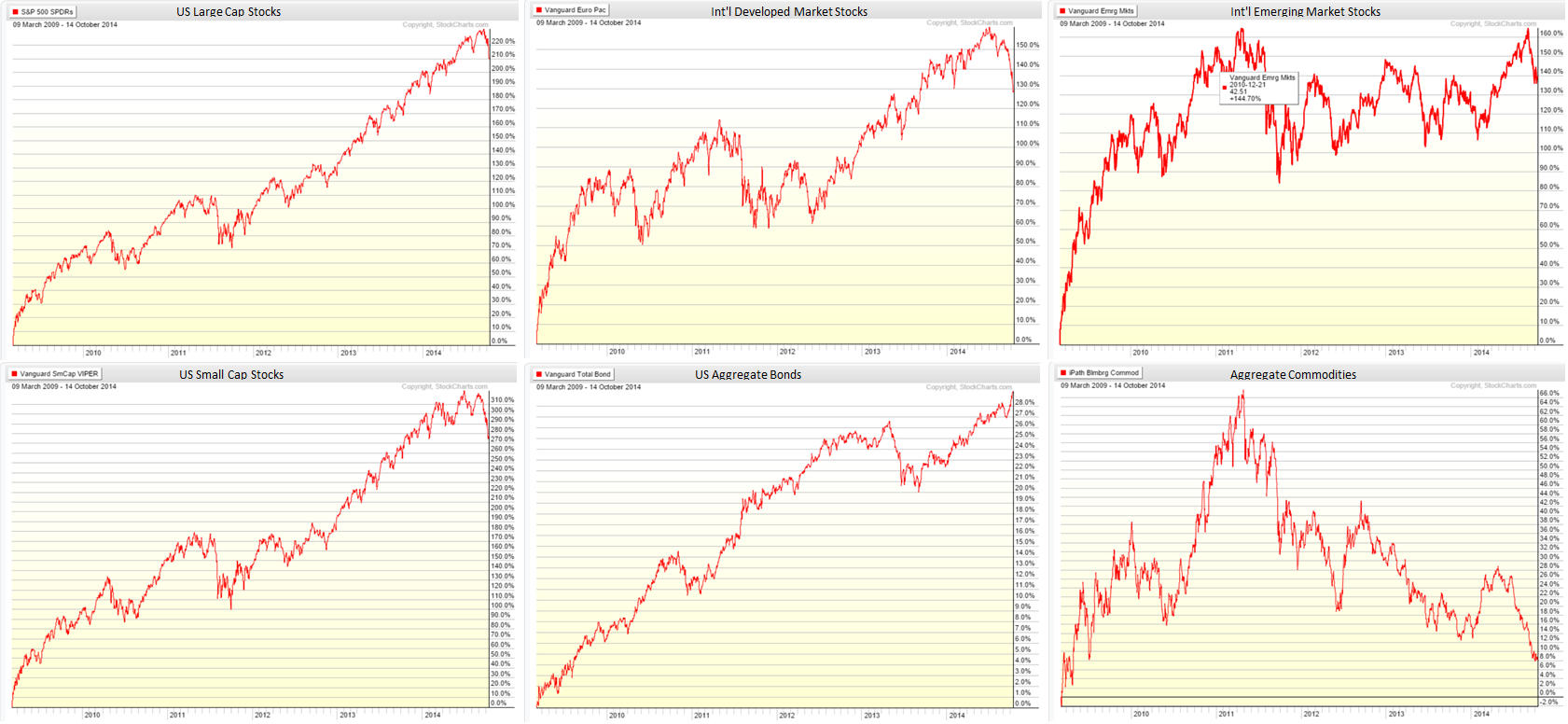

· Recovery Phase 1: Fed starts ZIRP (zero interest rate policy) and QE (quantitative easing). Unemployment peaks. Stock market bottoms. On 3/24/09, I wrote about QE as a “game changer”, just after that bottom. I’d describe the psychology of this period as pricing out the potential for the end of the financial world. The stock market in March of 2009 had essentially fallen 60% from peak in October 2007. Earnings estimates for S&P 500 companies for the next 12 months had fallen from over $100 per share at peak to ~$60 per share. At the same time, fear in the markets led to PE contraction and the S&P 500 PE fell to just over 10 (for more on PE and market valuation, please see this recent blog post). I remember discussing this with a colleague and stating that “applying a trough multiple to trough earnings is a trough in intelligence.” When earnings fall and have a massive path of recovery in sight (growth back to peak earnings over the next several years), PEs should expand to reflect that, not contract. This is exactly what happened. Over just a few months, PEs expanded back to their market average around 15-16 as the S&P 500 gained 50% from bottom with little change in future earnings estimates.

· Recovery Phase 2: Over the next few years, the Fed continues QE and adds its guidance that rates will stay low for an extended period. The economy begins to grow again, slowly. Job creation picks up to slightly above the level of population growth. Unemployment slowly begins to fall. The stock market continues to climb, but now due to increases in earnings due to a growing economy. At the same time, the unsatisfyingly slow growth weighs on confidence and though earnings are expanding, PEs begin to fall again on concerns for future growth.

· Recovery Phase 3: The Fed launches its new open-ended QE program, called “QE Infinity” by some (see Monetary Bazooka Fired). The Fed promises to keep rates low even longer (first through 2015, then till unemployment falls to a threshold, then beyond that). Interest rates plunge to historical lows as a result of QE and the Fed’s promise. The economy still grows slowly, job creation is still slow, and unemployment continues to fall slowly. Confidence seems a bit higher in the economy and in the Fed’s ability to create a no-lose situation. PEs expand again along with growing earnings and the stock market makes another strong move higher. This time though, I think the reason for the PE expansion is the promise of lower long-term rates for a very long time. We see dividend-paying stocks like utilities and REITs due extremely well in this environment because low interest rates makes their high dividends seem even more valuable. The economic recovery still doesn’t seem to have reached self-sufficiency though with the Fed still pushing it. What happens when the training wheels come off the bike and it has to pedal on its own? In phase 3, that was the market’s biggest worry.

· Recovery Phase 4: The Fed announces the tapering of its QE program, slowing bond purchases with hope of ending the program by late 2014. Markets hiccup on fear that this marks the beginning of the end for low rates. Rates begin to increase, PEs contract, and the stock market dips into the summer of 2013. The Fed reacts by strengthening its resolve to keep rates low well beyond the end of QE. Into early 2014 as the Fed continues to cut back on QE, Europe and Japan embark on monetary easing programs (Japan is in a massive QE program already and Europe begins to hint at one to come). European interest rates, even those for fiscally troubled countries like Italy and Spain plunge to levels that approach US interest rates because of growing confidence that the European Central Bank (ECB) will do anything and everything to make sure those countries don’t default. If Italy’s 10-year treasury yields 3% and the US 10-year treasury (thought to be much much safer than Italy’s bonds) yields 3%, that puts a cap on how much US interest rates can rise. Now, in mid-2014, even though the Fed is almost done with QE, the fear of rapidly rising rates remains in check due to central bank actions overseas. If rates are going to continue to remain low long-term because of those actions, then PEs should expand again to reflect that. Additionally, confidence that the economy won’t falter as rates rise takes hold. Housing can continue to recover. Employers can hire and plan for growth. Consumers can spend without worry of erosion in the jobs market. This is precisely what has happened over the past few months as unemployment has taken another dip down and job creation has picked up sharply. PEs have expanded back out to 15-16 on the S&P 500 (based on next 12 month’s earnings), right at their historical average. The recovery now appears closer to being self-sustaining, or at least is no longer dependent on the Fed’s QE (might still be dependent on Europe and Japan though).

That brings us to present day. Can self-sustaining (or ECB induced) economic growth increase earnings enough to push the stock market higher? Can the expectation of low interest rates for the foreseeable future push PEs above historic averages thereby pushing the stock market higher? Could both happen and really put upward pressure on the market without a spike in inflation? I believe this latest run up in stocks has come from more and more belief that the answer to all of those questions can be “yes”. This, in my opinion, is where the danger lies. If the market starts to price in “yes” answers, but the economy falters and earnings estimates turn out to be too high, or the ECB doesn’t go as far as everyone is expecting, or inflation starts to rear its ugly head and interest rates start to rise, putting pressure on PEs, we could be in for that correction everyone has been expecting for the last 5 years and 200% of gains. Remember, when the wall of worry disappears, stocks may no longer have anything to climb. So, there are lots of reasons to be positive and lots of reasons to worry about being positive. Again, I can’t predict the future, but I do hope my interpretation of why stocks have climbed 200% in 5 years helps you see that we’re not living in a world of irrational exuberance. I also hope my warnings of what could go wrong in the future can keep the greed-monster in check. Stocks are not massively over-valued, nor are they under-valued (S&P 500 PE is 15.55 at the time of this writing, which right about the historical average). There are pockets of stocks that seem very expensive (small cap growth companies, especially in the social media and cloud space), but not the market overall. Stocks have merely recovered from insanely low valuations, have reflected the growth in earnings in recent years, and have adjusted to a new level of long-term interest rates. While corporate margins are at the typical cycle highs, there is still room for revenue expansion if the economy as a whole picks up. We just need to be careful not to count on sharply rising earnings before they occur and not to price in very low long-term rates forever (forever is a very long-time).

This brings me to a related and important point. A few of you have asked in recent months for my stance on what I would do in an insanely and clearly overvalued stock market situation. If such a situation was to present itself (and seeing it might be like trying to drive around a corner while looking in the rear view mirror), I’m prepared to move models to a more conservative allocation and wait for the economy to catch up to the stock market. I’m not saying that evidence will always present itself before the market falls (it would be atypical if it did). I’m not saying we’ll ever move to “all cash” or “all in” at any point regardless of the evidence. I am saying that in an extremely overvalued situation, expectations of future returns will be lower, but risk will be higher. If that’s overwhelmingly clear, it would make sense to reduce risk temporarily, as a matter of prudence, not as a prediction of an impending market disaster. I have been close to doing this a few times in the past, but have a high tolerance when it comes to “overwhelmingly clear”, and so I didn’t act. Doing so would have missed at least a period of one of the biggest bull markets in history. Making such a move, even a small one, is not something I’d take lightly (especially with tax complications in mind that can offset any benefit to being right). If I ever do decide to take this step, I will communicate further on how it will be implemented and of course give all clients the opportunity to ask any questions and express any concerns. What I think is far more important than worrying about this sort of situation is making sure that your asset allocation is reasonable for your financial goals, that you can handle the downside risk without being scared when that risk becomes a reality, and that the upside returns target the returns you need to achieve your goals. Along those lines, after bashing stock market predictions earlier in this message, I’ll end it with two of my own. First, sometime in the next 50 years, the stock market is going to lose at least half of its value over a very short period of time. It might have started yesterday. It might start two decades from now. But, it’s inevitably going to happen. Don’t let the good times lure you into risking money you can’t afford to risk in the stock market. We use bonds and other asset classes for short-term goals because of their safety. We use cash for emergency funds because of the liquidity it provides. We can target an overall asset allocation that gives the best chance of hitting your goals regardless of what the stock market does, but we can’t be greedy and gamble for high returns over the short-term. Second, unless the world comes to a brutal end in some cataclysmic event that would make money useless anyway, the stock market will be much higher 50 years from now than it is today. A dollar invested in the S&P 500 in 1963 would be worth $116 today. That’s despite losing 10% in 1966, more than 42% in 1973-74, almost 50% from late 2000 to early 2003, and almost 60% from late 2007 to early 2009. Amazingly, even a dollar invested at the peak in Oct 2007 would be worth $1.47 today, almost a 50% return. Don’t let fear of the market falling tomorrow stop you from investing for the long-term today. There is no upside to hoarding cash, especially when it earns less than the rate of inflation like it does today. Stick to your plan in the good times and the bad, and always remember that there will be more of both in the future.