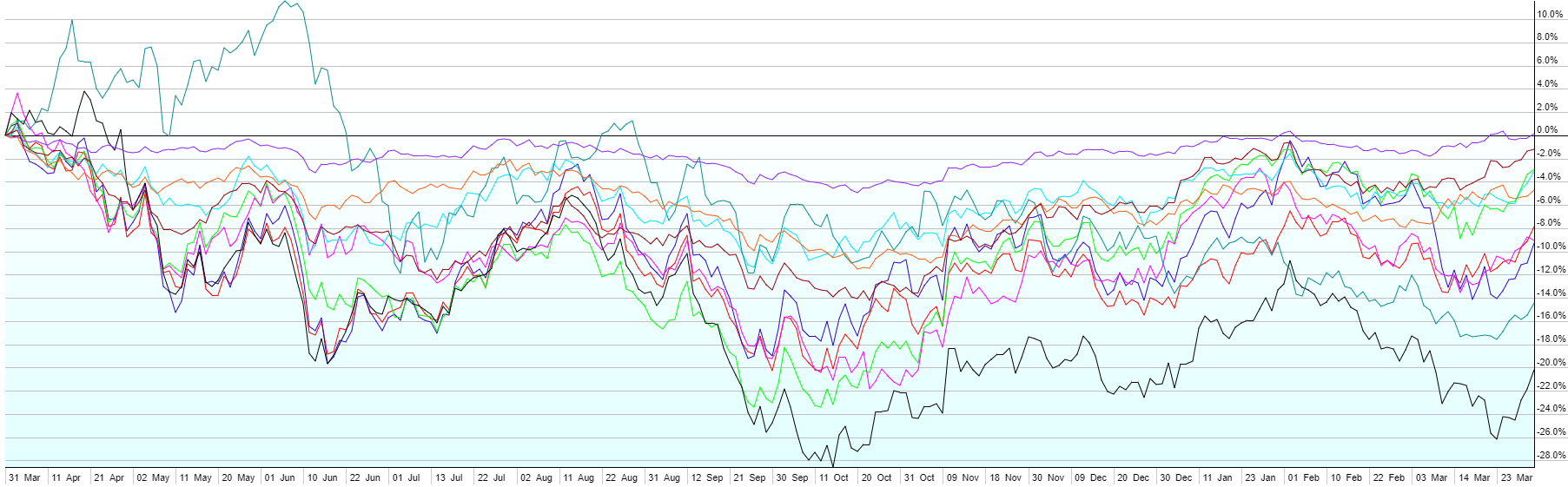

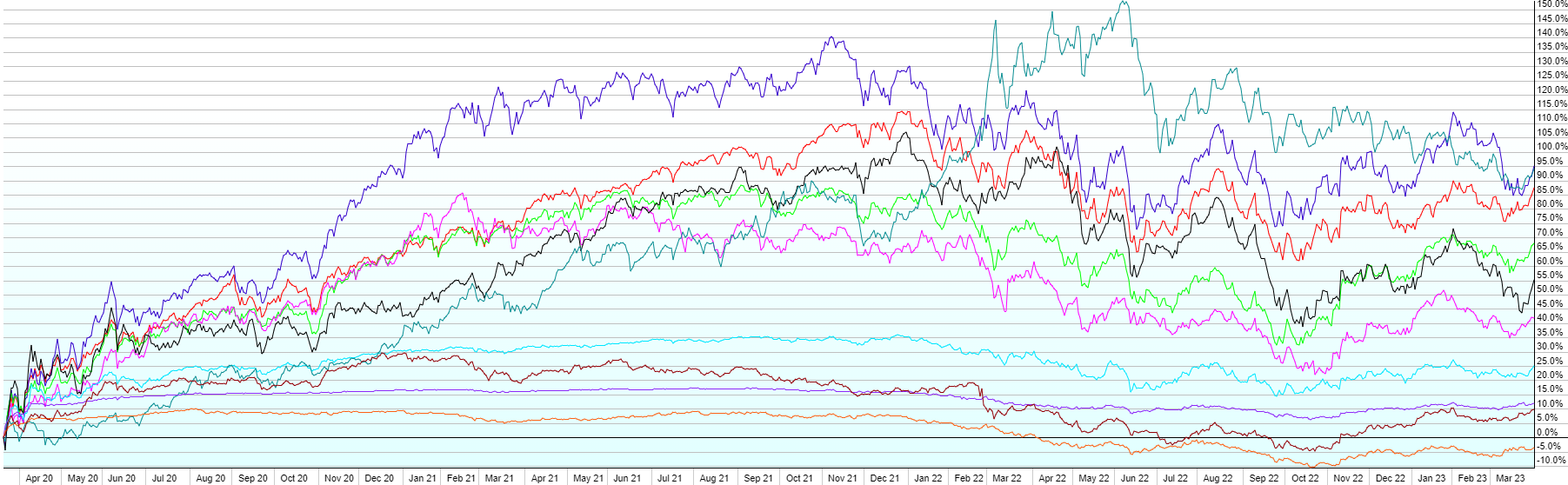

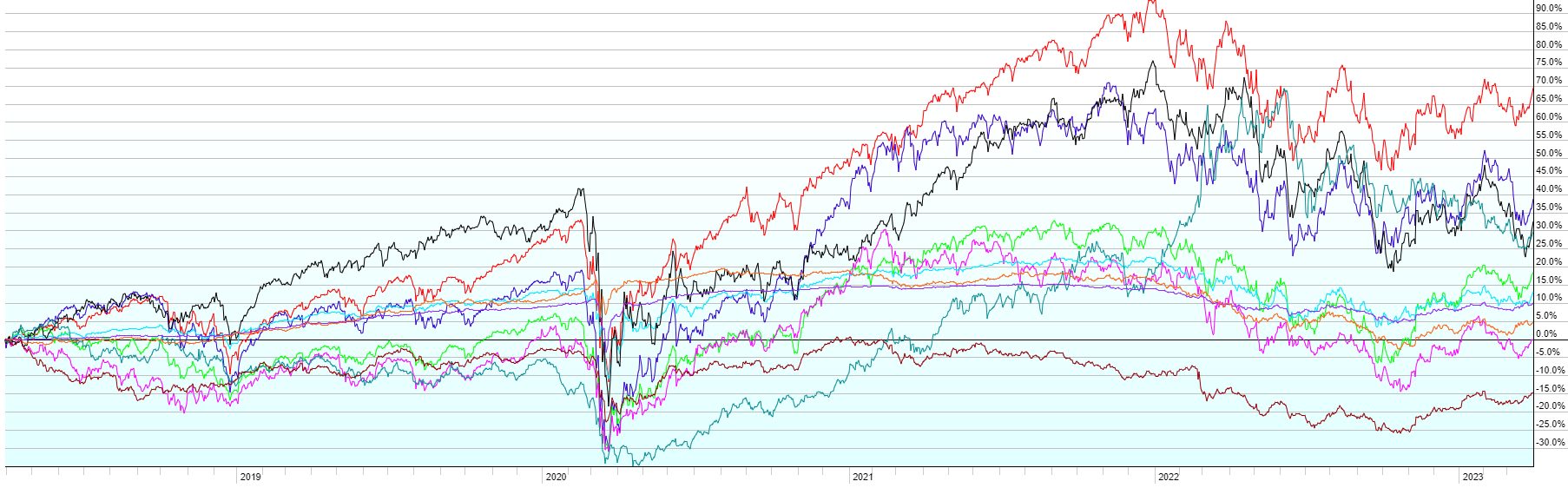

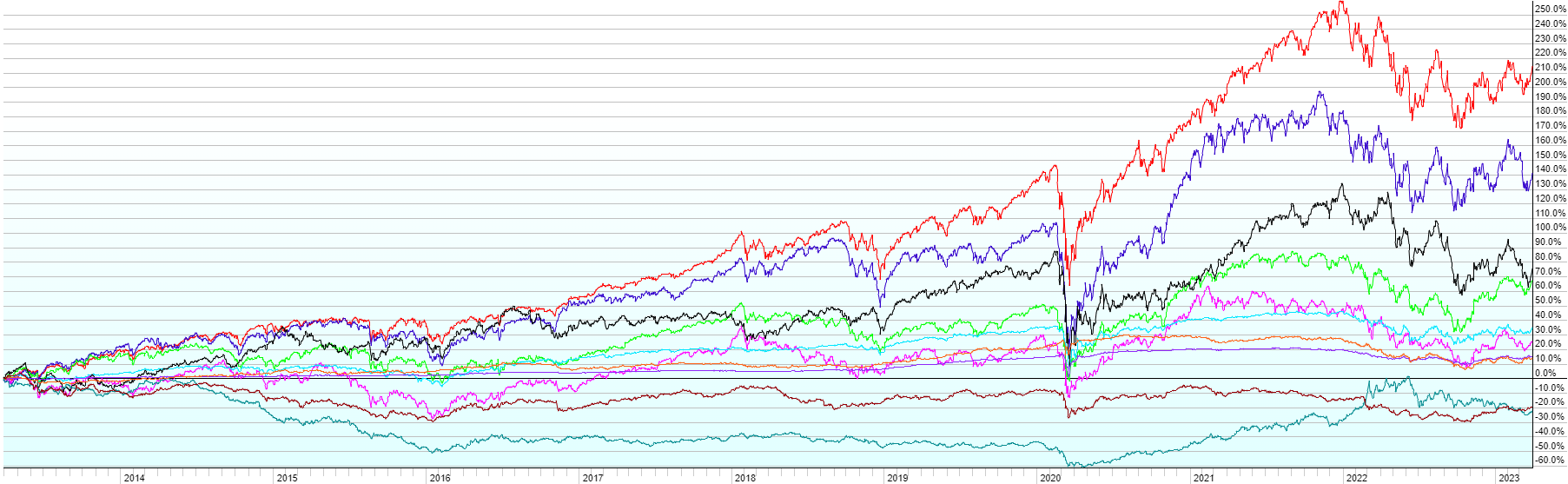

This post contains the usual returns by asset class for this past quarter (by representative ETF), last year, last five years, last ten years, and since the covid low (3/23/2020). While there is still no predictive power in this data, I’ll continue to post this quarterly for those of you that are interested.

A few notes:

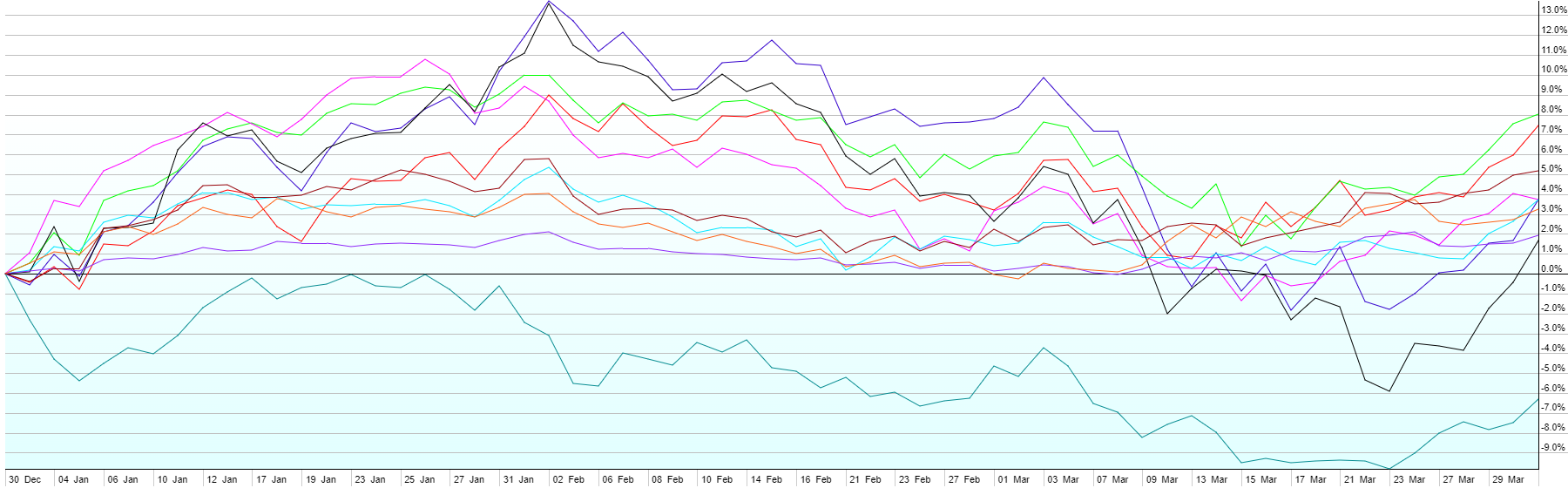

- Q1 2023 felt like it was much longer than just one quarter. After starting with one of the strongest January month’s on record, the next month and half were a disaster for markets as inflation proved to be stubborn, leading to more hawkishness by the Fed. By the end of February, markets were pricing in near 6% short-term rates for the end of 2023. In early March, Silicon Valley Bank and Signature Bank failed after a bank run and fears grew of a much bigger banking crisis. The anticipation of a pullbank in credit stoked recession fears, which were already present due to the pace of Fed rate hikes over the last year. Interest rates tumbled and by the third week in March, markets were pricing in substantial Fed rate cuts by the end of the year. In the last week of the quarter, fear of contagion in the banking sector relaxed a bit after the sale of a large portion of SVB’s assets by the FDIC and substantial investments in other regional banks by some of the stronger players in the space. Rates rebounded somewhat, but stayed in check as markets tried to balance inflation trends with growing concerns that further rate hikes would continue to pressure banks and the economy. With imminent additional bank failures seeming less likely, but interest rates still down considerably from the beginning of March, stocks rallied in the last week, making the quarter a positive one overall. Ending a quarter positive after the 2nd largest bank failure in US history, once again shows us that trying to predict the stock market’s short-term movement is a fruitless endeavor.

- International Developed Stocks led the way for the quarter (+8%) with US Large Caps close behind (+7.5%). Small Caps (+3.7%) fared a bit worse as smaller companies in general need more access to credit than large ones and a banking crisis would increase borrowing costs while decreasing the availability of credit. Additionally, the regional banks, some of which became a concern after the SVB failure, make up a decent portion of the small cap indexes. Real Estate Investment Trusts gained 1.7% after being down as much as 6% in the quarter. Again credit fears and recession put pressure on REITs, with borrowing costs up, housing prices falling, and high vacancies in the corporate real estate space. On the bond side, local currency Emerging Market bonds let the way (+5.2%) as the dollar took a breather on lower rate expectations. High-yield (“junk”) US bonds were up 3.7%, with the Aggregate Bond Market Index up 3.2%, all due to lower rates, which move inversely with bond prices. Shorter-term bonds gained 1-2% in the quarter. Commodities lagged all other asset classes, down 6.3% in the quarter as future inflation expectations cooled and recession fears grew.

- Not shown in the charts above, but growth outperformed value sharply in Q1. Lower future rate expectations seemed to flip a switch that turned everything that fell in 2022, back to growth in Q1 2023. It will take a lot more to undo the carnage in growth stocks, but Q1 was a good start. ARKK, which I’ve mentioned in previous quarters as being one of the most speculative areas of the market, was up 29% in Q1 2023, but is still down 67% from it’s high in Nov 2021.