This post contains the usual returns by asset class for this past quarter (by representative ETF), year-to-date, last 12 months, last five years, last ten years, and since the covid low (3/23/2020). While there is still no predictive power in this data, I’ll continue to post this quarterly for those of you that are interested.

A few notes:

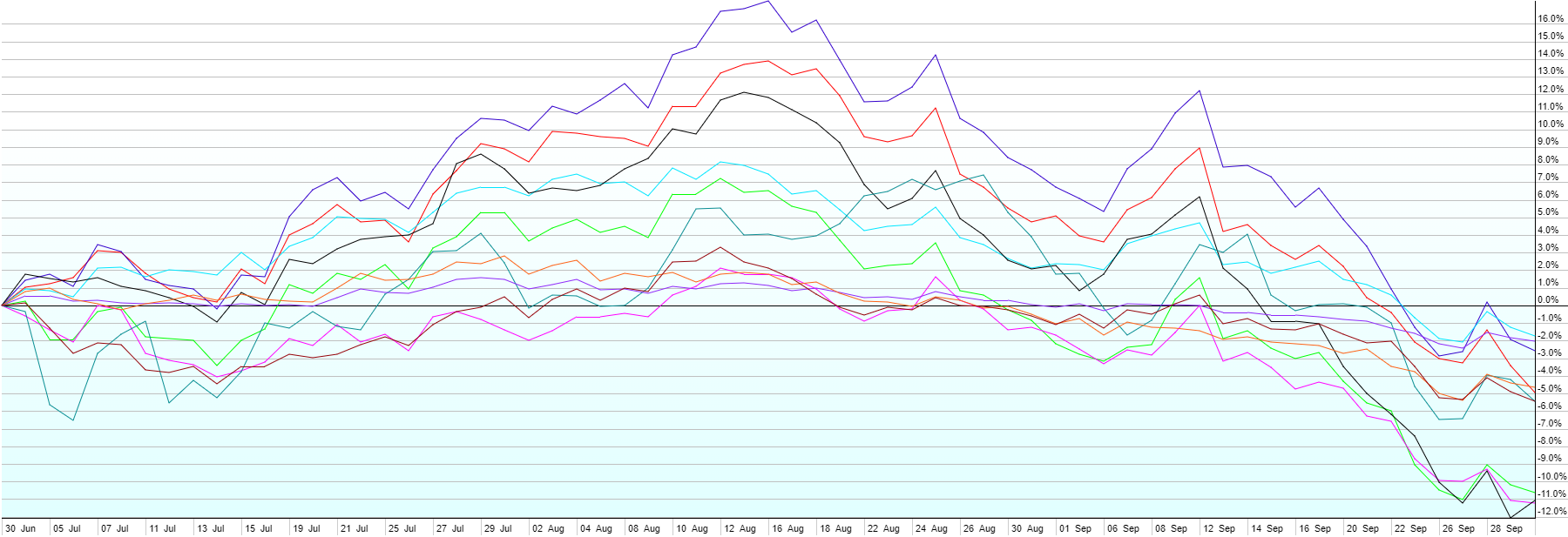

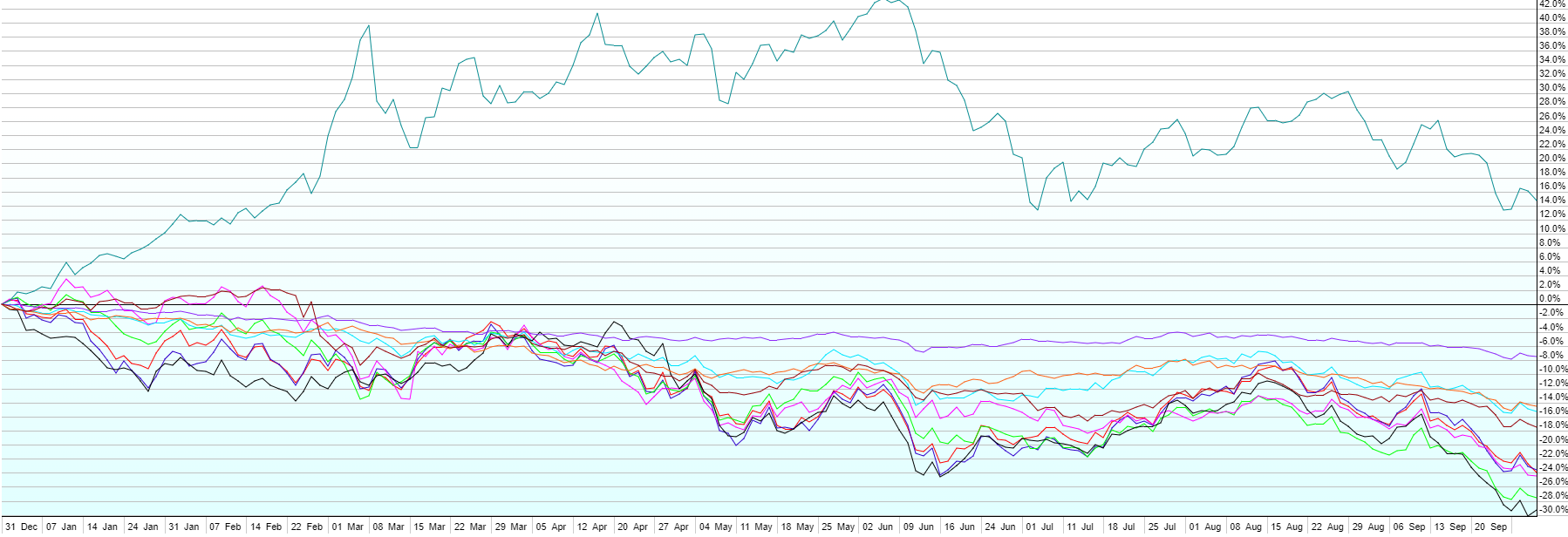

- After spending the first half of Q3 building up significant gains, all asset classes struggled in the second half, closing down for the quarter, and, with the exception of Commodities, down for the year. International Stocks, both Emerging and Developed markets, as well as US Real Estate performed worst (-11% to -12%) for the quarter. “Best” performers for Q3 were High-Yield (junk) bonds, Short-Term Corporate Bonds, and US Small Caps (all down ~2%). US Large Caps (S&P 500), Commodities, Emerging Market Bonds, and US Aggregate Bonds finished the quarter in the middle of the pack, down 5-6% each.

- The turning point for the market was the Federal Reserve’s annual meeting in Jackson Hole in August. There, chairman Jerome Powell reiterated a tough stance against inflation, indicating the Fed was poised to continue to raise rates considerably and willing to accept the “pain” (likely recession) that would result, in order to tame inflation.

- As a result of the Fed’s action, bonds had another tough quarter too in Q3. Long-term treasuries (TLT, not shown above) were down another 11.6% in the quarter, now down ~31% YTD as rates spiked, and prices (which are inversely correlated with rates) sank. We generally keep the bond side of client portfolios much shorter in duration, and include inflation-protected bonds, both of which faired much better again. Short-term inflation protected treasuries were only down ~2.5% for the quarter., with short-term investment-grade credit down less than 2%.

- On the bright side of the bond rout, higher rates means higher yields going forward. Short-term treasuries now yield ~4%, with junk bonds over 8%. Holding funds with bonds that mature soon means that those holdings are soon to be replaced by new bonds that pay today’s higher rates. Short-term losses are made up for quickly by higher yields going forward.

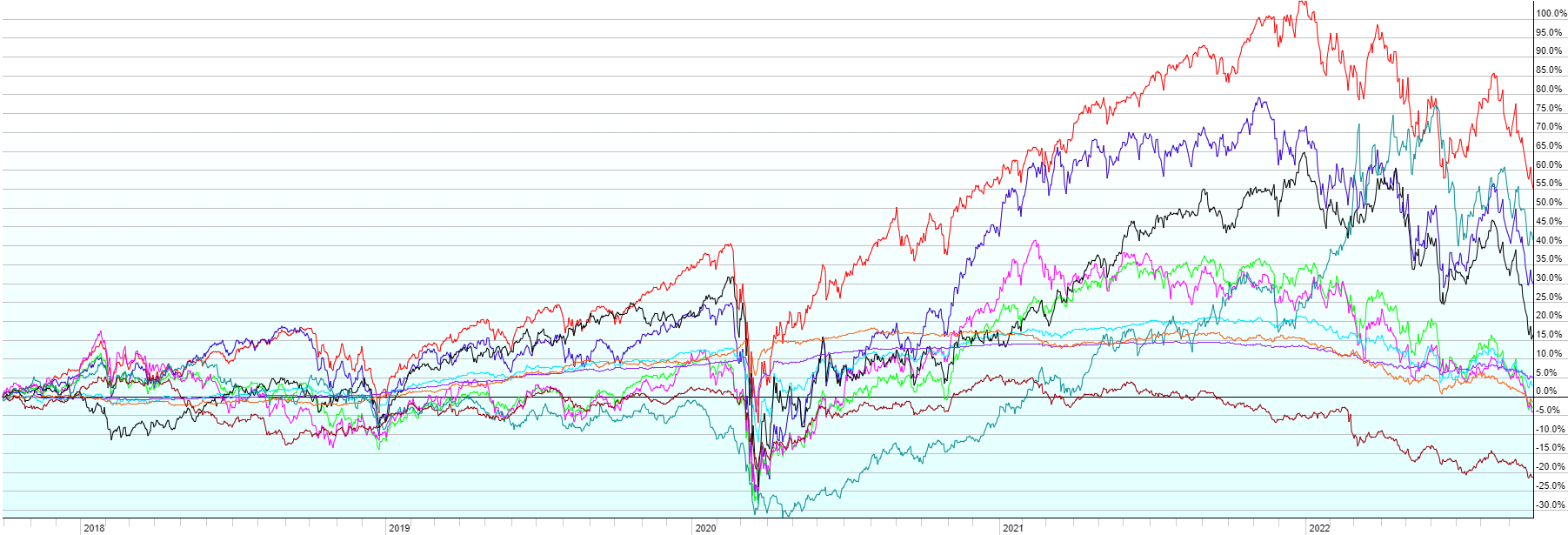

- Interestingly, the ARK Innovation Fund (ARKK), which I’ve mentioned here in previous quarters due to it’s awful performance, did not make a new low for 2022 in Q3, despite the market as a whole doing just that. It’s still down 60% year-to-date though as the values of high-growth stocks have been destroyed by high interest rates.

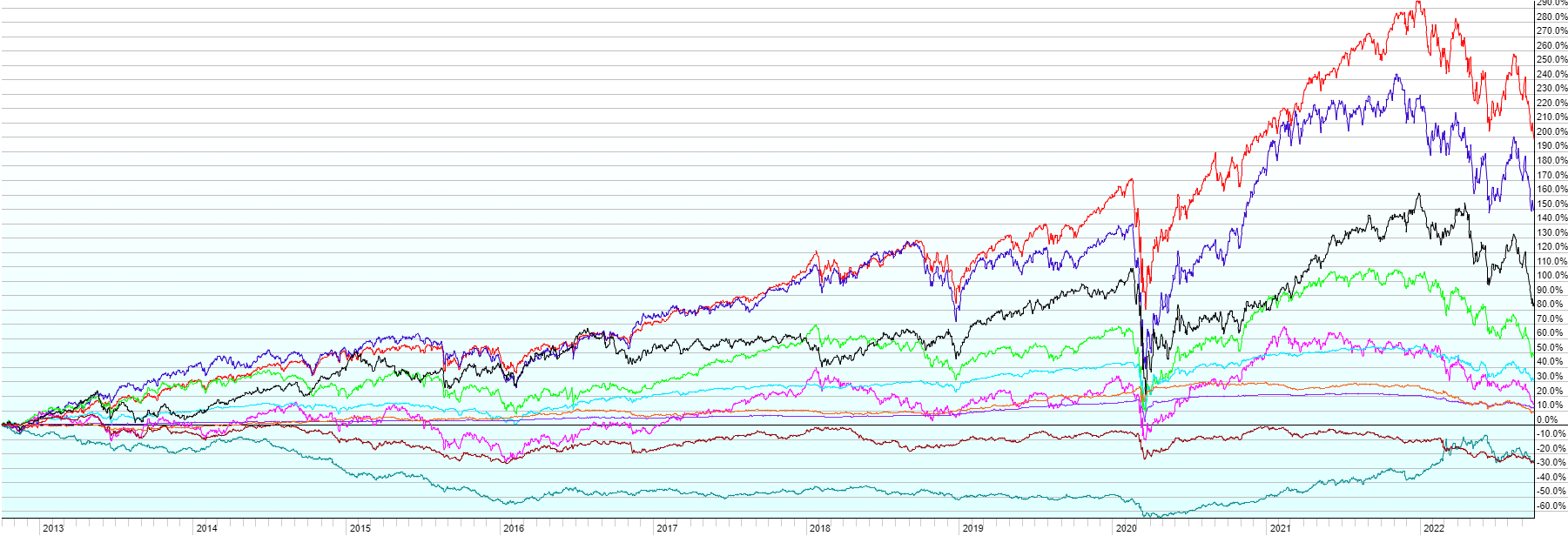

- Markets in general are still sharply up from the 2020 Covid lows and over the last 5 and 10 years. US Large and Small Caps have dominated global performance over the last decade.