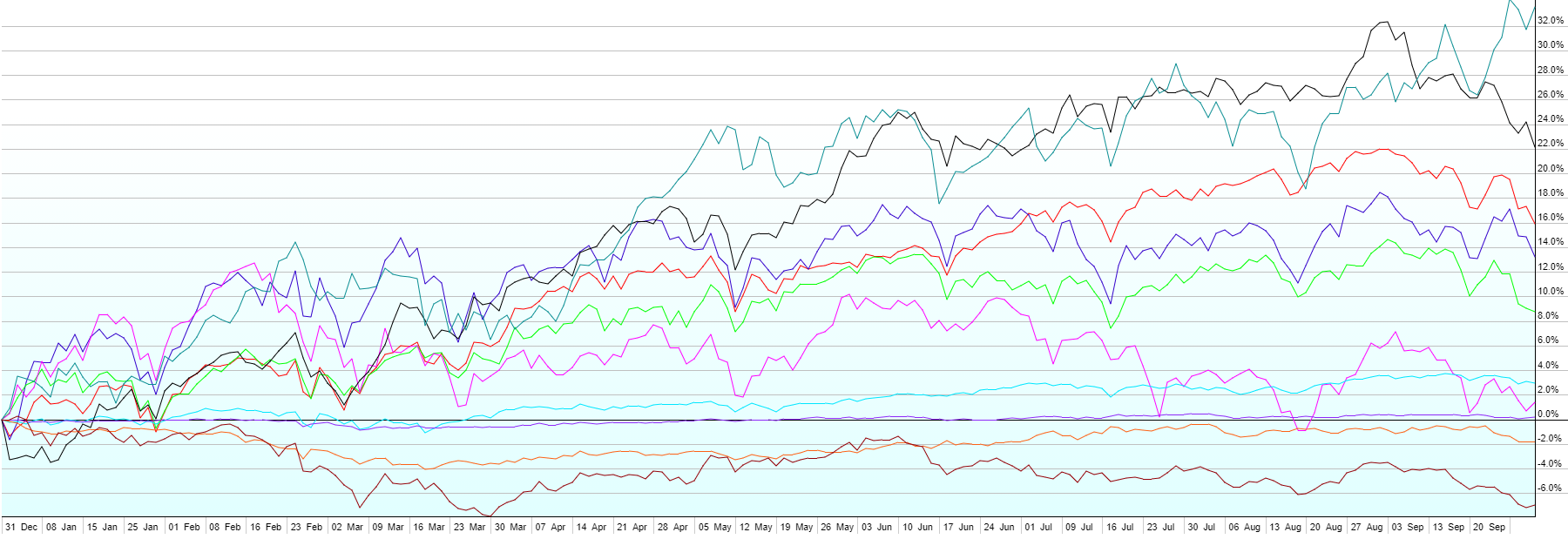

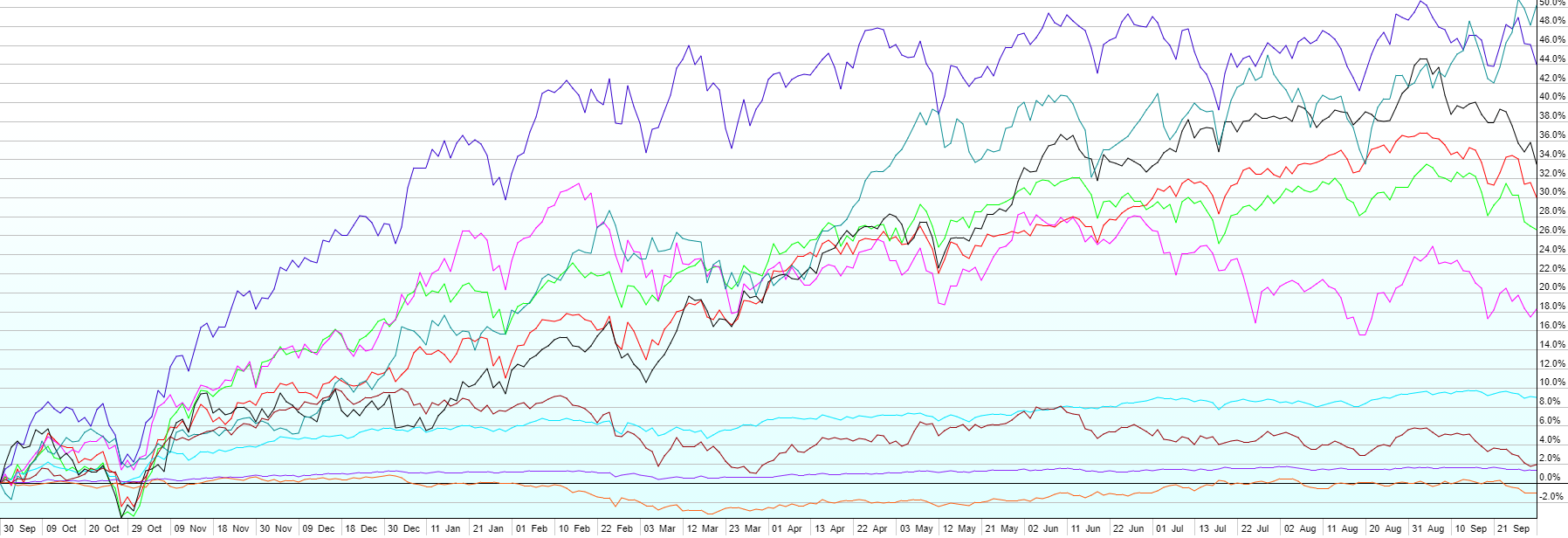

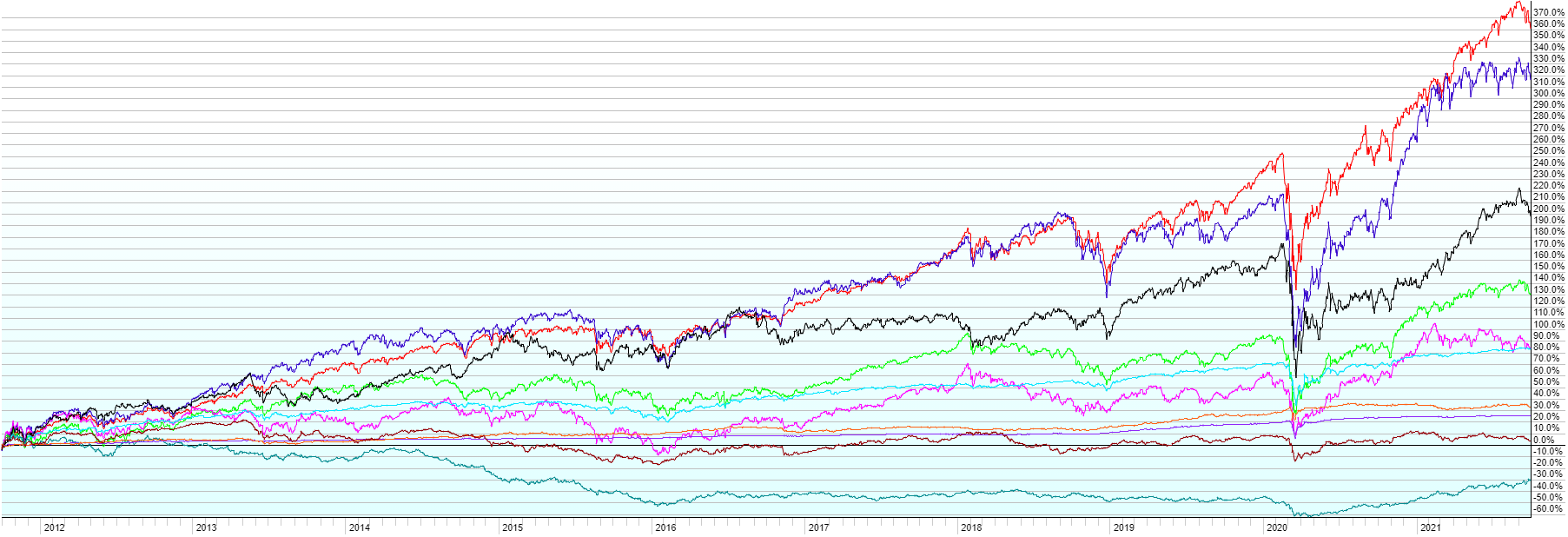

This post contains the usual returns by asset class for this past quarter (by representative ETF), year-to-date, last twelve months, last five years, last 10 years, and since the covid low (3/23/2020). While there is still no predictive power in this data, I’ll continue to post this quarterly for those of you that are interested.

A few notes:

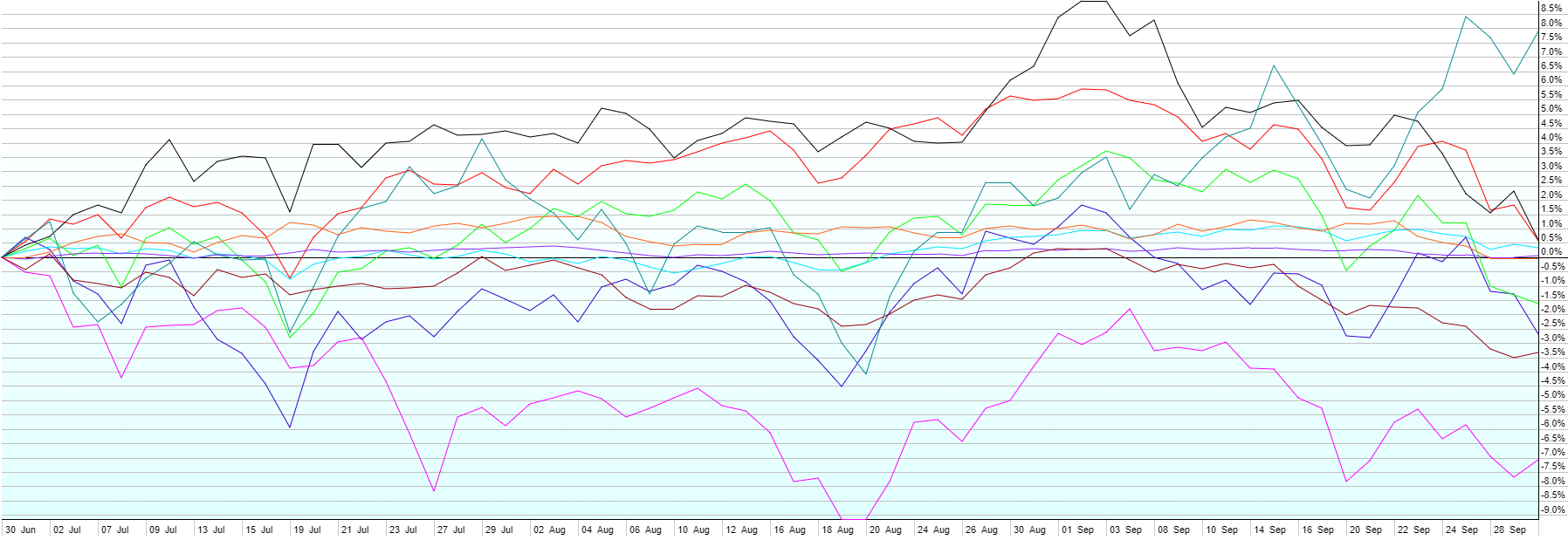

- A solid first two months of the quarter hit an ugly September, which left Q3 mixed to slightly down overall. Commodities led the way (+8%) for the second straight quarter as supply chain issues led to shortages in many areas of the economy. The Fed has softened its opinion on the transitory nature of inflation, and are indicating a chance for costs rising higher than their 2% per year target for some time. They’ve indicated that if the employment picture continues to improve, they’re likely to start tapering their bond purchases (quantitative easing) in the coming months, with rate hikes down the road in late 2022 / early 2023.

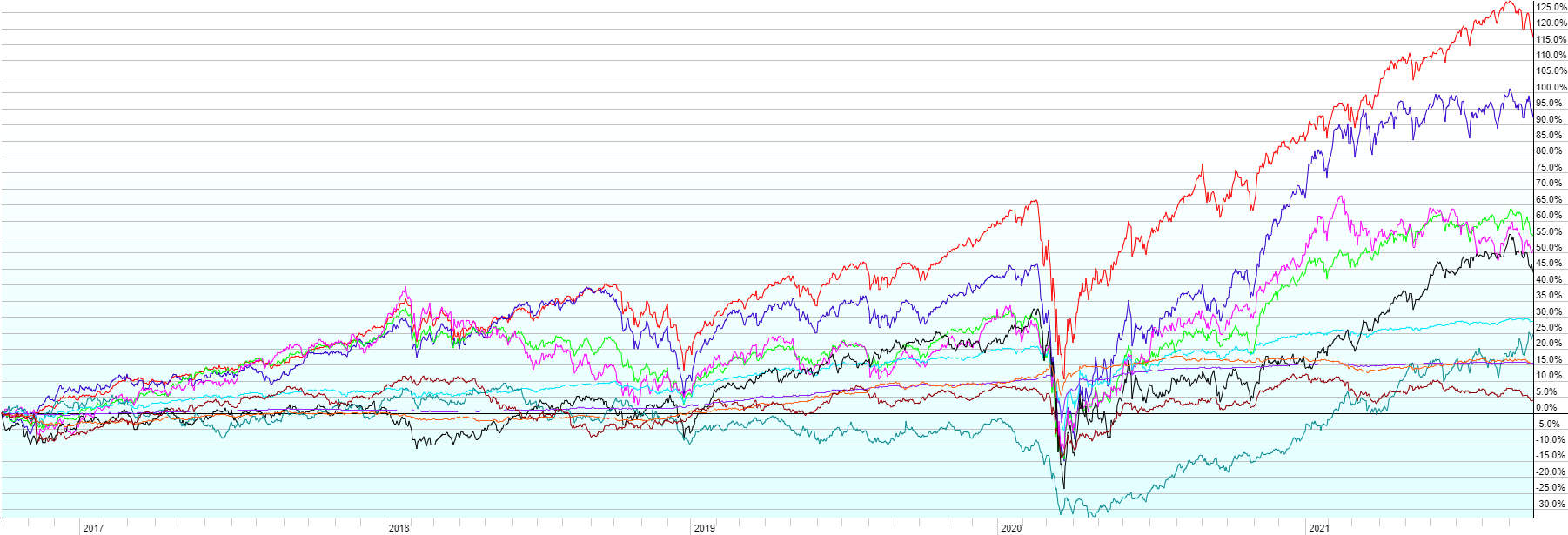

- Rounding out the performance numbers by asset class: US Bonds, US Large Cap Stocks, US Real Estate, and High-Yield Bonds all returned between 0-1% in Q3. On the losing side were Foreign Developed Stocks (-1.5%), US Smalls Caps (-2.5%), Emerging Market Debt (-3.5%), and Emerging Market Stocks (-7%). The stability of bonds made more conservative portfolios outperform in Q3. But, as you can see in the 5-year chart and the “since covid low” chart, overall performance across the financial markets has been superb.

- While commodities have continued to roar back over the past 18 months, the 5 and 10-year charts show just how far they’ve lagged behind other asset classes. Commodities generally track inflation over the long-term, and they really suffered after the financial crisis, the oil glut, and the early part of covid. Now, higher inflation has been pushing commodities higher. Whether that continues or not depends on whether supply constraints ease and on how quickly global demand returns following the peak of the Delta variant of covid (and whatever variant of concern comes next).